Friday, October 2, 2015

The Frenchman Who Reshaped the IMF

Reflections on the work of Olivier, the IMF’s now retired chief economist.

The IMF is often caricatured as an institution that wants to nail every problem with the hammer of austerity and structural reforms.

An article in TIME claimed that the IMF tends to “dish out roughly similar advice to all countries, no matter what their circumstances,” noting that a cursory look at the IMF’s website would show that “prudent fiscal policy and reforms” had been recommended to Lesotho, France and Russia.

Whatever the merits of the caricature, Olivier Blanchard, the French-born, former MIT economist who served as the IMF’s chief economist from September 2008 to September 2015, achieved a rare feat.

He not only changed perceptions of the institution both on the inside and the outside but also, even more crucially, managed to reshape IMF policies.

Under Blanchard’s watch, the IMF:

- lent its support to a global fiscal stimulus during the Great Recession

- urged a very cautious removal of this stimulus during the Not-So-Great Recovery, and

- staunchly advocated easy monetary policies—including quantitative easing.

Even a famous critic of the institution agreed: “A recovery in aggregate demand is the single best cure … what a relief to hear the Fund say that,” Paul Krugman cooed about the thrust of IMF policy prescriptions during the Great Recession.

Olivier Blanchard also threw out some controversial ideas for discussion, such as: Should inflation targets be raised?

That idea ran into some predictable criticism (“if you flirt with inflation, you end up marrying it,” said a former German Bundesbank president).

But it also drew fire from friendly sources—Blanchard’s mentor and long-time collaborator Stan Fischer, currently the U.S. Fed Vice Chairman, thinks that a higher target would be a “mistake.”

Blanchard also nudged the IMF towards less doctrinaire positions on several other issues, notably on the use of capital controls during crises.

He thereby gave an impetus to a rethinking that had started after the Asian crisis of 1997-98—see my article for The Globalist entitled “The Vindication of Joe Stiglitz.”

The fiscal triptych

The biggest change that Blanchard brought about was in the IMF’s advice on fiscal policies. This came in three steps:

- In early 2008, Larry Summers advocated a U.S. fiscal stimulus that was “timely, targeted and temporary.” Avoiding alliteration’s allure, Blanchard and co-authors advocated a global fiscal stimulus that was “timely, large, lasting, diversified, contingent, collective, and sustainable.”

- Next came a chapter in the October 2010 edition of the IMF’s flagship publication (World Economic Outlook), which Blanchard played an active role in shaping. To the question “Will austerity hurt?” the chapter gave a clear answer: “Yes.

- And then came three pages that Gavyn Davies in a FT blog said could have “a greater effect on global economic policy than all of the interminable” sessions held in Tokyo that year at the Bank-Fund annual meetings.

This was in the October 2012 World Economic Outlook—and subsequent paper — where Blanchard and his colleague Daniel Leigh showed that “in advanced economies, stronger planned fiscal consolidation has been associated with lower growth than expected.”

Translation: the adverse impact of austerity on output was perhaps larger than had been expected.

The upshot of this work was not that fiscal consolidation should never be undertaken. Rather, it was that one should expect austerity to lower output.

Moreover, this effect could be greater in some circumstances (e.g., when monetary policy was constrained because policy interest rates could not be pushed below zero).

It wasn’t just fiscal

Here are three other areas where Blanchard left his imprint through his own writing, by guiding the work of others or by creating an open atmosphere where his staff could explore new pastures:

Who’s afraid of capital controls?

Blanchard presided over a series of papers by IMF staff that nudged the Fund towards a more flexible position on capital controls.

A December 2012 blog by Blanchard and Ostry “explains the logic and research that underpins the shift” in the Fund’s position.

The “4% solution”

In a paper with Giovanni Dell’Ariccia and Paolo Mauro, Olivier posed the question: “Should policymakers therefore aim for a higher target inflation rate in normal times, in order to increase the room for monetary policy to react to such shocks?”

Though the paper never explicitly advocated a new 4% target (that was done later by Larry Ball in an IMF working paper), and certainly not one to be adopted right away, this quickly became known as the “4 percent solution.”

Inequality

The IMF has received a lot of credit for its work on inequality. The finding that captured attention — by Jonathan Ostry and Andy Berg — was that inequality was detrimental to sustained growth.

Blanchard initially regarded this finding as an interesting cross-section correlation and then as a correlation that had cleverly tapped into the zeitgeist.

It is only more recently, in his foreword to the April 2014 WEO, that Blanchard has come to the view that the implications of inequality for macroeconomic developments are a “central issue.”

From the Globalist:

Reflections on the work of Olivier, the IMF’s now retired chief economist.

The IMF is often caricatured as an institution that wants to nail every problem with the hammer of austerity and structural reforms.

