Wednesday, August 12, 2015

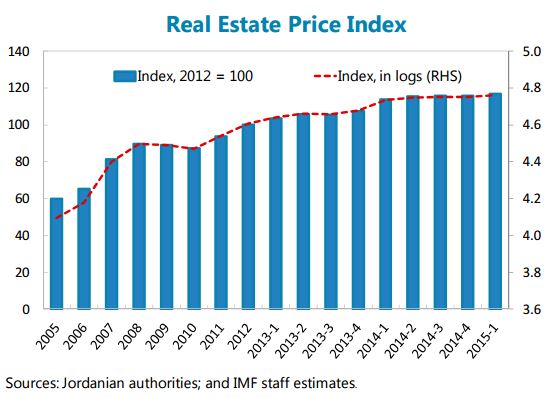

House Prices in Jordan

“Mortgages slowed down in tandem with real estate prices; exposure of banks to real estate credit risk has remained limited”, notes the latest IMF report on Jordan.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, August 10, 2015

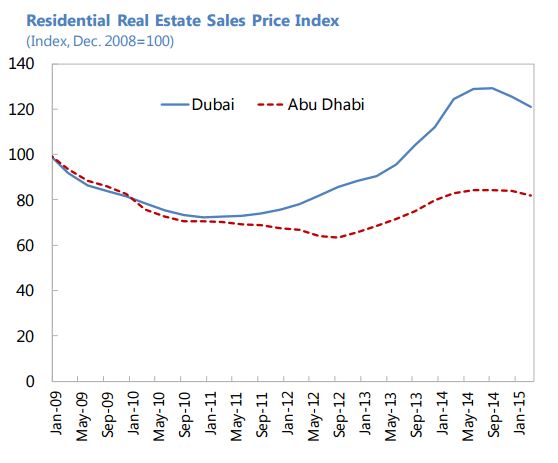

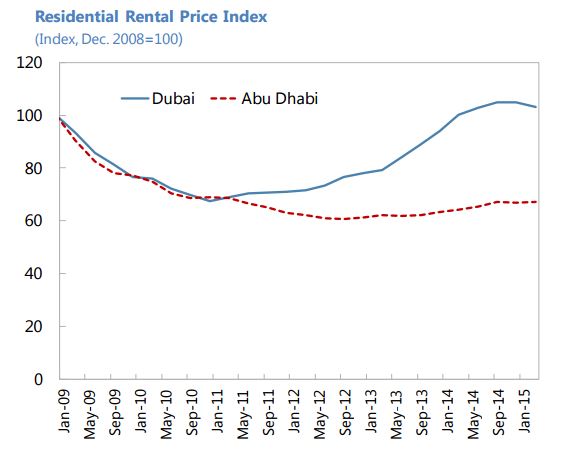

House Prices in United Arab Emirates

“The real estate market in the UAE has cooled down after expanding strongly in 2013 and the first half of 2014. By end-2014, sales price increases moderated in Dubai and Abu Dhabi, and in March 2015, growth in residential sales prices turned slightly negative in both Emirates, in year-on-year terms (…). These developments are taking place amid increased supply, particularly in Dubai, and reduced demand associated with lower oil prices and appreciating US dollar, and following the introduction of mortgage regulations based on loan-to-value ratios and an increase in the property transfer fee in late 2013. Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, August 5, 2015

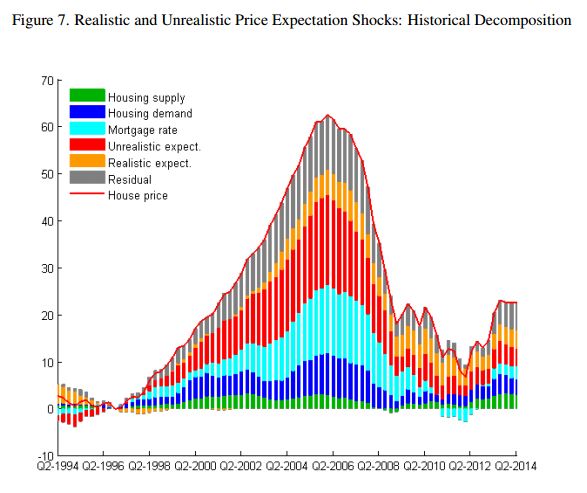

Price Expectations and the US Housing Boom

A new IMF paper by Pascal Towbin and Sebastian Weber looks at the shifts in house price expectations as an important driver of the US house price boom that preceded the financial crisis.

