Monday, March 5, 2018

Economic Fluctuations in Sub-Saharan Africa

From a new IMF Working Paper:

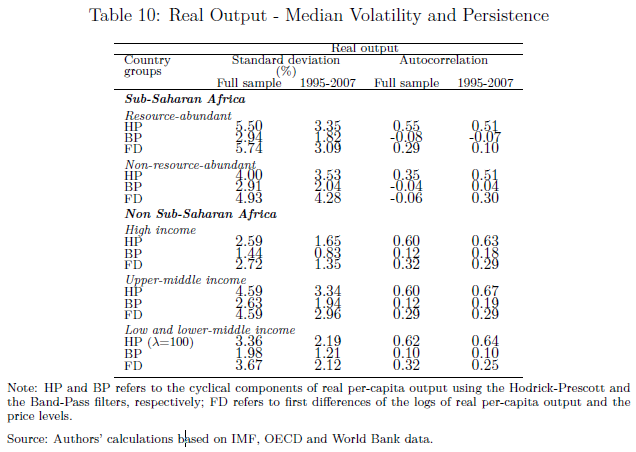

“We compare business cycle fluctuations in Sub-Saharan African (SSA) countries vis-à-vis the rest of the world. Our main results are as follows: (i) African economies stand out by their macroeconomic volatility, which is is reflected in the volatility of output and other macro variables; (ii) inflation and output tend to be negatively correlated; (iii) unlike advanced economies and emerging markets (EMs), trade balances and current accounts are acyclical in SSA; (iv) the volatility of consumption and investment relative to GDP is larger than in other countries; (v) the cyclicality of consumption and investment is smaller than in advanced economies and EMs; (vi) there is little comovement between consumption and investment; (vii) consumption and investment are strongly positively correlated with imports.”

Continue reading here.

From a new IMF Working Paper:

“We compare business cycle fluctuations in Sub-Saharan African (SSA) countries vis-à-vis the rest of the world. Our main results are as follows: (i) African economies stand out by their macroeconomic volatility, which is is reflected in the volatility of output and other macro variables; (ii) inflation and output tend to be negatively correlated; (iii) unlike advanced economies and emerging markets (EMs), trade balances and current accounts are acyclical in SSA;

Posted by at 5:30 PM

Labels: Inclusive Growth

House Prices in Namibia

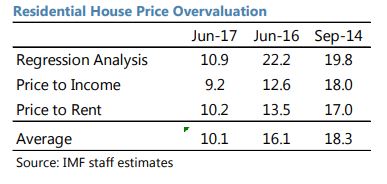

The IMF’s latest report on Namibia says that:

“Recently decelerating house prices and banks’ and households’ large exposure to mortgage loans raise concerns about risks from sudden corrections in the housing market. Staff estimate that, with the economy decelerating, house prices remain on average overvalued by about 10 percent, down from about 18 percent three years ago. FSAP sensitivity analysis suggests that all banks are resilient to a full correction in house price overvaluation. However, in the case of an over-correction (e.g., 20 percent price decline), some banks would be unable to comply with capital requirements. Under these scenarios, banks would deleverage with negative effects on credit and growth.”

The IMF’s latest report on Namibia says that:

“Recently decelerating house prices and banks’ and households’ large exposure to mortgage loans raise concerns about risks from sudden corrections in the housing market. Staff estimate that, with the economy decelerating, house prices remain on average overvalued by about 10 percent, down from about 18 percent three years ago. FSAP sensitivity analysis suggests that all banks are resilient to a full correction in house price overvaluation.

Posted by at 10:53 AM

Labels: Global Housing Watch

Saturday, March 3, 2018

Welfare Gains from Market Insurance: The Case of Mexican Oil Price Risk

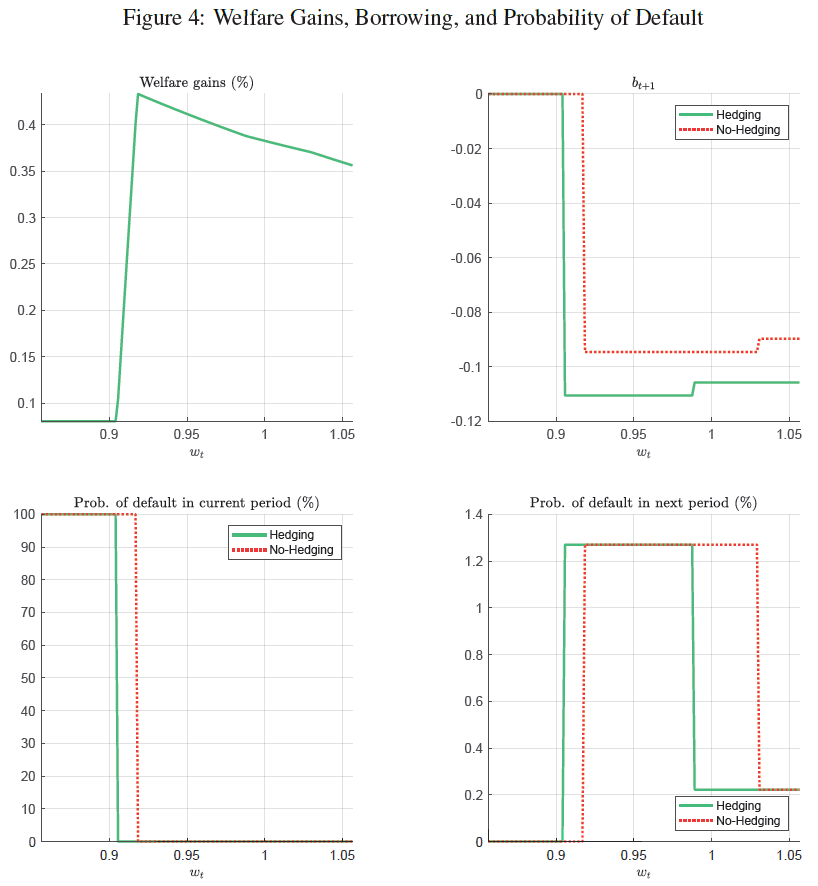

From a new IMF working paper:

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

From a new IMF working paper:

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

Posted by at 9:13 AM

Labels: Energy & Climate Change, Inclusive Growth

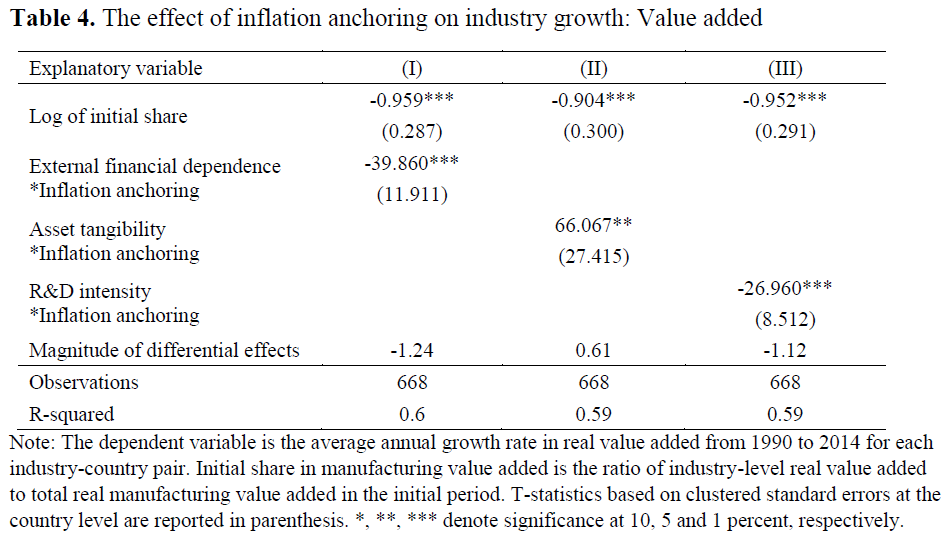

Inflation Anchoring and Growth: Evidence from Sectoral Data

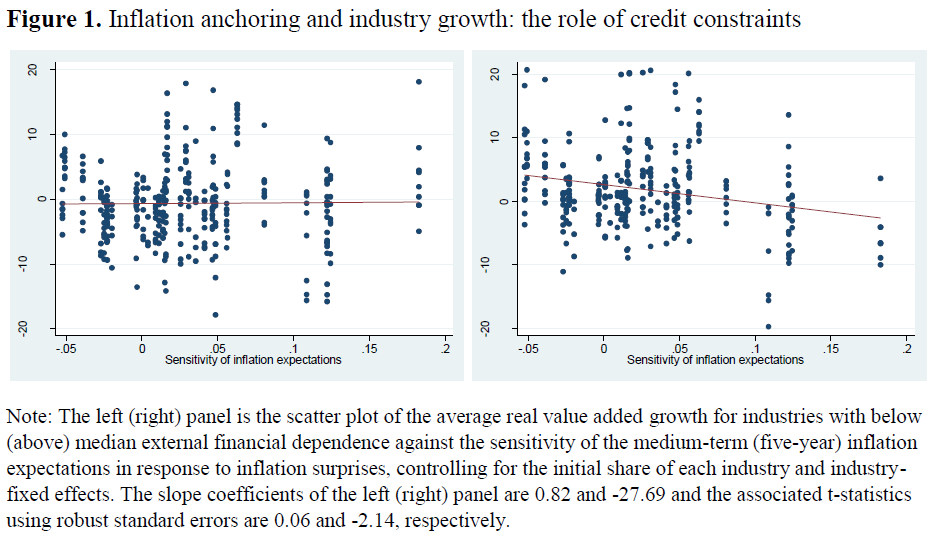

From my latest IMF working paper with Sangyup Choi and Davide Furceri:

“Central bankers often assert that low inflation and anchoring of inflation expectations are good for economic growth (Bernanke 2007, Plosser 2007). We test this claim using panel data on sectoral growth for 22 manufacturing industries for 36 advanced and emerging market economies over the period 1990-2014. Inflation anchoring in each country is measured as the response of inflation expectations to inflation surprises (Levin et al., 2004). We find that credit constrained industries—those characterized by high external financial dependence and R&D intensity and low asset tangibility—tend to grow faster in countries with well-anchored inflation expectations. The results are robust to controlling for the interaction between these characteristics and a broad set of macroeconomic variables over the sample period, such as financial development, inflation, the size of government, overall economic growth, monetary policy counter-cyclicality and the level of inflation. Importantly, the results suggest that it is inflation anchoring and not the level of inflation per se that has a significant effect on average industry growth. Finally, the results are robust to IV techniques, using as instruments indicators of monetary policy transparency and independence.”

From my latest IMF working paper with Sangyup Choi and Davide Furceri:

“Central bankers often assert that low inflation and anchoring of inflation expectations are good for economic growth (Bernanke 2007, Plosser 2007). We test this claim using panel data on sectoral growth for 22 manufacturing industries for 36 advanced and emerging market economies over the period 1990-2014. Inflation anchoring in each country is measured as the response of inflation expectations to inflation surprises (Levin et al.,

Posted by at 9:04 AM

Labels: Inclusive Growth

Friday, March 2, 2018

Housing View – March 2, 2018

On cross-country:

- Housing Europe Yearbook 2017 – Housing Europe

- Supply is the cause of the housing crisis – and we do need to build more homes in successful cities – Centre for Cities

- Real estate agent performance and fee structure – Vox

- The “V” in LTV and Why it Matters – European Covered Bond Council

- Strong house price rises continue in Europe, US, Canada and parts of Asia. The Middle East is weak. – Global Property Guide

On the US:

- California wants cities to build more housing near transit hubs. Can LA improve its track record on TOD? – Brookings

- America’s taxpayers shoulder too much housing risk – Economist

- Long-Term Outcomes of FHA First-Time Homebuyers – Federal Reserve Bank of New York

- Do State Income Taxes Affect Home Values? – Harvard Joint Center for Housing Studies

- The Number of High-Income Renters Surged, Especially in the Nation’s Highest-Cost Markets – Harvard Joint Center for Housing Studies

- What Would it Take for HUD to Meaningfully Increase Inclusion? – Harvard Joint Center for Housing Studies

- Foreign Investors Pile Into U.S. Student Housing – Wall Street Journal

- Airbnb CEO pledges to take more responsibility for impact to housing – Reuters

- Housing Bubble’s 10th Burst-Day – Real Estate Center at Texas A&M University

- How Do Mortgage Refinances Affect Debt, Default, and Spending? Evidence from HARP – Federal Reserve Bank of New York

On other countries:

- [Austria] Why Vienna remains a renter’s paradise – Financial Times

- [Canada] Toronto’s housing supply challenge and the growth plan paradox – Reuters

- [Chile] Squatters, Shanties, and Technocratic Professionals: Urban Migration and Housing Shortages in Twentieth-Century Chile – City University of New York

- [Malaysia] Affordable Housing: Challenges and the Way Forward – Central Bank of Malaysia

- [New Zealand] Residential construction and population growth in New Zealand: 1996-2016 – Reserve Bank of New Zealand

- [Spain] The Financial Transmission of Housing Bubbles: Evidence from Spain – Universitat Pompeu Fabra

- [Singapore] Singapore swing: pent-up demand boosts property prices – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Housing Europe Yearbook 2017 – Housing Europe

- Supply is the cause of the housing crisis – and we do need to build more homes in successful cities – Centre for Cities

- Real estate agent performance and fee structure – Vox

- The “V” in LTV and Why it Matters – European Covered Bond Council

- Strong house price rises continue in Europe,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts