Monday, November 30, 2015

Canada’s Housing Market: Which Way Now?

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”, says Canada Mortgage and Housing Corporation (CMHC). When looking at the local level, CHMC notes that there is “strong overall evidence of problematic conditions in Toronto, Winnipeg, Saskatoon and Regina. In Toronto, strong evidence of problematic conditions reflects a combination of price acceleration and overvaluation. Strong evidence of problematic conditions in Winnipeg, Saskatoon, and Regina reflects detection of overvaluation and overbuilding.” The divergence in Canada’s housing market is also pointed out by Scotiabank and the Canadian Real Estate Association. On developments in the west part of Canada, CMHC is expecting to see more homeowners fall behind in their mortgage payments as a prolonged slump in oil prices hit household budgets. Finally, the OECD recently released a report warning that the “newly completed but unoccupied housing units have soared in Toronto, increasing the risk of a sharp market correction.” However, Benjamin Tal at CIBC says that the most widely used data on unabsorbed units overstates and misrepresents the level of condo inventory.

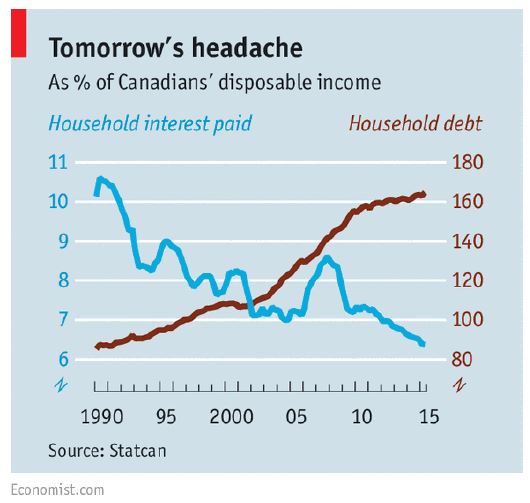

The views on household debt: “Consumer debt is a record 165% of disposable income. Most of that borrowing has gone into buying houses, which now look scarily overpriced”, says the Economist. TD Economics looked at the household debt issue in geographical terms. In doing so, TD Economics finds that “(…), financial vulnerability remains at elevated levels nationally. Households in British Columbia, Ontario and Alberta hold the top three spots, in that order. Households in these three provinces report having the highest debt-to-income ratios, devote the greatest share of income to making debt payments and have built up the highest degree of froth in their housing markets over the last decade.” Meanwhile, the Canadian Centre for Policy Alternatives looked at the household debt issues in terms of age group. It “(…) assesses the impact of a housing market correction on the net worth of Canadian families and finds a 20% decline in real estate prices would leave 169,000 families under 40 underwater, with more debts than assets.” However, the risk of household debt is not shared among the developers and builder community. A report by Ben Myers at Fortress Real Developments says: “The elevated level of household indebtedness in Canada is frequently cited as a vulnerability to the domestic economy, yet none of the builders and developers in our 2015 survey felt it was a significant risk to the housing market.” A new paper by the Central Bank of Canada finds “(…) that high and rising levels of both house prices and debt since the late-1990s can be mostly explained by movements in incomes, housing supply, mortgage interest rates and credit conditions, suggesting that the outlook for house prices and debt could depend mainly on the future paths of these variables.” A paper by Alan Walks (University of Toronto Mississauga) provides a picture of the emerging urban debtscape in Canadian cities, reflecting an essential element of the geography of risk and financialization. His research demonstrates that debt-related risk is associated with high and rising real estate values at each scale. Urban growth has thus brought with it significant new vulnerabilities, mainly related to housing costs and large mortgages, and this is particularly evident within Canada’s global cities.

Who is buying in the city of Vancouver? And how? New research by Andy Yan (Bing Thom Architects) looks at all the sales to occur within three west side neighborhoods in the City of Vancouver over a 6 month period and the ownership and mortgage patterns within these titles. There were a total of 172 transactions, with a total dwelling value of $525 million and with a starting price of $1.25 million and above. Here are some of the interesting findings: in terms of cash vs. mortgage, the study finds that 82 percent of the properties held a mortgage. In terms of ownership, 109 properties were listed with a single name and only 8 listed as corporation. In terms of occupations, 52 were listed as homemaker/housewife. And 66 percent of the 172 buyers had non-anglicized Chinese name. On a separate note, Tony Roy (BC Non-Profit Housing Association) says that nearly half of all renters are pouring more than 30 percent of their income into rent, while 24 percent in Metro Vancouver are spending more than half of their income on rent.

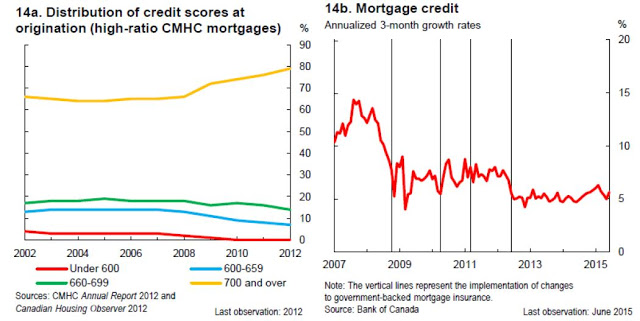

Macroprudential Policies: Are they working? More needed? According to the Central Bank of Canada, there have been four successive rounds of macroprudential tightening. The main target has been the rules for insured mortgages. For example, the maximum amortization period for insured loans has been shortened from 40 years to 25. Loan-to-value ratios have been lowered to 95 percent for new mortgages, and 80 percent for refinancing and investor properties. Qualification criteria such as limits on the total debt-service ratio and the gross debt-service ratio, as well as requirements for qualifying interest rates, have also been tightened.

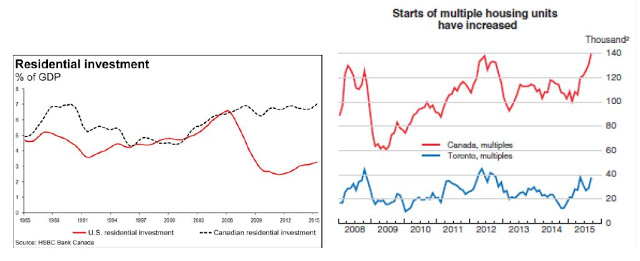

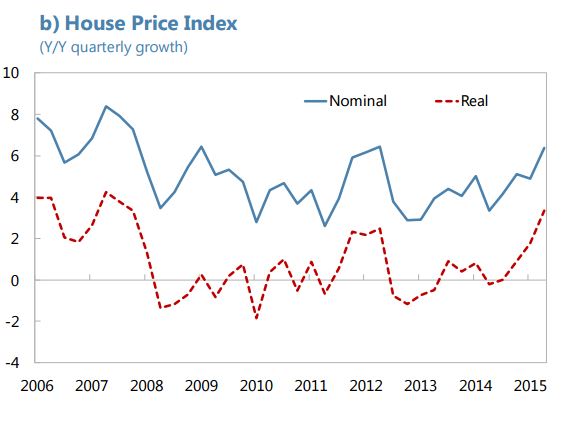

The measures taken have resulted in higher average credit scores, which have improved the quality of mortgage borrowing. With respect to household credit growth, the trend growth of mortgage credit declined from 14 percent in 2007–08 to around 5 percent in 2013–15. However, David Watt at HSBC Bank Canada says that there is a strong case for further macroprudential measures. He points out the trend in residential investment (see figure below on the left) and says that “the rise in residential investment as a percentage of GDP between 2002 and 2008 was in the backdrop of a generally rising terms of trade … With the terms of trade now worsening, it suggest that these trends should cool off, not accelerate.” Moreover, the OECD says that “(…) high household debt and strong price increases in some markets (single dwellings in Toronto and Vancouver) that are already expensive relative to fundamentals, further macro-prudential tightening on mortgage lending in these markets, such as maximum loan-to-value or debt-servicing ratios, should be implemented to ensure financial stability.”

From the Global Housing Watch Newsletter: November 2015

The views on the housing market: New research by National Bank Financial says that “There are now two housing markets in Canada.”

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”,

Posted by at 10:00 AM

Labels: Global Housing Watch

Sunday, November 29, 2015

Sovereign wealth funds in the new era of oil

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. The growth in the assets of their sovereign wealth funds, which were rising at a rapid rate until recently, is now slowing – and some have started drawing on their buffers.

Figure 1. Brent crude price, 2014-2015 (US dollars per barrel)

In the short run, this phenomenon is not cause for alarm. Most oil exporters have enough buffers to withstand a temporary drop in oil prices. But what will happen if low oil prices persist, and how will policymakers react? We explore here the fallout from low oil prices on sovereign wealth funds in oil-exporting countries and find that that they have important domestic implications. The impact on global asset prices will depend on the extent of unwinding of the sovereign wealth funds of oil exporters that will not be compensated by portfolio adjustment in other parts of the world that will in turn depend on their economic prospects.

