Sunday, March 11, 2018

Economic Forecasts with the Yield Curve

From the Federal Reserve Bank of San Francisco:

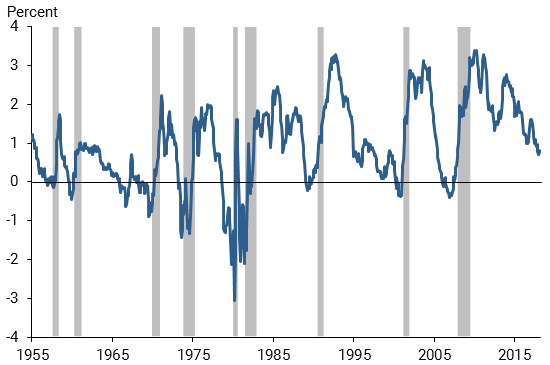

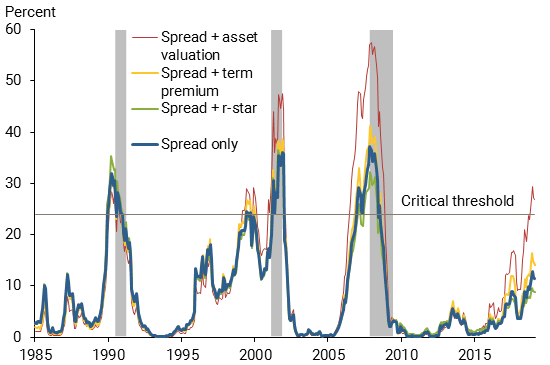

“Forecasting future economic developments is a tricky business, but the term spread has a strikingly accurate record for forecasting recessions. Periods with an inverted yield curve are reliably followed by economic slowdowns and almost always by a recession. While the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished. These findings indicate concerns about the scenario of an inverting yield curve. Any forecasts that include such a scenario as the most likely outcome carry the risk that an economic slowdown might follow soon thereafter.”

Figure 1

The term spread and recessions

Note: Gray bars indicate NBER recession dates.

Figure 2

Estimated probabilities of recession based on term spread

Note: Gray bars indicate NBER recession dates.

From the Federal Reserve Bank of San Francisco:

“Forecasting future economic developments is a tricky business, but the term spread has a strikingly accurate record for forecasting recessions. Periods with an inverted yield curve are reliably followed by economic slowdowns and almost always by a recession. While the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished.

Posted by at 9:46 AM

Labels: Macro Demystified

Saturday, March 10, 2018

Forecasts in Times of Crises

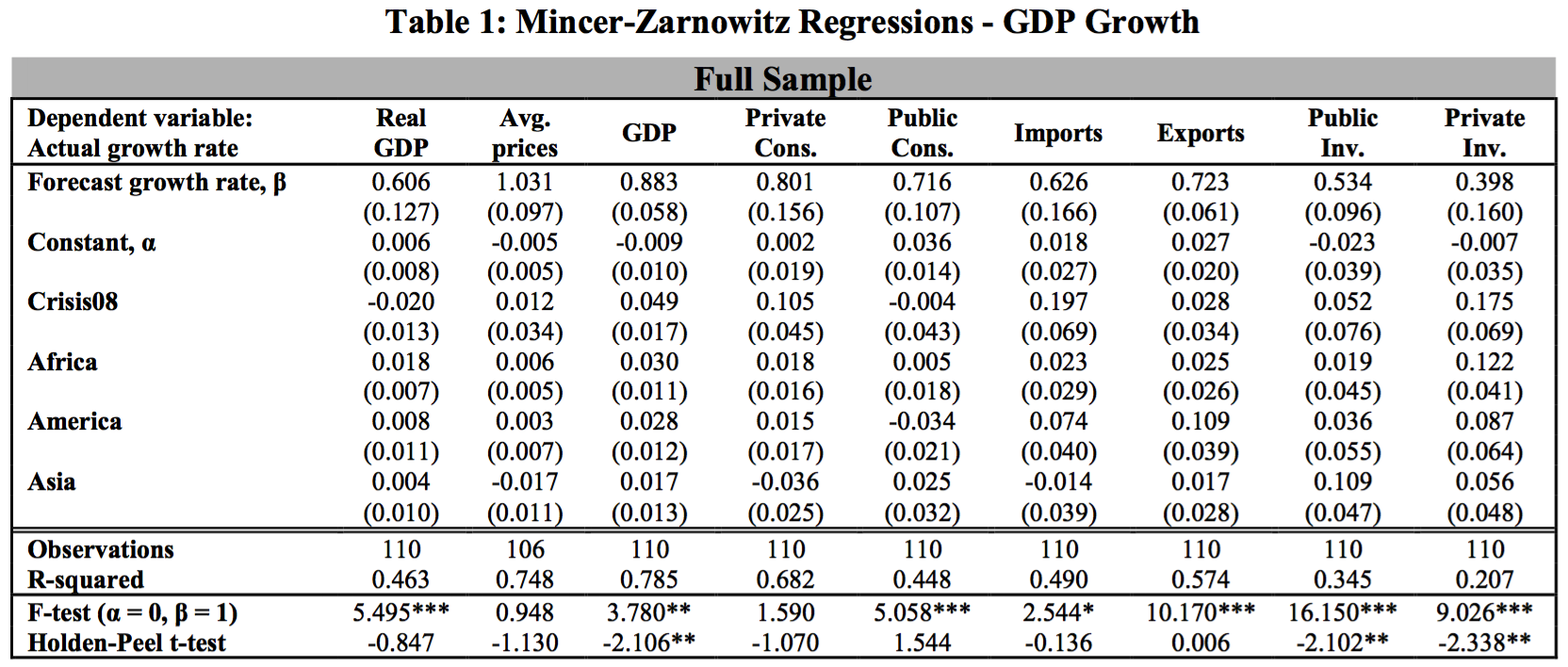

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However, we also document that there is room for improvement: two thirds of the key macroeconomic variables that we examine are forecast inefficiently and 6 variables (growth of nominal GDP, public investment, private investment, the current account, net transfers, and government expenditures) exhibit significant forecast bias. Forecasts for low-income countries are the main drivers of forecast bias and inefficiency, reflecting perhaps larger shocks and lower data quality. When we decompose the forecast errors into their sources, we find that forecast errors for private consumption growth are the key contributor to GDP growth forecast errors. Similarly, forecast errors for non-interest expenditure growth and tax revenue growth are crucial determinants of the forecast errors in the growth of fiscal budgets. Forecast errors for balance of payments growth are significantly influenced by forecast errors in goods import growth. The results highlight which macroeconomic aggregates require further attention in future forecast models for countries in crises.”

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However,

Posted by at 10:57 PM

Labels: Forecasting Forum

Thursday, March 8, 2018

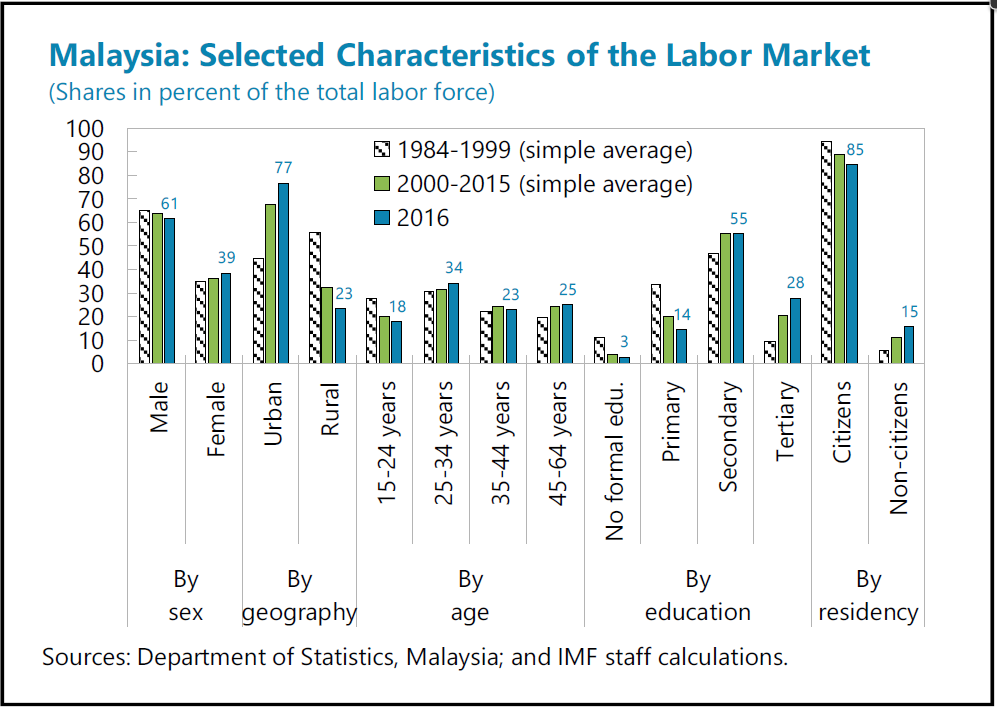

Significant Shifts in Malaysian Labor Market

The latest IMF report on Malaysia says the “Malaysia’s economy and its labor market have undergone significant shifts in the last three decades. The labor market is now more urban and has a higher share of female workers and workers with tertiary education. Employment has kept pace with labor supply, keeping the unemployment rate stable for more than a decade. Meanwhile, reliance on non–citizen workers has also increased against the backdrop of slower growth in citizen population. Continuing with its economic transformation, Malaysia aspires to achieve high–income status, with a labor market that is ready for the economy of the future: a market that can support more female workers, more skilled jobs, and a higher labor productivity growth.”

The latest IMF report on Malaysia says the “Malaysia’s economy and its labor market have undergone significant shifts in the last three decades. The labor market is now more urban and has a higher share of female workers and workers with tertiary education. Employment has kept pace with labor supply, keeping the unemployment rate stable for more than a decade. Meanwhile, reliance on non–citizen workers has also increased against the backdrop of slower growth in citizen population.

Posted by at 5:15 PM

Labels: Inclusive Growth

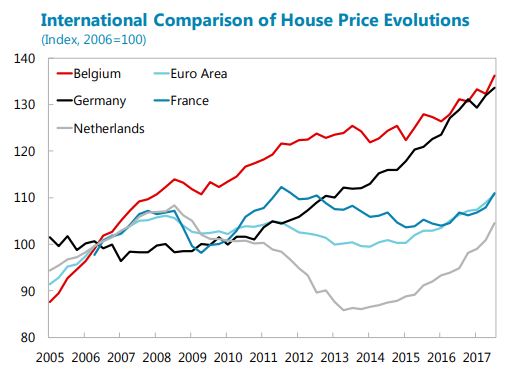

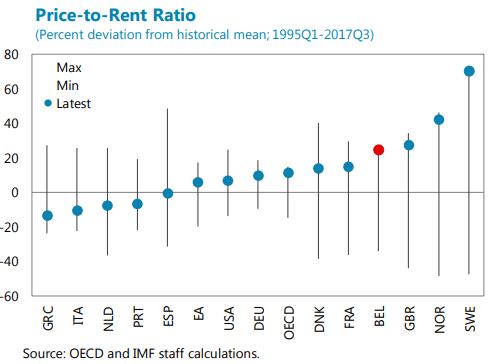

Housing Market in Belgium

The latest IMF report on Belgium says that:

“The housing market appears to be only moderately overvalued, but pockets of vulnerability exist. Having grown rapidly in the 2000s, residential housing prices did not experience a sharp decline during the crisis, and have since risen by about 20 percent in nominal terms. The price-to-rent and price-to-income ratios stand well above their historical averages. More sophisticated measures, however, indicate only a moderate overvaluation. Since 2015 there has been a reversal in the tightening of mortgage lending standards, as evidenced by a growing share of loans with high loan-to-value (LTV) and/or high debt service-to-income (DSI) ratios. Risks are mitigated to some extent by the fact that Belgian households generally hold considerable financial assets. Nevertheless, nearly a third of outstanding mortgage debt is held by households whose liquid financial assets cover less than six months of debt service.

It will be important to stand ready to tighten macroprudential conditions further if balance sheet risks were to grow significantly. To address growing risks in the housing market, the NBB in 2014 introduced a 5 percent risk weight add-on for banks using internal ratings models to determine their minimum regulatory capital requirements for mortgage loans. In 2017, the NBB proposed a tightening of macroprudential policies through a targeted increase in capital charges linked to the riskiness of exposures, proxied by LTV ratios. However, as this proposal was not accepted by the government, the NBB subsequently proposed a new macroprudential measure requiring banks with riskier mortgage portfolios to hold more capital. This measure should be enacted promptly. Looking ahead, it will be important to strengthen the NBB’s ability to deploy cyclical macroprudential measures in the financial sector in a timely manner.”

The latest IMF report on Belgium says that:

“The housing market appears to be only moderately overvalued, but pockets of vulnerability exist. Having grown rapidly in the 2000s, residential housing prices did not experience a sharp decline during the crisis, and have since risen by about 20 percent in nominal terms. The price-to-rent and price-to-income ratios stand well above their historical averages. More sophisticated measures, however, indicate only a moderate overvaluation.

Posted by at 4:26 PM

Labels: Global Housing Watch

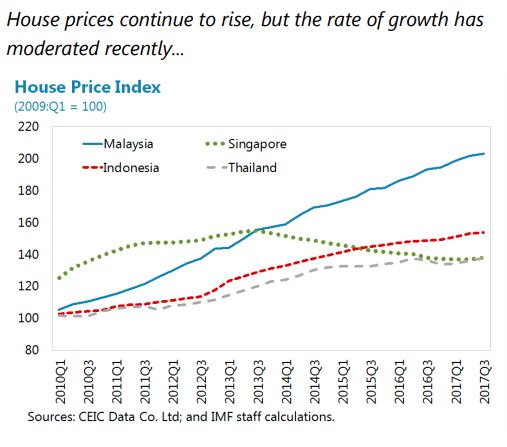

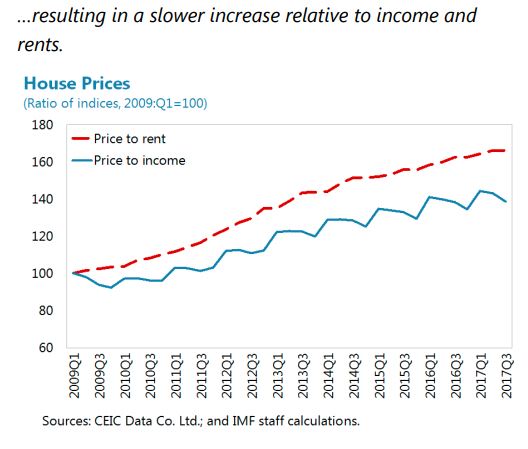

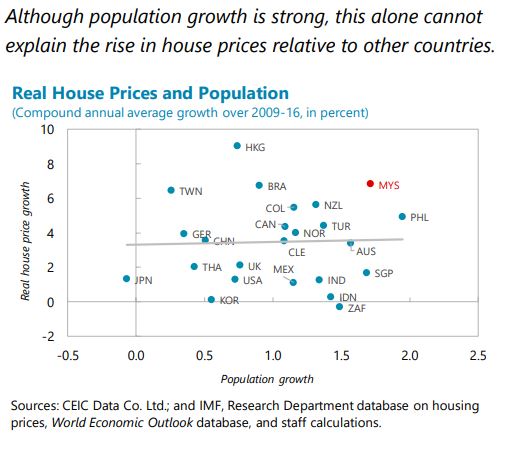

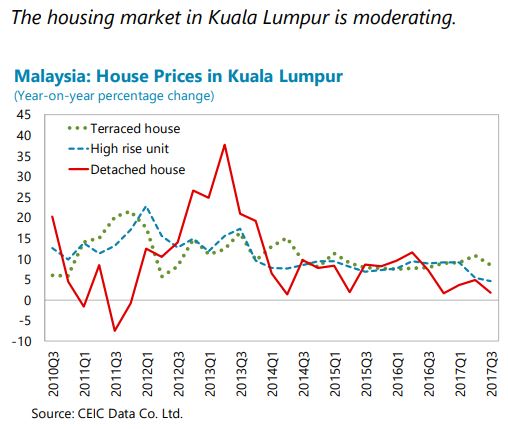

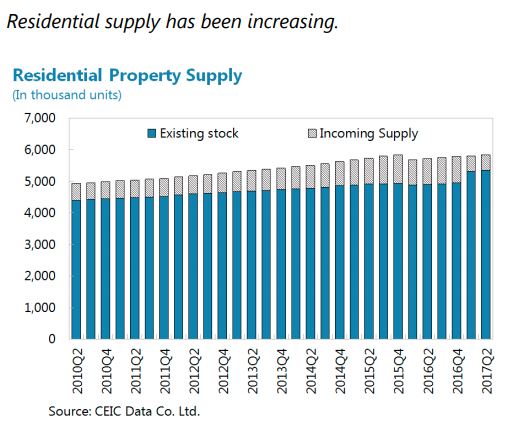

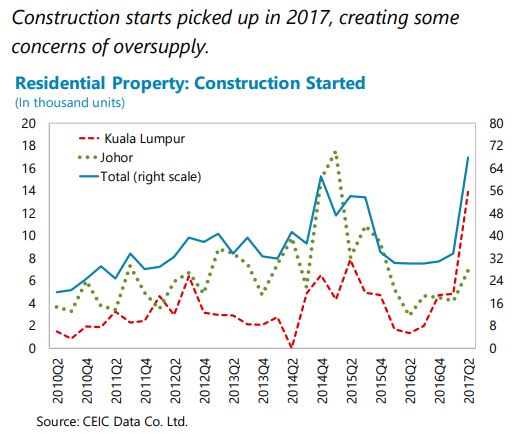

Housing Market in Malaysia

The IMF’s latest report on Malaysia says that:

“Measures could be considered to mitigate risks to financial stability. For the housing (…) market, possible measures could include risk weights and lending limits targeting the construction sector, and measures encouraging developers to lease the housing stock that remains unsold for an extended period. To encourage the rental market, the authorities could look into reforming the regulations pertaining to rents and tenant-landlord relationships or granting developers tax exemptions for rental income on leasing units, within the context of the approved government budget envelope. On mortgage lending, sector-wide LTVs (on the second and first properties) and debt service to income limits could supplement the ones that are presently selfimposed by the banks, complementing the existing limit for borrowers with income under 3,000 ringgits per month. Strong economic conditions offer a good window of opportunity for the above policy adjustments.”

The IMF’s latest report on Malaysia says that:

“Measures could be considered to mitigate risks to financial stability. For the housing (…) market, possible measures could include risk weights and lending limits targeting the construction sector, and measures encouraging developers to lease the housing stock that remains unsold for an extended period. To encourage the rental market, the authorities could look into reforming the regulations pertaining to rents and tenant-landlord relationships or granting developers tax exemptions for rental income on leasing units,

Posted by at 4:20 PM

Labels: Global Housing Watch

Subscribe to: Posts