Friday, September 7, 2018

Understanding the Decline of U.S. Manufacturing Employment

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong, and that, as in agriculture, productivity growth, assumed to reflect automation, is largely responsible for the relative and absolute decline in manufacturing employment. Although the size and scope of the decline in employment manufacturing industries in the 2000s was unprecedented, many

see it as part of a long-term trend and deem the role of trade small.”

“That view, I have argued, reflects a misinterpretation of the numbers. First, aggregate manufacturing output and productivity statistics are dominated by the computer industry and mask considerable weakness in most manufacturing industries, where real output growth has been much slower than average private sector growth since the 1980s and has been anemic or declining since 2000. Second, labor productivity growth is not synonymous with, and is often a poor indicator of, automation. Measures of labor productivity growth may capture many forces besides automation—including improvements in product quality, outsourcing and offshoring, and a changing industry composition owing to international competition. Indeed, the rapid productivity growth in the computer and electronics products industry, and by extension in the manufacturing sector, largely reflects improvements in product quality, not automation. In short, the stylized facts, when properly interpreted, do not provide prima facie evidence that automation drove the relative and absolute decline in manufacturing employment.”

“It is difficult to parse out the effects of various factors on manufacturing employment, and research does not provide simple decompositions of the total contribution that trade and the broader forces of globalization make to manufacturing’s recent employment decline. Nevertheless, the research evidence points to trade and globalization as the major factor behind the large and swift decline of manufacturing employment in the 2000s. Although manufacturing processes continue to be automated, there is no evidence that the pace of automation in the sector accelerated in the 2000s; if anything, research comes to the opposite conclusion.”

“Manufacturing still matters, and its decline has serious economic consequences. Reflecting the sector’s deep supply chains, manufacturing’s plight contributed to the weak employment growth and poor labor market outcomes prevailing during much of the 2000s. Research shows that such large-scale shocks have persistent adverse effects on affected communities and their residents, though these costs rarely are fully considered in policy making (Klein, Schuh, and Triest 2003). In addition, because manufacturing accounts for a disproportionate share of R&D, the health of manufacturing industries has important implications for innovation in the economy. The widespread denial of domestic manufacturing’s weakness and globalization’s role in its employment collapse has inhibited much-needed, informed debate over trade policies.”

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong,

Posted by at 10:56 AM

Labels: Inclusive Growth, Macro Demystified

Housing View – September 7, 2018

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs. Wealth in Household Debt Obligations: Evidence from Housing Policy in the Great Recession – NBER

- Lessons from the financial crisis: The central importance of a sustainable, affordable and inclusive housing market – Brookings

- Three ways to strengthen the affordable rental housing supply – Urban Institute

On other countries:

- [Australia] Australia’s property boom ends as credit squeeze begins – Financial Times

- [Brazil] Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- [China] China struggles to heed Xi’s call to develop rental housing – Financial Times

- [China] Housing Affordability in Urban China: A Comprehensive Overview – SSRN

- [Hong Kong] Hong Kong’s hot property sector show signs of cooling – Financial Times

- [Hong Kong] Hong Kong’s Runaway Property Market May Be Heading for a Fall – Bloomberg

- [Netherlands] Netherlands’ housing market remains strong – Global Property Guide

- [United Kingdom] History Dependence in the Housing Market – Centre for Economic Performance

- [United Kingdom] London housing: the bearish Brexit take – Financial Times

- [United Kingdom] Can house prices teach us anything about schools? – BBC

Photo by Aliis Sinisalu

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs.