The authors find “that the contribution of price expectation shocks to the U.S. housing boom in the 2000s has been substantial. In our baseline specification, price expectation shocks explain roughly 30% of the increase. Another 30% of the increase in house prices remains, Read the full article…

Posted by at 12:00 PM

Labels: Global Housing Watch

Tuesday, August 4, 2015

House Prices in Europe

growth is still low and the housing market recovery is still at an early stage. Macroprudential policies

are the first option, although responsibility in this area is shared between the ECB and national

authorities” notes the IMF report on the Euro Area.

“Credit

growth is still low and the housing market recovery is still at an early stage. Macroprudential policies

are the first option, although responsibility in this area is shared between the ECB and national

authorities” notes the IMF report on the Euro Area.

Posted by at 4:20 PM

Labels: Global Housing Watch

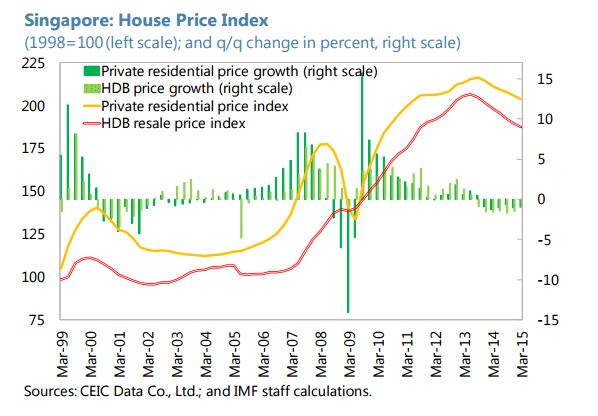

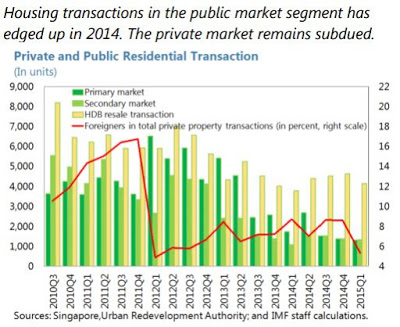

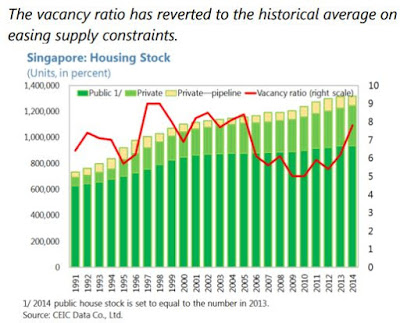

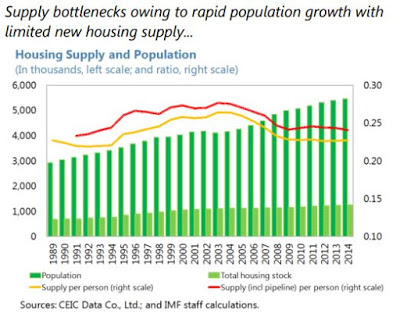

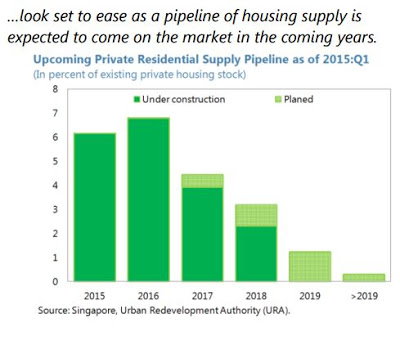

House Prices in Singapore

“Recent macroprudential measures have contributed to smoothing the cycle for credit and house prices”, says IMF’s annual report on Singapore. More specifically, the report notes that “House prices have continued to decline modestly and are below their peaks by 9 percent and 6 percent in the public resale and private market segments as of the first quarter of 2015, respectively. The pace of house price decline has been slower over the past 7 quarters, Read the full article…

Posted by at 3:52 PM

Labels: Global Housing Watch

Subscribe to: Posts