Monday, September 28, 2015

India’s Housing Market: What’s happened? What’s next?

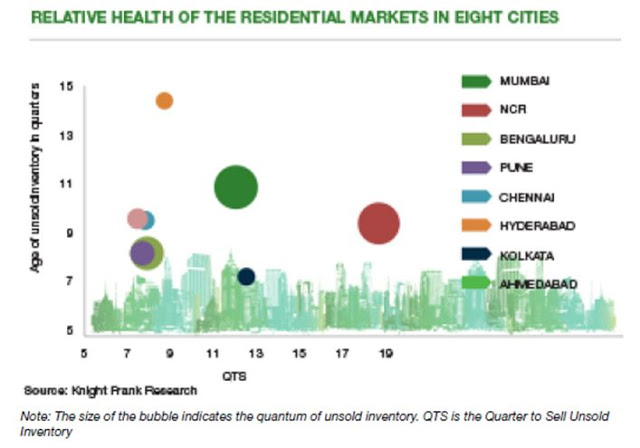

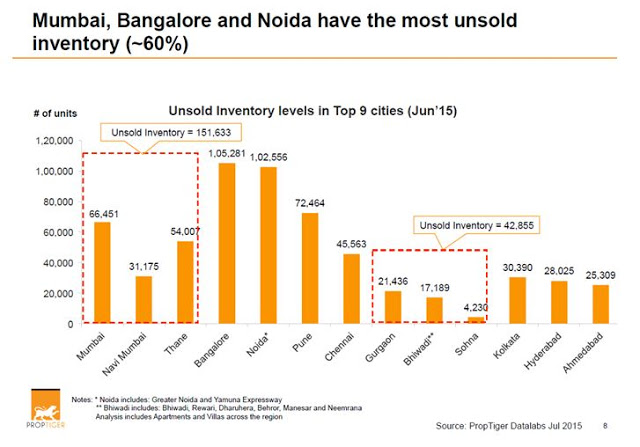

What’s happened to India’s housing market? There seems to be a slowdown and also a rising stock of unsold houses. This development has led to different views on India’s housing market. In a recent interview, Raghuram Rajan (Reserve Bank of India—RBI) said that “if real estate developers, who are sitting on unsold [housing] stocks, start bringing down prices, that will be a very big help to the sector because once there is a sense that the prices have stabilized more people will be willing to buy. (…) we also don’t want to create a situation where prices stay high at the level, which means demand can’t pick up (…)”. Similarly, the National Housing Bank (NHB) and Rayman Partners also agree that house prices are high. In terms of how long it will take to clear the housing inventory, Knight Frank says that “Mumbai has the highest number of unsold units in India (…). However, the NCR [National Capital Region] market will take the maximum time to liquidate its existing unsold inventory. At the current pace of sales, NCR will take more than four years to exhaust the unsold homes completely. Pune is currently the healthiest market, with the lowest QTS [quarters to sell unsold inventory] and a relatively lower age of unsold inventory”.

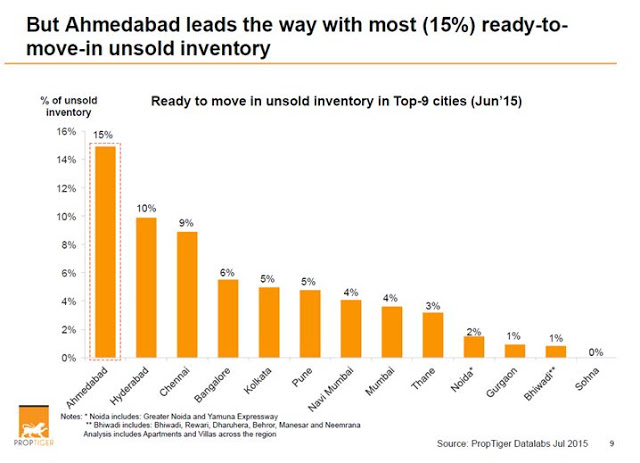

However, PropTiger and Farook Mahmood (Silverline Group and Chairman of NAR-India 7th Annual Convention) noted that when we talk about housing inventory data, we need to differentiate between the different types of inventory (e.g. ready-to-move-in vs. under-construction).

Also, the price of the unsold housing stock differs. For example, “69% of Mumbai’s unsold housing stock is priced above Rs. 1 Crore”, notes Ramesh Nair at Jones Lang LaSalle. Meanwhile, Irfan Razack (Prestige Group) stated that “(…) prices could come down only if the government reduced taxes related to property and ensured speedy approval of projects.” And Shashank Jain (PricewaterhouseCoopers) said “(…) developers were unlikely to drop base prices (…) if base prices were reduced, buyers may hold back purchases expecting more cuts in future. That would become counterproductive for the industry and economy.” Finally, a report by Ambit notes that there is “(…) a broad-based real estate pullback, with prices correcting in most tier I and tier II cities alongside sharp drops in transaction and new launch volumes. The drivers for this slowdown are a mix of supply-side factors (banks have pulled back lending to developers) and demand-side factors (the black money bill has created fear amongst speculators).”

What’s next for India’s housing market? “As the economic growth has started to take off, the overall buyer sentiment is expected to rise. Presumably, developers are counting on this to happen and hence holding the prices”, according to the RBI’s latest report. Meanwhile, PropTiger says that the housing market “(…) will soon be in better shape with the number of new launches likely to rise (…) when the festival season begins in October (…) the Q1 report predicts that the prices are not likely to fall in the near future.” On the unsold inventory, Knight Frank says that “(…) the unwinding process of the excess unsold inventory in these markets has already commenced since the first half of this year and (…) this process will continue for another six months in order to bring stability in the residential market. The deliberate slowdown in new launches undertaken by the real estate developer fraternity seems to be a pragmatic step in this direction and will hopefully lead the industry towards a path of sustainable development.” Finally, Shashank Jain says that “The inherent Indian demographics still makes the country’s real estate sector attractive. But if you are looking at short-term gains, then that continues to be a challenge (…) The long-term story is intact.”

More on India’s housing market. Charan Singh (Indian Institute of Management Bangalore) has studied the housing market in India. On India’s house price index, Singh notes that the NHB and RBI construct and release a house price index. But, there are a number of problems with both indices. NHB’s HPI “(…) is based on extensive data collected by different commercial banks and finance company located in 26 cities and is widely accepted in the country. Innovations that rely on data sources cannot be implemented until precise indices are provided in public domain and with robust history to inspire confidence. In India, neither data definitions are standardized nor is the methodology. The data is also collected by non-trained officials. The methodology of the RBI’s HPI is somewhat standardized but also has gaps. HPI only covers data collected from registration department of 9 cities but computes a national HPI based on that limited data set.” In a separate study, Singh compares India’s housing market with the United States and Spain and notes that there is need to have a well developed housing finance market in India.

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts