Saturday, January 6, 2018

Growth-Equity Trade-offs in Structural Reforms

From a new IMF working paper by Jonathan Ostry, Andrew Berg, and Siddharth Kothari:

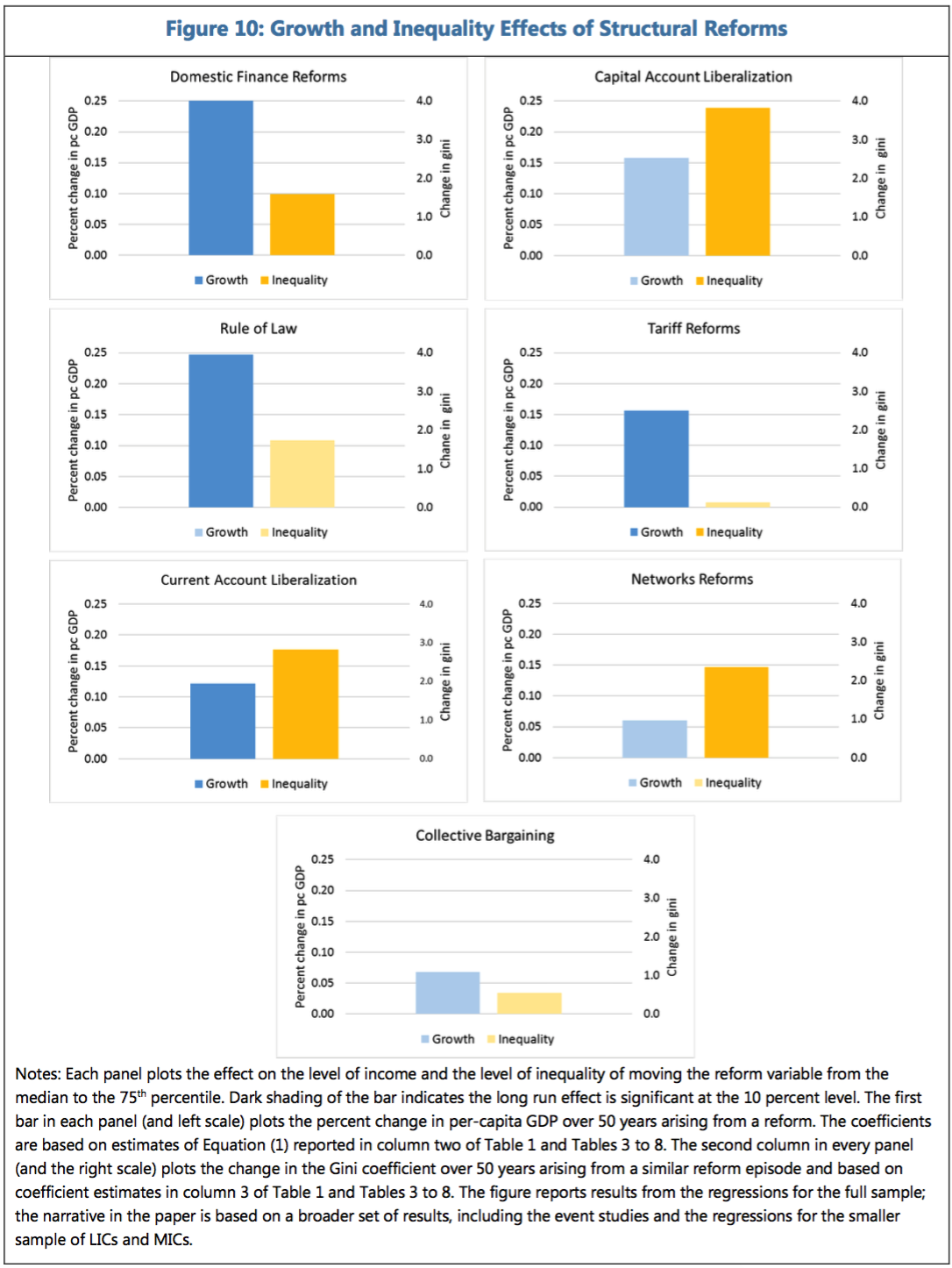

“Do structural reforms that aim to boost potential output also change the distribution of income? We shed light on this question by looking at the broad patterns in the cross-country data covering advanced, emerging-market, and low-income countries. Our main finding is that there is indeed evidence of a growth-equity tradeoff for some important reforms. Financial and capital account liberalization seem to increase both growth and inequality, as do some measures of liberalization of current account transactions. Reforms aimed at strengthening the impartiality of and adherence to the legal system seem to entail no growth-equity tradeoff—such reforms are good for growth and do not worsen inequality. The results for our index of network reforms as well as our measure of the decentralization of collective labor bargaining are the weakest and least robust, potentially due to data limitations. We also ask: If some structural reforms worsen inequality, to what degree does this offset the growth gains from the reforms themselves? While higher inequality does dampen the growth benefits, the net effect on growth remains positive for most reform indicators.”

From a new IMF working paper by Jonathan Ostry, Andrew Berg, and Siddharth Kothari:

“Do structural reforms that aim to boost potential output also change the distribution of income? We shed light on this question by looking at the broad patterns in the cross-country data covering advanced, emerging-market, and low-income countries. Our main finding is that there is indeed evidence of a growth-equity tradeoff for some important reforms. Financial and capital account liberalization seem to increase both growth and inequality,

Posted by at 8:28 AM

Labels: Inclusive Growth

Friday, January 5, 2018

Housing View – January 5, 2018 [2018 AEA Annual Meeting Special Edition]

On international house pricing:

- Measuring House Prices in the Long Run: Insights from Dublin, 1900-2015 – AEA

- A Tale of Two Countries: Comparing Booms, Busts and Bubbles in the United States and Chinese Housing Markets – Paper

- Analyzing the Changes in the Distribution of House Prices in Beijing – AEA

- Locally Weighted Quantile House Price Indices and Distribution in Japanese Cities, 1986 – AEA

- Do Airbnb Properties Affect House Prices? – Paper

- The Sharing Economy and Housing Affordability: Evidence from Airbnb – Paper

- Think Globally, Aggregate Locally: Index Consistency in the Presence Asymmetric Appreciation – Paper

- S. Metropolitan House Price Dynamics – Paper

- Did Investors Price Regional Housing Bubbles? A Tale of Two Markets – Paper

- Monetary Policy and the Housing Market – Paper

- Teardowns, Popups and Bump-outs: What Do Building Permits Say About Housing Supply? – Paper

- House Price Beliefs and Leverage Choice – Paper

- Do Gasoline Prices Affect Residential Property Values? – Paper

- Bank Risk-taking and the Real Economy: Evidence From the Housing Boom and its Aftermath – AEA

- Do Financial Constraints Cool a Housing Boom? Theory and Evidence From a Macroprudential Policy on Million Dollar Homes – Paper

- Housing Appreciation and Marginal Land Supply in Monocentric Cities with Topography – Paper

- Prospect Theory, Reverse Disposition Effect and the Housing Market – Paper

- How Do Households Discount Over Centuries? Evidence From Singapore’s Private Housing Market – Paper

- Property Right Restriction and House Prices – Paper and Presentation

- Cyclical Housing Prices in Flatland – Paper and Presentation

- House Prices, Mortgage Debt and Labor Mobility – AEA

- Model-Free Estimation of the Hedonic Price for Housing Space – Paper

On household finance:

- Household Finance and Consumer Behavior – Paper

- The Housing Crisis and the Rise in Student Loans – Paper

- Home Equity and the Timing of Claiming Social Security Retirement Income – AEA

- The Effect of Debt on Default and Consumption: Evidence From Housing Policy in the Great Recession – Paper

- Housing Wealth Effects: The Long View – Paper

On mortgages:

- Time to Homeownership and Mortgage Design: Income Sharing and Saving Incentive – Paper

- The Effect of Changing Mortgage Payments on Default and Prepayment: Evidence From HAMP Resets – Paper and Presentation

- The Effect of Interest Rates on Home Buying: Evidence From a Discontinuity in Mortgage Insurance Premiums – Paper and Presentation

- Liquidity Provision, Credit Risk and the Bond Spread: New Evidence From the Subprime Mortgage Market – Paper

- Collateral Damage: The Impact of Shale Gas on Mortgage Lending – Paper

- Are Mortgage Regulations Affecting Entrepreneurship? – Paper

- Eyes Wide Shut? Mortgage Insurance During the Housing Boom – AEA

- Effects of FHA Loan Limit Increases by ESA 2008: Housing Demand and Adverse Selection – AEA

- The Macroeconomic Effect of Government Asset Purchases: Evidence From Post-war United States Housing Credit Policy – Paper and Presentation

- How Much Are Car Purchases Driven by Home Equity Withdrawal? – Paper

- How Home Equity Extraction and Reverse Mortgages Affect the Credit Outcomes of Senior Households – AEA

- An Empirical Study of Termination Behavior of Reverse Mortgages – Paper

- Mortgage Default with Positive Equity – Paper

- Lending Competition and Non-Traditional Mortgages – Paper

On behavioral real estate:

- How Do the CEO Political Leanings Affect REIT Business Decisions? – Paper

- Outshine to Outbid: Weather-induced Sentiments on Housing Market – Paper and Presentation

- Contact High: The External Effects of Retail Marijuana Establishments on House Prices – AEA

- Relational Contracts, Reputational Concerns, and Appraiser Behavior: Evidence from the Housing Market – Paper

On affordable housing:

- Neighbors and Networks: The Role of Social Interactions on the Residential Choices of Housing Choice Voucher Holders – Paper

- Neighborhood Choices, Neighborhood Effects and Housing Vouchers – AEA

- Waiting for Affordable Housing – Paper

- Long-Run Outcomes of HOPE VI Public Housing Demolitions for Children – AEA

- The Effects of Residential Evictions on Low-Income Adults – Paper

On property taxes:

- Greener on the Other Side? Spatial Discontinuities in Property Tax Rates and their Effects on Tax Morale – AEA

- The Hated Property Tax: Salience, Tax Rates, and Tax Revolts – AEA

- Measuring Both Direct and Spillover Effects of Taxation: Evidence From a Property Tax Break for First-Time Buyers – Paper

- Impact of Housing Tax Preferences on Home Values and Neighborhood Sorting – AEA

- Do Local Governments Tax Homeowner Communities Differently? – Paper

On agency and bargaining:

- Why Disclose Less Information? Toward Resolving a Disclosure Puzzle in the Housing Market – Paper

- Examining Both Sides of the Transaction: Bargaining in the Housing Market – Paper

- Investor Bargaining Power, Rental Externalities and Housing Prices – Paper

- When are Real Estate Flippers Smarter Than the Crowd? – Paper

On homeownership:

- African-American Mayors, Home Ownership and Mortgage Lending in US Cities – Paper

- Do Homeowners Save More Than Renters? Evidence From the Panel on Household Finances – Paper and Presentation

- Home Sweet Home: (Mis-)Beliefs About the Extent to Which Home Ownership Makes People Happy – Paper

- Job Separation Risk and Home Ownership: Evidence From Assistant Professors – AEA

- Identifying the Benefits from Home Ownership: A Swedish Experiment – Paper

- Owned Now Rented Later? Housing Stock Transitions and Market Dynamics – Paper

- Diverted Homeowners and Rental Affordability – AEA

- School Quality, Latent Demand, and Bidding Wars for Houses – AEA

- Wage Trickle Down vs. Rent Trickle Down: How Does Increase in College Graduates Affect Wages and Rents? – AEA

Photo by Aliis Sinisalu

On international house pricing:

- Measuring House Prices in the Long Run: Insights from Dublin, 1900-2015 – AEA

- A Tale of Two Countries: Comparing Booms, Busts and Bubbles in the United States and Chinese Housing Markets – Paper

- Analyzing the Changes in the Distribution of House Prices in Beijing – AEA

- Locally Weighted Quantile House Price Indices and Distribution in Japanese Cities,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 4, 2018

Okun’s Law in Russia

A new paper concludes that “Okun’s law is applicable in Russia.” “The economic connection between economic growth rates and changes in unemployment proposed by Okun (1962) over half a century ago remains one of the main tools for analyzing labor markets.”

“Gabrisch and Buscher (2006) proposed that the formation of the labor market mechanism in the formerly planned economies could be considered as completed once Okun’s law became persistently applicable there.”

“The general conclusion is that Okun’s law is applicable in Russia both in the short and long run. A comparison (Akhundova et al., 2005) has shown that transition processes in the Russian labor market were completed during the first half of the 2000s (i.e., the shaping of the labor market mechanisms took slightly more than 10 years).”

The article is available from the Russian Journal of Economics.

A new paper concludes that “Okun’s law is applicable in Russia.” “The economic connection between economic growth rates and changes in unemployment proposed by Okun (1962) over half a century ago remains one of the main tools for analyzing labor markets.”

“Gabrisch and Buscher (2006) proposed that the formation of the labor market mechanism in the formerly planned economies could be considered as completed once Okun’s law became persistently applicable there.”

“The general conclusion is that Okun’s law is applicable in Russia both in the short and long run.

Posted by at 10:42 AM

Labels: Inclusive Growth

GDP growth forecasts and information flows: Is there evidence of overreactions?

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories. In addition to these warnings, further motivation is provided by macroeconomic episodes in which improved economic prospects are followed by crises. For instance, several European economies, among them Greece and Ireland, went through this type of trajectory. Another case is given by recent events in Brazil, where prominent optimism regarding economic prospects was later proven wrong in a stark manner.”

“The empirical analysis shows a significant association between mean forecast errors and earlier information flows. The sign of the documented relationship is consistent with the overreaction hypothesis. More positive information is followed, on average, by higher forecast errors, that is, by increments in the mean difference between forecast growth and realized growth.”

“It is worth noting that the strongest evidence is documented for information flows and forecasts errors that are between 4 and 8 years apart. In other words, the evidence indicates the presence of a process that develops at a frequency that is lower than the usual business cycle frequency.”

“This work documents the presence of systematic errors in growth forecasts. Mean forecast errors are positively associated with the tone of information flows observed in previous periods.”

“The inefficient use of information and the associated errors in decision-making could explain economically significant aggregate fluctuations. In particular, excessive optimism after the arrival of positive information can contribute to the emergence of vulnerabilities that increase the likelihood of economic crises.”

The article is available from the International Finance.

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories.

Posted by at 10:41 AM

Labels: Forecasting Forum

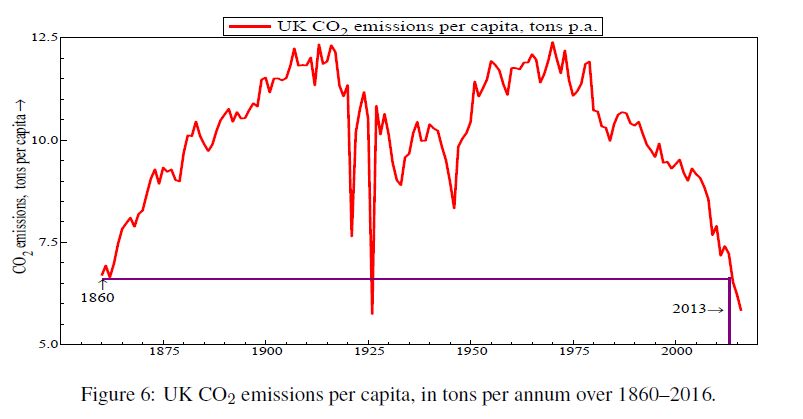

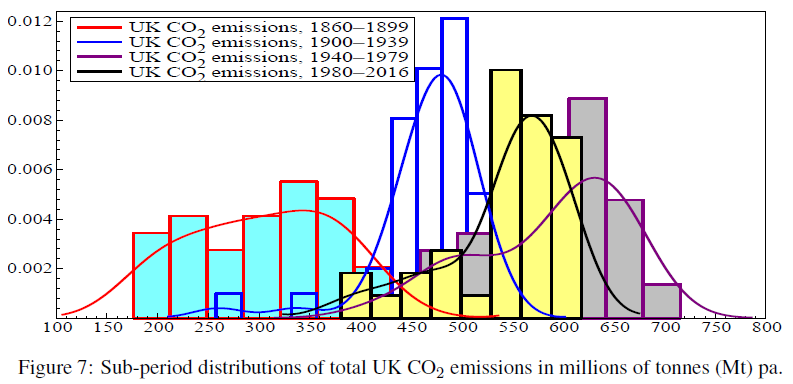

CO2 Emissions in UK

Hendry reports per capita UK CO2 emissions, “which rose considerably till 1916, fluctuated violently till 1950, and have dropped dramatically since 1970” (see Hendry, 2017b).

“The sub-period distributions of UK CO2 emissions in [the figure below] illustrate their changes in shape, spread and location.”

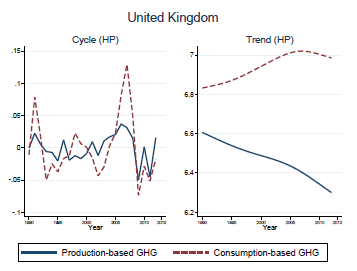

My working paper with Gail Cohen, Joao Jalles and Ricardo Marto shows how production-based emissions and consumption-based emissions differ in the UK. Both the cyclical components and the trend components are shown in the figure below.

Hendry reports per capita UK CO2 emissions, “which rose considerably till 1916, fluctuated violently till 1950, and have dropped dramatically since 1970” (see Hendry, 2017b).

“The sub-period distributions of UK CO2 emissions in [the figure below] illustrate their changes in shape, spread and location.”

My working paper with Gail Cohen, Joao Jalles and Ricardo Marto shows how production-based emissions and consumption-based emissions differ in the UK.

Posted by at 10:37 AM

Labels: Energy & Climate Change

Subscribe to: Posts