An article in TIME claimed that the IMF tends to “dish out roughly similar advice to all countries, no matter what their circumstances,” noting that a cursory look at the IMF’s website would show that “prudent fiscal policy and reforms” had been recommended to Lesotho,

Posted by at 12:14 PM

Labels: Profiles of Economists

Thursday, October 1, 2015

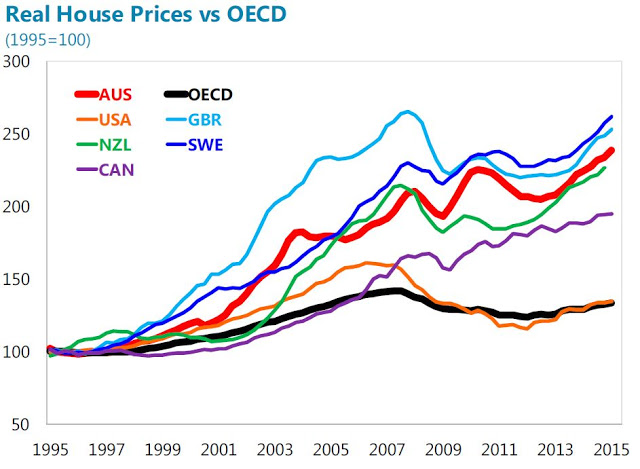

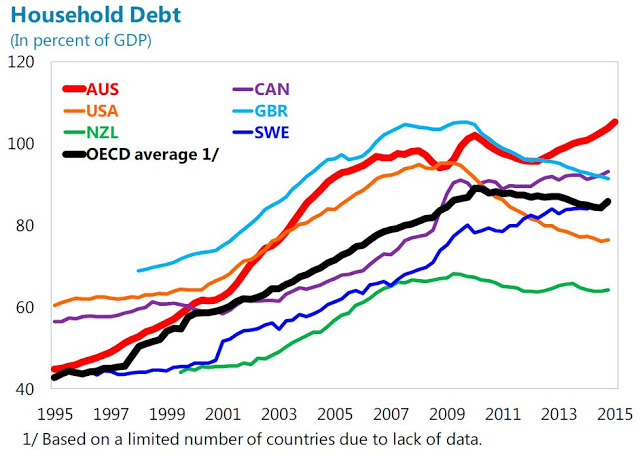

Are Australia’s House Prices Overvalued?

Below is the argument, counter arguments, and the bottom line from the study:

Argument: House prices have risen faster in Australia than in most other countries, suggesting, ceteris paribus, overvaluation

Counter argument 1: House prices are in line on an absolute basis

Bottom line: Price-to-income ratios have risen across all measures in Australia and are now near historic highs. However, international comparisons of price-to-income ratios suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.

Counter argument 2: The equilibrium level of house prices has also risen sharply

Bottom line: Lower nominal and real interest rates and financial liberalization are key contributors to the strong increases in house prices over the past two decades. The various house price modeling approaches indicate that house prices are moderately stronger (in the range of 4-19 percent) than economic fundamentals would suggest.

Counter argument 3: High prices reflect low supply

Bottom line: housing supply does indeed seem to have grown significantly slower than demand, reducing (but not eliminating) concerns about overvaluation.

Counter argument 4: It is just a Sydney problem, not a national one

Bottom line: The two most populous cities, Sydney and Melbourne, have seen strong house price increase in recent years, including in the investor segment. A sharp downturn in the housing market in these cities could be expected to have real sector spillovers, pointing to the need for targeted measures –including investor lending-to reduce the risks related to a housing downturn.

Counter argument 5: There are no signs of weakening lending standards or speculation

Bottom line: While lending standards overall seem not to have loosened, the growing share of investor and interest only loans focused on the highly-buoyant Sydney market, is a pocket of concern.

Counter argument 6: Even if they are overvalued, it doesn’t matter as banks can withstand a big fall

Bottom line: While bank capital levels are likely sufficient to keep them solvent in the event of a major fall in house prices, they are not enough to prevent banks making an already extremely difficult macroeconomic situation worse.

“House prices in Australia have increased strongly over the past two decades, including by comparison internationally. Thus house prices are often argued to be overvalued. Many counter-arguments have been put forward for why such measures are flawed. We argue that house prices are moderately stronger than consistent with current economic fundamentals, but less than a comparison to historical or international averages would suggest”, according to the IMF special report on Australia’s housing market.

Below is the argument,

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, September 30, 2015

US Housing Market: An Update

What are the latest developments and emerging trends in the US housing and mortgage markets? This was the overall question that was the subject of a recent conference organized by Goldman Sachs in New York City on September 11. Here is a brief summary on the conference takeaways (extracts are taken from a note prepared by Hui Shan and Marty Young, both from Goldman Sachs).

On the housing market: “Housing starts far from normal, but hard constraints prevent a faster pace of normalization. The prolonged downturn disrupted the supply chain. For example, trade schools for construction workers disappeared, local governments cut back on their capacity in granting building permits, and builders did not begin buying lots three years ago, as they were not sure that housing had bottomed or could not secure financing. These forces add up to a slow pace of recovery.” Moreover, “There has been a seismic shift in household composition, with more singles and more families without kids. Both demographic and business cycle forces point to expanded growth in multi-family rental into the future.”

On how technology can change the housing and mortgage markets? “Compared to many other industries, housing and mortgage markets have lagged in their adoption of technology. More recently, real estate brokers have been using online search data to predict house price and home sales movements.” However, more could be done. For example, “Embracing e-Mortgage technology could potentially shorten closing timelines and reduce costs.”

On policy: “Housing policy needs to adapt to the new economy. Traditional ways of underwriting mortgages need to be changed to adapt to the evolving economy. For example, new FICO score formulas that reduce the weight of medical debt need to be incorporated. Income of borrowers such as Uber drivers needs to be underwritten properly. An inability to adjust to the changing economy can result in an inadvertent tightening of mortgage lending.”

From the Global Housing Watch Newsletter: September 2015

What are the latest developments and emerging trends in the US housing and mortgage markets? This was the overall question that was the subject of a recent conference organized by Goldman Sachs in New York City on September 11. Here is a brief summary on the conference takeaways (extracts are taken from a note prepared by Hui Shan and Marty Young, both from Goldman Sachs).

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, September 28, 2015

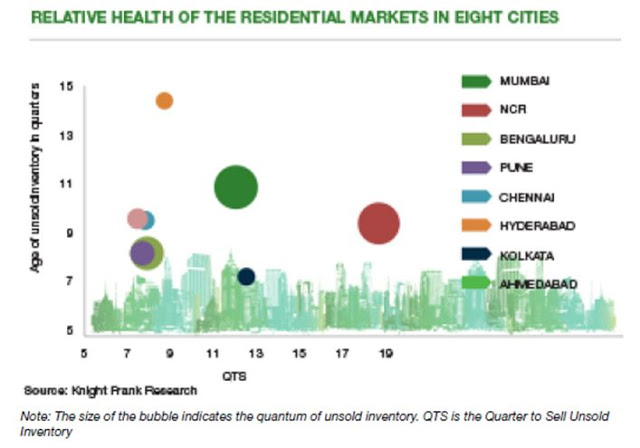

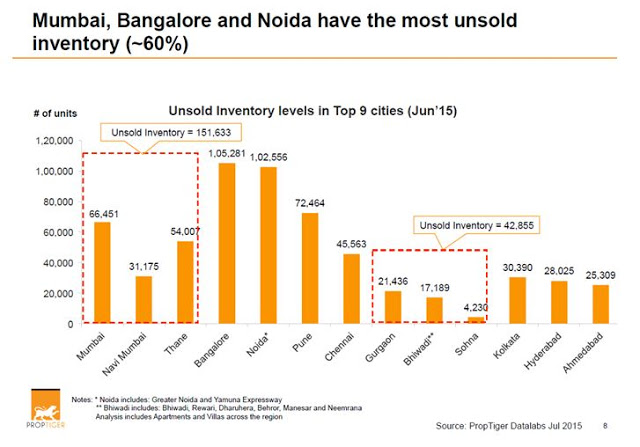

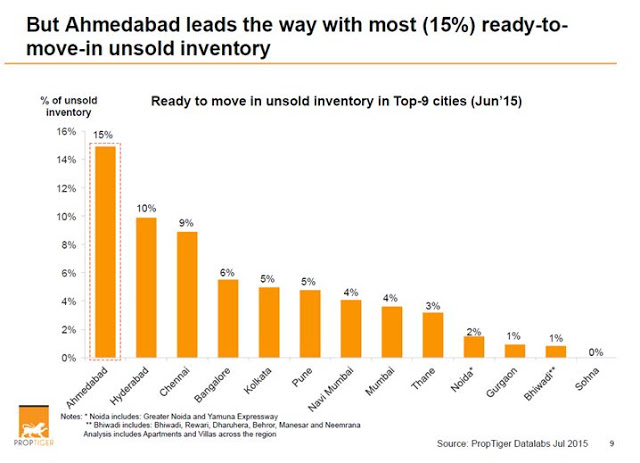

India’s Housing Market: What’s happened? What’s next?

What’s happened to India’s housing market? There seems to be a slowdown and also a rising stock of unsold houses. This development has led to different views on India’s housing market. In a recent interview, Raghuram Rajan (Reserve Bank of India—RBI) said that “if real estate developers, who are sitting on unsold [housing] stocks, start bringing down prices, that will be a very big help to the sector because once there is a sense that the prices have stabilized more people will be willing to buy. (…) we also don’t want to create a situation where prices stay high at the level, which means demand can’t pick up (…)”. Similarly, the National Housing Bank (NHB) and Rayman Partners also agree that house prices are high. In terms of how long it will take to clear the housing inventory, Knight Frank says that “Mumbai has the highest number of unsold units in India (…). However, the NCR [National Capital Region] market will take the maximum time to liquidate its existing unsold inventory. At the current pace of sales, NCR will take more than four years to exhaust the unsold homes completely. Pune is currently the healthiest market, with the lowest QTS [quarters to sell unsold inventory] and a relatively lower age of unsold inventory”.

However, PropTiger and Farook Mahmood (Silverline Group and Chairman of NAR-India 7th Annual Convention) noted that when we talk about housing inventory data, we need to differentiate between the different types of inventory (e.g. ready-to-move-in vs. under-construction).

Also, the price of the unsold housing stock differs. For example, “69% of Mumbai’s unsold housing stock is priced above Rs. 1 Crore”, notes Ramesh Nair at Jones Lang LaSalle. Meanwhile, Irfan Razack (Prestige Group) stated that “(…) prices could come down only if the government reduced taxes related to property and ensured speedy approval of projects.” And Shashank Jain (PricewaterhouseCoopers) said “(…) developers were unlikely to drop base prices (…) if base prices were reduced, buyers may hold back purchases expecting more cuts in future. That would become counterproductive for the industry and economy.” Finally, a report by Ambit notes that there is “(…) a broad-based real estate pullback, with prices correcting in most tier I and tier II cities alongside sharp drops in transaction and new launch volumes. The drivers for this slowdown are a mix of supply-side factors (banks have pulled back lending to developers) and demand-side factors (the black money bill has created fear amongst speculators).”

What’s next for India’s housing market? “As the economic growth has started to take off, the overall buyer sentiment is expected to rise. Presumably, developers are counting on this to happen and hence holding the prices”, according to the RBI’s latest report. Meanwhile, PropTiger says that the housing market “(…) will soon be in better shape with the number of new launches likely to rise (…) when the festival season begins in October (…) the Q1 report predicts that the prices are not likely to fall in the near future.” On the unsold inventory, Knight Frank says that “(…) the unwinding process of the excess unsold inventory in these markets has already commenced since the first half of this year and (…) this process will continue for another six months in order to bring stability in the residential market. The deliberate slowdown in new launches undertaken by the real estate developer fraternity seems to be a pragmatic step in this direction and will hopefully lead the industry towards a path of sustainable development.” Finally, Shashank Jain says that “The inherent Indian demographics still makes the country’s real estate sector attractive. But if you are looking at short-term gains, then that continues to be a challenge (…) The long-term story is intact.”

More on India’s housing market. Charan Singh (Indian Institute of Management Bangalore) has studied the housing market in India. On India’s house price index, Singh notes that the NHB and RBI construct and release a house price index. But, there are a number of problems with both indices. NHB’s HPI “(…) is based on extensive data collected by different commercial banks and finance company located in 26 cities and is widely accepted in the country. Innovations that rely on data sources cannot be implemented until precise indices are provided in public domain and with robust history to inspire confidence. In India, neither data definitions are standardized nor is the methodology. The data is also collected by non-trained officials. The methodology of the RBI’s HPI is somewhat standardized but also has gaps. HPI only covers data collected from registration department of 9 cities but computes a national HPI based on that limited data set.” In a separate study, Singh compares India’s housing market with the United States and Spain and notes that there is need to have a well developed housing finance market in India.

From the Global Housing Watch Newsletter: September 2015

What’s happened to India’s housing market? There seems to be a slowdown and also a rising stock of unsold houses. This development has led to different views on India’s housing market. In a recent interview, Raghuram Rajan (Reserve Bank of India—RBI) said that “if real estate developers, who are sitting on unsold [housing] stocks, start bringing down prices, that will be a very big help to the sector because once there is a sense that the prices have stabilized more people will be willing to buy.

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, September 25, 2015

The Stekler Award for Courage in Forecasting (Recessions Inaccurately)

My presentation at the Federal Forecasters Conference summarized my work on the inability or unwillingness of forecasters to predict recessions. I also suggested that to get forecasters to predict recessions (even inaccurately) we should have a Stekler Award for Courage in Forecasting. The award would be in honor of noted forecaster Herman Stekler who says that forecasters should predict recessions early and often and that he himself has predicted 9 of the last 5 recessions. Read the full article…

Posted by at 2:00 PM

Labels: Forecasting Forum

Subscribe to: Posts