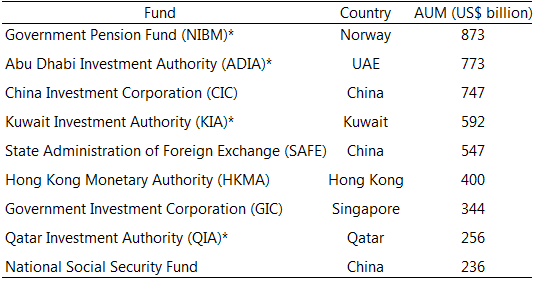

Figure 2. World’s biggest sovereign wealth funds, 2015 estimates

The rise of sovereign wealth funds

In the early 2000s, high oil prices brought about a massive redistribution of income to oil exporters, resulting in current account surpluses and a rapid buildup of foreign assets. Governments established new sovereign wealth funds or increased the size of existing ones to help manage the larger pool of financial assets. The total assets of sovereign wealth funds are concentrated in a few countries. As of March 2015, it is estimated at $7.3 trillion, of which $4.2 trillion are oil and gas related. While there are large differences across sovereign wealth funds, available information on their asset allocation points to a significant share in equities and bonds.

From Vox by Rabah Arezki, Adnan Mazarei, and Ananthakrishnan Prasad

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge,

Posted by at 11:49 AM

Labels: Energy & Climate Change

Tuesday, November 24, 2015

IMF’s Thanksgiving message: ensure benefits of foreign capital are shared broadly

“Davide Furceri and Prakash Loungani use an event-study framework — looking at what happens on average after clear changes in policy — to assess the effects of “neoliberal” policy changes (although they don’t put it that way) on inequality. Sure enough, they find that both fiscal austerity and liberalization of international capital movements are followed by noticeable rises in income inequality. So, if you were a ranting leftist, you might say that political attitudes are shaped by class, and that ideological justifications for high inequality are just a veil for class interest. You might also say that “sound” economic policies are really just policies that redistribute income upwards. And it turns out that the econometric evidence more or less supports your rant.”

Well, our evidence holds up to further scrutiny. And the conclusions we’d like you to draw from our work are summarized in our new blog. And then, if you really want to get a break from the in-laws, here’s the paper. Nothing clears the living room better than a statement like “Guys, let me tell you about this fascinating paper – its findings do not imply that countries should not undertake capital account liberalization, but it suggests an additional reason for caution.”

Happy Thanksgiving,

Prakash

Opening up capital markets, unless managed well, can raise inequality. That’s the message of a new working paper by Davide Furceri and me that the IMF released today. Paul Krugman, based on the early evidence from our work, wrote:

“Davide Furceri and Prakash Loungani use an event-study framework — looking at what happens on average after clear changes in policy — to assess the effects of “neoliberal” policy changes (although they don’t put it that way) on inequality.

Posted by at 8:34 PM

Labels: Inclusive Growth

Saturday, November 21, 2015

Forecasting: Who keeps the score?

Superforecasting: The Art and Science of Prediction. By Philip Tetlock and Dan Gardner. Crown; 352 pages; $28.

Here are four forecasts that have been made in the technology field. First: “There is no reason anyone would want a computer in their home”, this was a forecast made in 1977 by Ken Olson—the president of Digital Equipment Corporation. Second: “There’s no chance that the iPhone is going to get any significant market share. No chance”, that was the forecast made in 2007 by Steve Ballmer—CEO of Microsoft. Third: “In five years I don’t think there’ll be a reason to have a tablet anymore”, forecast made in 2013 by Thorsten Heins—CEO of BlackBerry. Fourth: “Yes, the iPad Pro is a replacement for a notebook or a desktop for many, many people. They will start using it and conclude they no longer need to use anything else, other than their phones”, this forecast was made few weeks ago by Tim Cook—CEO of Apple. In the first three cases, it is safe to say that we know the outcome. In the last case, we will have to wait and see.

Can ordinary people also make forecasts? Who keeps the score of all the forecasts that are made? Why keeping the score matters? What is needed in the forecasting field? Can we do better at forecasting? These are some of the questions that are discussed in a fascinating new book: Superforecasting: The Art and Science of Prediction by Philip E. Tetlock and Dan Gardner. Tetlock is a professor at the University of Pennsylvania and Gardner is a journalist, author, and a lecturer.

The new book by Tetlock and Gardner describes the results from a massive forecasting tournament—the Good Judgment Project—sponsored by Intelligence Advanced Research Projects Activity (IARPA). The idea behind the project was to see who could invent the best methods of making forecasts that intelligence analysts make every day. The participants were asked to make a forecast on different topics. Some of the topics included were: Will OPEC agree to cut its oil output at or before its November 2014 meeting? Will the president of Tunisia flee to a cushy exile in the next month? Will the gold price exceed $1,850 on September 30, 2011? Will the euro fall below $1.20 in the next twelve months? The project recruited a very high number of volunteers. These volunteers came from a very wide range of backgrounds: from retired computer programmer, social service worker, to a homemaker. Below are some of the interesting parts of the book.

Can ordinary people also make forecasts? Here is one example from the forecasting tournament: “With his gray beard, thinning hair, and glasses, Doug Lorch doesn’t look like a threat to anyone. He looks like a computer programmer, which he was, for IBM. He is retired now. (…) Doug likes to drive his little red convertible Miata around the sunny streets, enjoying the California breeze, but that can only occupy so many hours in the day. Doug has no special expertise in international affairs, but he has a healthy curiosity about what’s happening. He reads the New York Times. He can find Kazakhstan on a map. So he volunteered for the Good Judgment Project. Once a day, for an hour or so, his dinning room table became his forecasting center, where he opened his laptop, read the news, and tried to anticipate the fate of the world. (…) In year 1 alone, Doug Lorch made roughly one thousand separate forecasts. Doug’s accuracy was as impressive as his volume (…) putting him in fifth spot among the 2,800 competitors in the Good Judgment Project. (…) In year 2, Doug joined a superforecaster team and did even better, (…) making him the best forecaster of the 2,800 GJP volunteers. (…) This is a man with no applicable experience or education, and no access to classified information. The only payment he received was the $250 Amazon gift certificate that all volunteers got at the end of each season. Doug Lorch was (…) so good at it that there wasn’t a lot of room for an experienced intelligence analyst with a salary, a security clearance, and a desk in CIA headquarters to do better. Someone might ask why the United States spends billions of dollars every year on geopolitical forecasting when it could give Doug a gift certificate and let him do it.”

Who keeps the score of all the forecasts that are made? “More often forecasts are made and then … nothing. Accuracy is seldom determined after the fact and is almost never done with sufficient regularity and rigor that conclusions can be drawn. The reason? Mostly it’s a demand-side problem: The consumers of forecasting—governments, business, and the public—don’t demand evidence of accuracy. So there is no measurement. Which means no revision. And without revision, there can be no improvement.”

Why keeping the score matters? “With scores and leaderboards, forecasting tournaments may look like games but the stakes are real and substantial. In business, good forecasting can be the difference between prosperity and bankruptcy; in government, the difference between policies that give communities a boost and those that inflict unintended consequences and waste tax dollars; in national security, the difference between peace and war. If the US intelligence community had not told Congress it was certain that Saddam Hussein had weapons of mass destruction, a disastrous invasion might have been averted.”

What is needed in the forecasting field? “For centuries, it hobbled progress in medicine. When physicians finally accepted that their experience and perceptions were not reliable means of determining whether a treatment works, they turned to scientific testing—and medicine finally started to make rapid advances. The same revolution needs to happen in forecasting.”

Can we do better at forecasting? “(…) it turns out that forecasting is not you have it or you don’t talent. It is a skill that can be cultivated.” Here are some tips for aspiring superforecasters: “Break seemingly intractable problems into tractable sub-problems (…) Strike the right balance between inside and outside views (…) Strike the right balance between under- and overreacting to evidence (…) Don’t treat commandments as commandments.”

My colleague Hites Ahir has a review and summary of Superforecasting

Superforecasting: The Art and Science of Prediction. By Philip Tetlock and Dan Gardner. Crown; 352 pages; $28.

Here are four forecasts that have been made in the technology field. First: “There is no reason anyone would want a computer in their home”, this was a forecast made in 1977 by Ken Olson—the president of Digital Equipment Corporation.

Posted by at 7:43 PM

Labels: Forecasting Forum

Friday, November 20, 2015

House Prices in Mexico

“House prices have been broadly stable in real terms since 2008, and there are no signs of a real estate bubble”, says IMF’s new report on Mexico.

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts