Wednesday, November 21, 2012

Honoring a Forecasting Giant

Herman Stekler has predicted 10 of the last 6 U.S. recessions. Despite this dismal forecasting performance, he is considered one of the giants of the economic forecasting profession. At the age of 80, he is still going strong, recently finishing his 100th academic paper.

|

| photo: IMF |

A GW-IMF Forecasting Forum held on November 15-16, 2012 honored Stekler’s contributions to the profession. The program features papers by:

- Prakash Loungani on whether forecasters believe in Okun’s Law (they do);

- Neil Ericsson on uncovering biases in government forecasts of U.S. debt;

- Ulrich Frtische on whether there is (lack of) herding in foreign exchange rate forecasts;

- Michael Kumhof on what will happen to the price of oil in ten years (warning: this is not the official IMF view);

- Natalia Tamirisa on information rigidity in growth forecasts;

- Massimiliano Marcellino on whether the estimation of large Bayesian VARs can be speeded up by assuming a common stochastic volatility factor.

The papers can be downloaded from here along with the comments of the stellar group of discussants (Kajal Lahiri, Tara Sinclair, Ed Gamber, Danny Bachman, Robert Fildes, Jonas Dovern, Olivier Coibion, Andy Levin, Fred Joutz, Chris Erceg, Keith Ord and Xuguang Sheng).

The forecasters attending the forum had been asked to predict the outcome of the U.S. Presidential election. Peg Young came the closest, predicting that Obama would win 50.5% of the popular vote (he got 50.6%) and 326 votes in the electoral college (he got 332).

|

| photo: IMF |

Herman Stekler has predicted 10 of the last 6 U.S. recessions. Despite this dismal forecasting performance, he is considered one of the giants of the economic forecasting profession. At the age of 80, he is still going strong, recently finishing his 100th academic paper.

photo: IMF

A GW-IMF Forecasting Forum held on November 15-16, 2012 honored Stekler’s contributions to the profession. The program features papers by:

- Prakash Loungani on whether forecasters believe in Okun’s Law (they do);

Posted by at 6:05 PM

Labels: Forecasting Forum

Friday, November 2, 2012

Okun’s Law: Fit at 50?

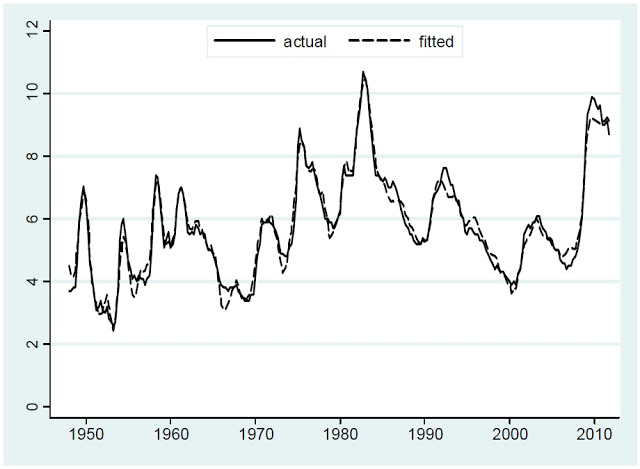

This paper investigates how well Okun’s Law explains short-run unemployment movements in the United States since 1948 and in a sample of 20 advanced economies since 1980. Our principal conclusion is that Okun’s Law is a strong and stable relationship in most countries. Also, the coefficient in the relationship—the effect of a one percent change in output on the unemployment rate—varies substantially across countries. We take a first look at the sources of these differences; one finding is that they are not explained by differences in employment protection laws. Finally, we find that Okun’s Law held up well during the Great Recession and that recoveries have not become “jobless” in the sense of a breakdown in Okun’s Law. The paper is available here.

This paper investigates how well Okun’s Law explains short-run unemployment movements in the United States since 1948 and in a sample of 20 advanced economies since 1980. Our principal conclusion is that Okun’s Law is a strong and stable relationship in most countries. Also, the coefficient in the relationship—the effect of a one percent change in output on the unemployment rate—varies substantially across countries. We take a first look at the sources of these differences;

Posted by at 8:22 AM

Labels: Inclusive Growth

Tuesday, October 16, 2012

Restoring Hope: Policy Options for Jobs & Growth

Sara Eisen of Bloomberg TV moderated a discussion on jobs and growth at the Tokyo annual meetings of the IMF and the World Bank. IMF Deputy Managing Director Zhu said that “in the near term, a growth strategy is the best jobs strategy”. Read his views here.

Sara Eisen of Bloomberg TV moderated a discussion on jobs and growth at the Tokyo annual meetings of the IMF and the World Bank. IMF Deputy Managing Director Zhu said that “in the near term, a growth strategy is the best jobs strategy”. Read his views here.

Posted by at 6:45 PM

Labels: Inclusive Growth

Are We Headed for Another Food Price Crisis?

My presentation at the Bank of America/Merrill Lynch conference in Tokyo is available here.

My presentation at the Bank of America/Merrill Lynch conference in Tokyo is available here.

Posted by at 6:10 PM

Labels: Energy & Climate Change

Wednesday, October 10, 2012

The global impact of the ‘food supply crunch’

From the FT:

Which countries will be worst affected by the sharp rise in global grains prices?

The International Monetary Fund, which has an interest in the question because it is usually a source of loans for countries that have run out of money, has studied the vulnerability of different regions to the jump in food prices due to the US drought.

In one section of its World Economic Outlook published on Monday, the fund analyses the effects of the “food supply crunch”.

While commodities traders – who are awaiting the US Department of Agriculture’s monthly forecasts on Thursday – may have already moved on from the US drought, higher prices are still a reality for consumers of wheat, corn and soyabeans. Despite a recent correction, prices for the three staples are still up 20-40 per cent year on year.

The IMF breaks down the issue into three sub-questions: which countries have low food inventories; which countries are most dependent on the global markets for their food supply; and which countries’ populations spend the largest proportion of their income on food.

The countries and regions at the most vulnerable end of the range for each of the categories are the most likely to suffer problems, the fund explains.

While China is a large importer of some foodstuffs (especially oilseeds), it would be able to withstand higher prices better than others because of its large stockpiles. At the other end of the scale, inventories of food commodities in the US have fallen well below historical norms, but food is a relatively small proportion of US consumer expenditure, therefore the country is less exposed.

It may not come as a complete surprise to learn which countries are most at risk. They are: the Caribbean and Central America, which are heavily reliant on corn imports and whose stocks are lower than during the 2007-08 food crisis; the Middle East and sub-Saharan Africa, which have relatively high import reliance and low inventories of wheat; and north Africa, where food accounts for about 40 per cent of final consumption.

Indeed, Morocco, which is forecast to import a record 4.5m tonnes of wheat this year, has already sought a $6.2bn precautionary loan from the IMF.

But the IMF says that the current situation is less severe than in 2007-08 as rice prices remain subdued, oil prices are not so high, and so far, there have not been widespread export restrictions.

Nonetheless, the fund concludes: “Countries should expect rising inflation and balance of payments pressures.”

From the FT:

Which countries will be worst affected by the sharp rise in global grains prices?

The International Monetary Fund, which has an interest in the question because it is usually a source of loans for countries that have run out of money, has studied the vulnerability of different regions to the jump in food prices due to the US drought.

In one section of its World Economic Outlook published on Monday,

Posted by at 10:09 AM

Labels: Energy & Climate Change

Subscribe to: Posts