Wednesday, August 5, 2015

Price Expectations and the US Housing Boom

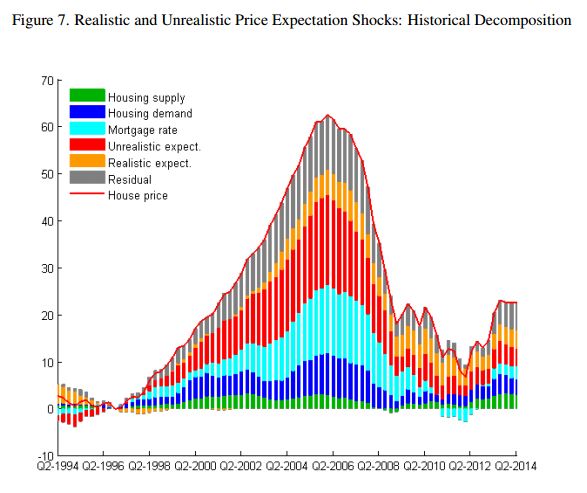

A new IMF paper by Pascal Towbin and Sebastian Weber looks at the shifts in house price expectations as an important driver of the US house price boom that preceded the financial crisis.

The authors find “that the contribution of price expectation shocks to the U.S. housing boom in the 2000s has been substantial. In our baseline specification, price expectation shocks explain roughly 30% of the increase. Another 30% of the increase in house prices remains, however, unaccounted for by the four identified shocks. This indicates that attributing the entire residual that cannot be explained by standard shocks to price expectations will lead to an overestimation of their contribution. We also find that a model-based measure of house price expectations is strongly positively correlated with leads of a survey based measure of house price expectations. This indicates that our measure contains similar information as a survey-based measure, but tends to provide the information more timely. Our approach to identify price expectation shocks leaves the reason why expectations change open. When using an additional constraint to distinguish realistic from unrealistic price expectation shocks, we provide evidence that the housing boom was driven to an important extent by unrealistic price expectations.”

Posted by at 12:00 PM

Labels: Global Housing Watch

Subscribe to: Posts