Monday, November 30, 2015

Canada’s Housing Market: Which Way Now?

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”, says Canada Mortgage and Housing Corporation (CMHC). When looking at the local level, CHMC notes that there is “strong overall evidence of problematic conditions in Toronto, Winnipeg, Saskatoon and Regina. In Toronto, strong evidence of problematic conditions reflects a combination of price acceleration and overvaluation. Strong evidence of problematic conditions in Winnipeg, Saskatoon, and Regina reflects detection of overvaluation and overbuilding.” The divergence in Canada’s housing market is also pointed out by Scotiabank and the Canadian Real Estate Association. On developments in the west part of Canada, CMHC is expecting to see more homeowners fall behind in their mortgage payments as a prolonged slump in oil prices hit household budgets. Finally, the OECD recently released a report warning that the “newly completed but unoccupied housing units have soared in Toronto, increasing the risk of a sharp market correction.” However, Benjamin Tal at CIBC says that the most widely used data on unabsorbed units overstates and misrepresents the level of condo inventory.

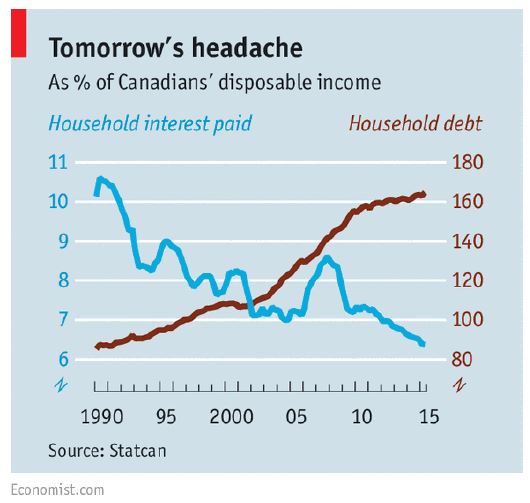

The views on household debt: “Consumer debt is a record 165% of disposable income. Most of that borrowing has gone into buying houses, which now look scarily overpriced”, says the Economist. TD Economics looked at the household debt issue in geographical terms. In doing so, TD Economics finds that “(…), financial vulnerability remains at elevated levels nationally. Households in British Columbia, Ontario and Alberta hold the top three spots, in that order. Households in these three provinces report having the highest debt-to-income ratios, devote the greatest share of income to making debt payments and have built up the highest degree of froth in their housing markets over the last decade.” Meanwhile, the Canadian Centre for Policy Alternatives looked at the household debt issues in terms of age group. It “(…) assesses the impact of a housing market correction on the net worth of Canadian families and finds a 20% decline in real estate prices would leave 169,000 families under 40 underwater, with more debts than assets.” However, the risk of household debt is not shared among the developers and builder community. A report by Ben Myers at Fortress Real Developments says: “The elevated level of household indebtedness in Canada is frequently cited as a vulnerability to the domestic economy, yet none of the builders and developers in our 2015 survey felt it was a significant risk to the housing market.” A new paper by the Central Bank of Canada finds “(…) that high and rising levels of both house prices and debt since the late-1990s can be mostly explained by movements in incomes, housing supply, mortgage interest rates and credit conditions, suggesting that the outlook for house prices and debt could depend mainly on the future paths of these variables.” A paper by Alan Walks (University of Toronto Mississauga) provides a picture of the emerging urban debtscape in Canadian cities, reflecting an essential element of the geography of risk and financialization. His research demonstrates that debt-related risk is associated with high and rising real estate values at each scale. Urban growth has thus brought with it significant new vulnerabilities, mainly related to housing costs and large mortgages, and this is particularly evident within Canada’s global cities.

Who is buying in the city of Vancouver? And how? New research by Andy Yan (Bing Thom Architects) looks at all the sales to occur within three west side neighborhoods in the City of Vancouver over a 6 month period and the ownership and mortgage patterns within these titles. There were a total of 172 transactions, with a total dwelling value of $525 million and with a starting price of $1.25 million and above. Here are some of the interesting findings: in terms of cash vs. mortgage, the study finds that 82 percent of the properties held a mortgage. In terms of ownership, 109 properties were listed with a single name and only 8 listed as corporation. In terms of occupations, 52 were listed as homemaker/housewife. And 66 percent of the 172 buyers had non-anglicized Chinese name. On a separate note, Tony Roy (BC Non-Profit Housing Association) says that nearly half of all renters are pouring more than 30 percent of their income into rent, while 24 percent in Metro Vancouver are spending more than half of their income on rent.

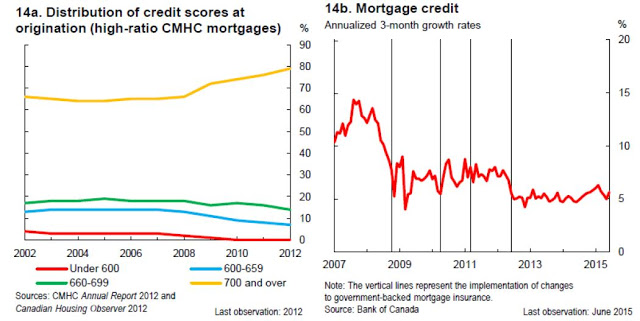

Macroprudential Policies: Are they working? More needed? According to the Central Bank of Canada, there have been four successive rounds of macroprudential tightening. The main target has been the rules for insured mortgages. For example, the maximum amortization period for insured loans has been shortened from 40 years to 25. Loan-to-value ratios have been lowered to 95 percent for new mortgages, and 80 percent for refinancing and investor properties. Qualification criteria such as limits on the total debt-service ratio and the gross debt-service ratio, as well as requirements for qualifying interest rates, have also been tightened.

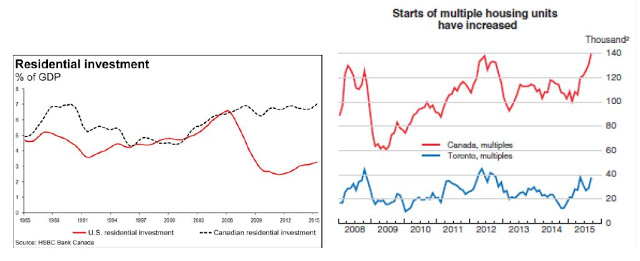

The measures taken have resulted in higher average credit scores, which have improved the quality of mortgage borrowing. With respect to household credit growth, the trend growth of mortgage credit declined from 14 percent in 2007–08 to around 5 percent in 2013–15. However, David Watt at HSBC Bank Canada says that there is a strong case for further macroprudential measures. He points out the trend in residential investment (see figure below on the left) and says that “the rise in residential investment as a percentage of GDP between 2002 and 2008 was in the backdrop of a generally rising terms of trade … With the terms of trade now worsening, it suggest that these trends should cool off, not accelerate.” Moreover, the OECD says that “(…) high household debt and strong price increases in some markets (single dwellings in Toronto and Vancouver) that are already expensive relative to fundamentals, further macro-prudential tightening on mortgage lending in these markets, such as maximum loan-to-value or debt-servicing ratios, should be implemented to ensure financial stability.”

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts