Friday, February 3, 2017

Housing Market in Turkey

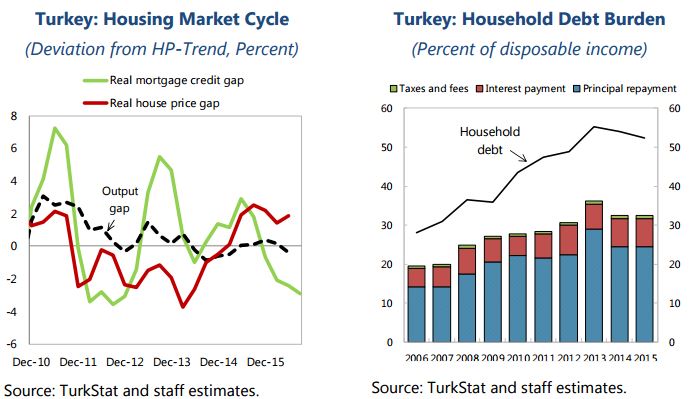

Below is an extract from the IMF’s latest report on Turkey:

“Turkish house prices have been markedly increasing for several years. The prices for homes rose cumulatively by 110 percent in nominal and 35 percent in real terms between end-2010 and July 2016. Valuation appears stretched by a number of metrics, such as price-to-income and price-to-rent ratios. The burden of household debt has also increased.

Demographic and socio-economic factors underpin the strong demand for housing. A young and rapidly growing population combined with a high and rising rate of urbanization drive demand for residential housing. In addition, the number of households has increased with a decline in average household size. Household preferences have also shifted toward newer and larger houses, with stronger construction codes.

Special sales campaigns and government stimulus have buoyed house sales since July 2016. The government launched a campaign for subsidized sales of 60,000 houses with mortgages offered at below-market lending rates and higher LTV ratios than the regulatory ceiling, in addition to applying moral suasion on banks to lower mortgage rates. Following the adoption of these measures, total house sales rose by 2 percent year-on-year in August. Since then, the LTV ceiling was raised from 75 to 80 percent.”

Also see a separate IMF report on Understanding Turkish Residential Real Estate Dynamics.

Below is an extract from the IMF’s latest report on Turkey:

“Turkish house prices have been markedly increasing for several years. The prices for homes rose cumulatively by 110 percent in nominal and 35 percent in real terms between end-2010 and July 2016. Valuation appears stretched by a number of metrics, such as price-to-income and price-to-rent ratios. The burden of household debt has also increased.

Posted by at 4:47 PM

Labels: Global Housing Watch

Thursday, February 2, 2017

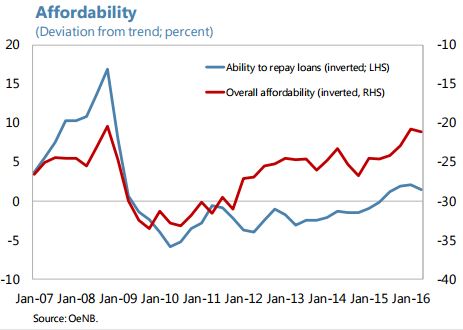

House Prices in Austria

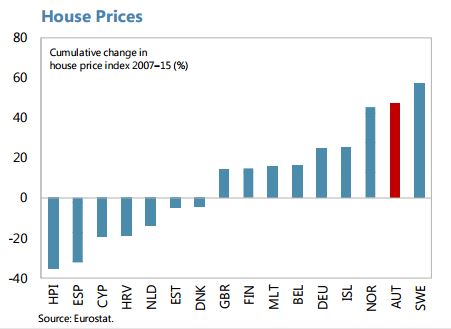

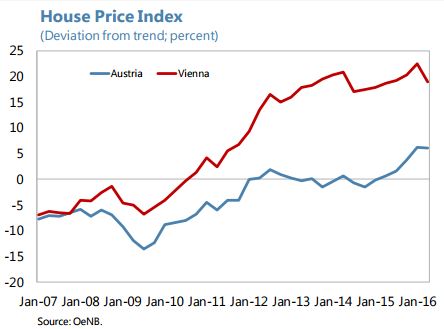

The IMF’s latest economic report on Austria points out that:

“House price growth has been strong in recent years by international comparisons. The cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna, while prices in the rest of the country appear broadly in line with fundamentals. Price increases in Vienna have moderated lately, while picking up in the rest of the country (…). Low interest rates over recent years have loosened credit constraints and increased households’ borrowing capacity, putting upward pressure on housing demand. That said, prices have been kept high by supply side constraints and other idiosyncratic factors, especially in Vienna. Reviewing and relaxing local planning systems and regulations to facilitate the supply response to price movement can help contain the price rises close to the long run trend. Are the rising prices a problem? Financial stability risks seem contained. (…) Nonetheless, the authorities need to have the legal authority to expand the macroprudential toolkit with real estate-specific instruments when needed, to limit any potential risks to banks’ portfolios if real estate price bubbles were to emerge.”

The IMF’s latest economic report on Austria points out that:

“House price growth has been strong in recent years by international comparisons. The cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna,

Posted by at 1:19 PM

Labels: Global Housing Watch

Groundhog Day Tradition: 2017 Stekler Award for Courage in Forecasting

This year’s award is shared by Allan Lichtman and Helmut Norpoth, two political scientists, who forecasted a Trump victory in the U.S. Presidential elections. Though I started out giving the award to people who had the courage to forecast recessions, I think it is good to broaden it to recognize courageous forecasts in other areas. Both Lichtman and Norpoth described the basis on which they were making their forecasts, which is an essential consideration in who gets the award. Outrageous forecasts made without providing some reasoning don’t qualify. The 2016 award went to Michael Shedlock (“Mish”) and the inaugural 2015 award to Lakshman Achuthan.

This year’s award is shared by Allan Lichtman and Helmut Norpoth, two political scientists, who forecasted a Trump victory in the U.S. Presidential elections. Though I started out giving the award to people who had the courage to forecast recessions, I think it is good to broaden it to recognize courageous forecasts in other areas. Both Lichtman and Norpoth described the basis on which they were making their forecasts, which is an essential consideration in who gets the award.

Posted by at 9:00 AM

Labels: Forecasting Forum

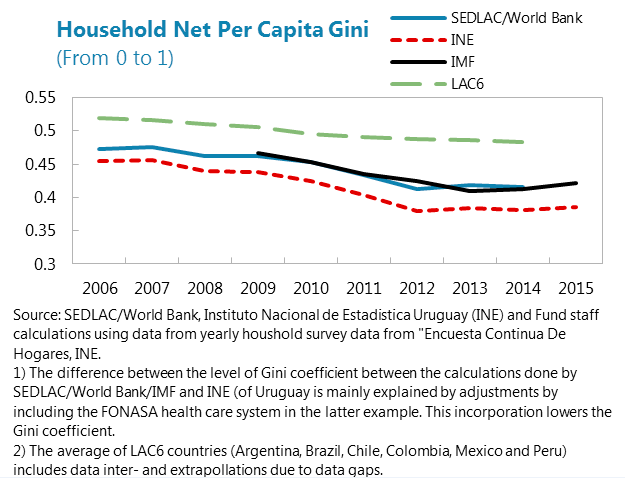

Increased Social Inclusion in Uruguay– the Role of Government Policies

A new IMF report analyzes the lowering of the Gini coefficient in Uruguay during the last six years. Social policies and transfers have played a significant role in reducing poverty and inequality. While income dispersion has decreased across Latin America over the last decade, Uruguay stands out as the country with the largest drop in the Gini coefficient between 2009 and 2014, and to the lowest level. This reflects both government guidelines to bolster low wages, and increased redistribution through income taxes and transfers. However, looking ahead, the positive effects of further redistributive policies may be weighed against their fiscal costs and by a possible trade-off between income compression and incentives for labor supply and education and training. Work incentives among women can be strengthened further via reforms of parental leave, to reduce the remaining gender wage gap, and would diminish future pressures on public finances due to population ageing.

A new IMF report analyzes the lowering of the Gini coefficient in Uruguay during the last six years. Social policies and transfers have played a significant role in reducing poverty and inequality. While income dispersion has decreased across Latin America over the last decade, Uruguay stands out as the country with the largest drop in the Gini coefficient between 2009 and 2014, and to the lowest level. This reflects both government guidelines to bolster low wages,

Posted by at 8:42 AM

Labels: Inclusive Growth

Tuesday, January 31, 2017

The Fruits of Growth: Economic Reforms and Lower Inequality

New IMF work on inequality was showcased by IMF Managing Director Christine Lagarde in an iMFdirect post:

“Growth is essential for improving the lives of people in low-income countries, and it should benefit all parts of society.

Traveling through Africa in the last few days, I have been amazed by the vitality I have witnessed: business startups investing in the future, new infrastructure under construction, and a growing middle class. Many Africans are now making a better living and fewer are suffering from poverty. My current host, Uganda, for example, has more than halved its absolute poverty rate to about 35 percent from close to 90 percent in 1990.

But we have also seen a flip side. Poverty, of course, but inequality as well remain stubbornly high in most developing countries, including in Africa, and too often success is not shared by all.

We have learned, both from working with our member countries, and from our research, that sharing the fruits of growth—what we call inclusion—is key to achieving sustainable economic growth. All segments of society should feel that they have an opportunity to make a better life for themselves.

Our new staff analysis, released today, uncovers the various channels through which critical reforms that promote growth (such as those in agriculture, the financial sector, and public investment) can sometimes widen inequality in lower-income countries. The study also illustrates how additional measures can mitigate such growth and equality trade-offs.

The bottom line is this: First, pro-growth policies can be truly inclusive only if policies are designed with careful attention to the details of who gains and who loses. Second, well-targeted measures can ensure that everyone gains from essential economic reforms—and help further strengthen the case for pursuing reforms.

A look at who gains and loses

Lifting growth and reducing inequality is especially hard in countries where workers cannot relocate easily and there are big productivity differences between services, industry, and agriculture. A large informal economy, poor infrastructure and lack of financial services make the task even more difficult. Yet, in many of the IMF’s poorest member countries, this is often the case.

In sub-Saharan Africa, for example, it is more than twice as expensive to move from rural to urban areas than it is in China. Only a third of sub-Saharan African households have electricity, compared to 85 percent in the rest of the world. And in low-income countries, only about 20 percent of the adult population has a bank account, compared to more than 80 percent in the rest of the world.

Such barriers get in the way of successful and equitable reforms. Infrastructure development and financial sector reforms are examples.

More, and more efficient, spending on roads, airports, power grids and education help an economy grow more productive and make it easier for people to relocate from farms to cities. But infrastructure investment can also increase inequality if some sectors of the economy become more competitive than others, particularly if labor mobility is limited.

The case is similar for financial sector reforms. On the positive side, these reforms could make it cheaper to borrow, thereby stimulating private investment and boosting growth. But unless financial reforms are deep enough, they may not help poorer segments of the population obtain access to credit and financial services.

How to deliver strong, but inclusive growth

So, what can be done? The answer is not for policymakers to hold off on reforms that boost productivity and growth. Rather, policymakers should consider options that make these reforms more palatable from both a growth and distributional perspective.

With this in mind, our staff paper looks at a number of country cases and analyzes how well-targeted measures can complement reforms and offset adverse distributional impact.

For instance, if Malawi were to consider reducing subsidies for maize production to enhance productivity in the agricultural sector, then targeted cash transfers to affected households would help provide immediate support to farmers who may be hurt by this move. This approach has been successful in reducing poverty and inequality in countries such as Ethiopia, which has one of the largest social transfer programs in Africa.

Similarly, with regard to financial sector reform, if Ethiopia were to increase credit to the private sector to promote manufacturing and boost growth and employment, complementing this by broadening financial access to the rural population and increasing labor mobility—through easier transport that connect rural and urban areas, affordable urban housing, and training—would help reduce inequality across sectors. Rural workers would then be able to find better paying jobs in more modern and competitive sectors, such as manufacturing and services.

Governments can also target investment to improve productivity in disadvantaged sectors, and even out the impact of other reforms. In Myanmar, for example, where half the workforce is on farms, investment in electrification, irrigation, and research and development for improved seed varieties could sharply improve agricultural productivity.

There is no doubt that governments will face challenges in building a consensus for bold policies to boost growth. The IMF will continue to work with them, advocating reforms that bear fruits for everybody to enjoy.”

New IMF work on inequality was showcased by IMF Managing Director Christine Lagarde in an iMFdirect post:

“Growth is essential for improving the lives of people in low-income countries, and it should benefit all parts of society.

Traveling through Africa in the last few days, I have been amazed by the vitality I have witnessed: business startups investing in the future,

Posted by at 8:58 AM

Labels: Inclusive Growth

Subscribe to: Posts