Wednesday, July 17, 2013

House Prices in the United Kingdom

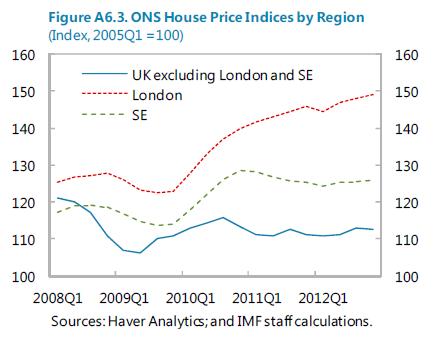

“(…) house prices in the UK are currently high relative to incomes and rents,” says the latest IMF report on house prices in the UK. More specifically, it says:

- “Residential property prices in the UK are elevated relative to incomes and rents. Although house prices declined significantly during the crisis (13 percent), they have recovered substantially, reaching near pre-crisis peak values. Moreover, residential property values are currently about 20 percent above their historical average values of price-to-income and price-to rent ratios.”

- “This aggregate trend masks some variation across regions. London remains prime real estate and prices are now 12 percent higher relative to their 2007 peak value. In the South East region, prices have stabilized at around 4 percent above their pre-crisis peak values. By contrast, in the rest of Britain house price inflation is zero, although residential values have stabilized at around 6 percent above their trough values.”

- “Overseas investment may be an important factor in driving the rapid increase in London house prices. London receives a constant flow of property investors from across Europe, the Middle East and Asia, who are looking for safe investments to protect their wealth. House purchases by foreigners amounted to 5 percent of total transactions in the UK in 2012, and this represented a 40 percent increase relative to 2010 in value terms.”

“(…) house prices in the UK are currently high relative to incomes and rents,” says the latest IMF report on house prices in the UK. More specifically, it says:

- “Residential property prices in the UK are elevated relative to incomes and rents. Although house prices declined significantly during the crisis (13 percent), they have recovered substantially, reaching near pre-crisis peak values. Moreover, residential property values are currently about 20 percent above their historical average values of price-to-income and price-to rent ratios.”

Posted by at 6:43 PM

Labels: Global Housing Watch

House Prices in China

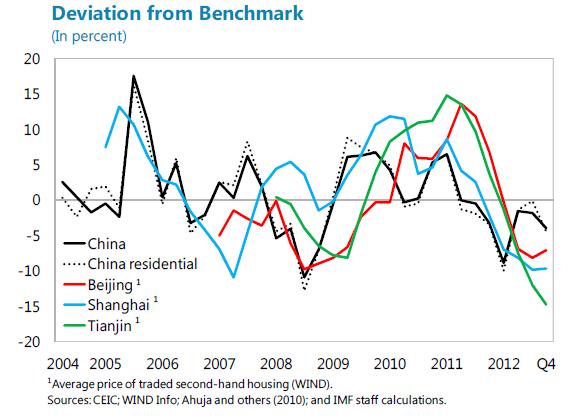

“Real estate has rebounded,” is one of the messages of the latest IMF’s economic report on China. The report says, “Real estate investment in 2012 accounted for 12½ percent of China’s GDP, 14 percent of total urban employment, and rising share of FAI. Lending to real estate is primarily for household mortgages and has slowed recently. The real estate market has shown signs of a recovery lately, with moderate growth in prices, investment, and sales and affordability indices have been improving and prices now seem to be broadly in line or even below fundamentals nationwide and in major cities. Over the medium term, residential construction is likely to slow as the market matures.”

“Real estate has rebounded,” is one of the messages of the latest IMF’s economic report on China. The report says, “Real estate investment in 2012 accounted for 12½ percent of China’s GDP, 14 percent of total urban employment, and rising share of FAI. Lending to real estate is primarily for household mortgages and has slowed recently. The real estate market has shown signs of a recovery lately, with moderate growth in prices, investment, and sales and affordability indices have been improving and prices now seem to be broadly in line or even below fundamentals nationwide and in major cities.

Posted by at 6:43 PM

Labels: Global Housing Watch

Friday, July 12, 2013

House Prices in Malta

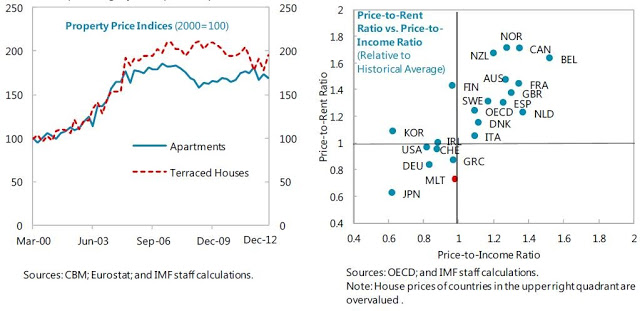

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

Posted by at 9:41 PM

Labels: Global Housing Watch

Wednesday, July 10, 2013

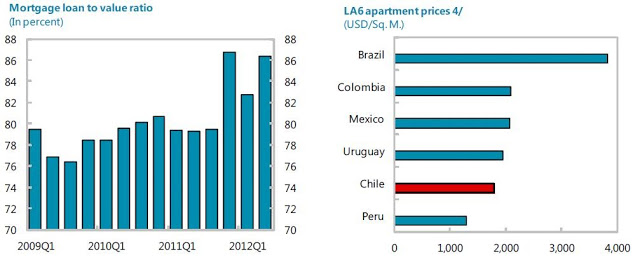

House Prices in Chile

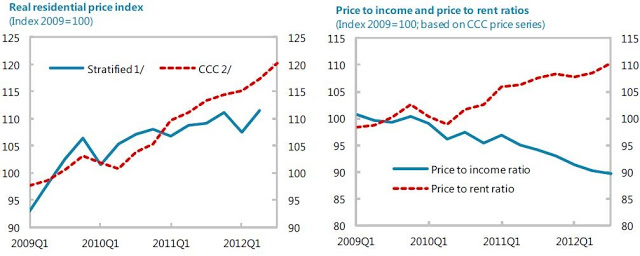

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011, as highlighted in recent central bank financial stability reports. Another issue is the above-mentioned worsening in construction companies’ financial strength. As for construction, while residential housing activity seems to be cooling off, commercial real estate (for which data are spotty) remains hot with a substantial amount of office space being completed in 2013-14.”

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011,

Posted by at 2:39 PM

Labels: Global Housing Watch

Friday, June 21, 2013

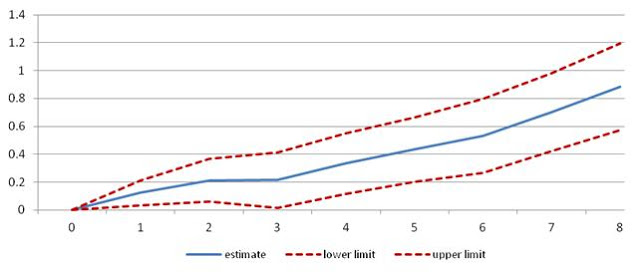

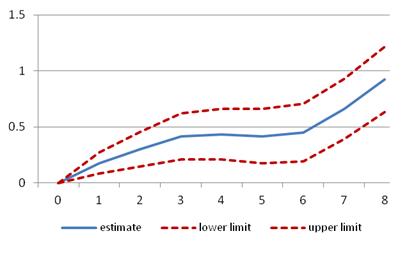

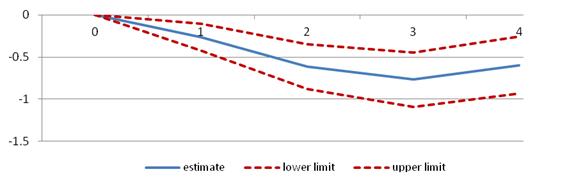

Does Fiscal Consolidation Raise Inequality?

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Fiscal consolidation raises inequality (as measured by the Gini Coefficient)

(The horizontal axis shows the year of the consolidation—year 0—and the impact up to 8 years after the consolidation)

Consolidation based on spending cuts raises inequality …

… as does consolidation based on tax increases

Fiscal consolidation lowers the wage share of income

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Posted by at 7:07 PM

Labels: Inclusive Growth

Subscribe to: Posts