Posted by at 10:26 AM

Labels: Global Housing Watch

Thursday, September 6, 2018

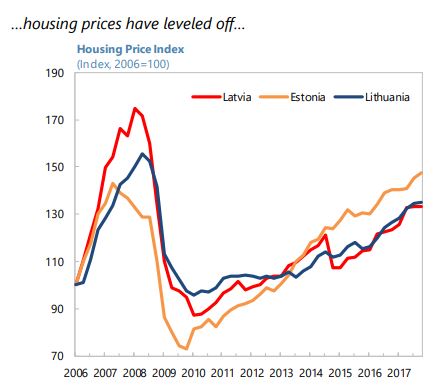

Housing Market in Latvia

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

Posted by at 10:34 AM

Labels: Global Housing Watch

Tuesday, September 4, 2018

RIP Herman Stekler, A Forecasting Giant

Herman Stekler, a giant in the field of forecasting, has passed away. He was known for insisting that “the cost of a recession is so great that a forecaster should never miss one. Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman shuttled between academia and policy institutions throughout his career. His interest was in business and applied economics; in fact, during his graduate school years at MIT he complained to Paul Samuelson about his “frustration and concern that economics was too abstract. There were not enough applications to the real world.” This interest in practical applications led him to spend a summer during his graduate school years at the Rand Corporation helping to devise an early warning radar system to alert the US and Canada in the event of an attack from the USSR. This experience nurtured some of Herman’s interest in leading indicators for economic activity, and it also led to a lasting interest in the defense industry.

For his starting job after graduate school, however, he chose academia over business because he “did not like some of the culture of the business community: During my visit to IBM, I was struck by the fact that every professional had to have his shoes polished before lunch.” He started instead at the University of California, Berkeley, in the business school, in 1959.

In July 1966, he moved to the Fed, starting work in the National Income Section of the Research and Statistics Division. Economic forecasts had just started to be included in the Fed’s so-called ‘Greenbook’ in the fourth quarter of 1965. Herman’s task at the Fed was to help prepare the Greenbook forecasts and sometimes to write an explanation for the rationale behind the forecasts. While the experience was exhilarating, Herman eventually left the Fed as the process of preparing the forecasts – at that time FOMC meetings were held every three weeks – left little time for research (including research on the assessment of the Fed’s forecasts, which Herman spent a lot of time on in the years that followed).

In 1968, Herman joined the faculty at the State University of New York–Stony Brook as a full professor. Reflecting his interest in the defense industry, he later moved to the Industrial College of the Armed Forces (ICAF), where he taught until the early 1990s. As he was planning to retire in 1994, George Washington University tempted him with a research professor position for a year. For every year since then, Herman incorrectly forecast the date of his retirement, which he always said would be “next year.” Nearly, twenty five years later, Herman was still at George Washington, writing papers and advising students to the very end of his days.

Herman published widely in nearly every branch of forecasting, including sports forecasting. A colleague of his once said that Herman “is willing to forecast anything that moves and everything that stands still.”

Herman, my dear friend, it is sad to see you stand still.

**

The Stekler Award for Courage in Forecasting

Herman’s views and his relentless push to get forecasters to predict “early and clearly” led me to institute a Stekler Award for Courage in Forecasting. The recipients of the award thus far are given below:

Groundhog Day Tradition: 2017 Stekler Award for Courage in Forecasting

A Groundhog Day Tradition: The Stekler Award for Courage in Forecasting

The Stekler Award for Courage in Forecasting (Recessions Inaccurately)

Special section in International Journal of Forecasting honoring Herman

In 2012, Herman’s colleagues and friends organized a workshop (Honoring a Forecasting Giant) on the occasion of his 80th birthday, the proceedings of which were published in a special section (On Groundhog Day, Honoring A Forecasting Giant) in the International Journal of Forecasting. The preface to that section describes Herman’s professional work, from which I quote below.

In a famous paper in the American Economic Review (Stekler, 1972), Herman tried to understand why forecasters fail to predict recessions. The evidence that forecasters prefer to miss turning points that occur rather than to predict recessions that do not occur led him to suggest asymmetric loss functions as one possible explanation. (For the record, in October 2007 Herman correctly predicted the onset of the Great Recession and also predicted that the ensuing recovery would be quite weak).

Herman had an abiding interest in improving the ability of economic forecasters to predict turning points. This was the theme of his Ph.D. thesis at MIT. Building on work by his advisor Sidney Alexander, Herman tried to develop a procedure that could be used to forecast turning points in real time. His idea was to predict a turning point if a composite indicator of economic activity was below (above) its previous peak (trough) for a certain number of months. Obviously, a longer lead was more desirable but it also increased the odds of calling a false turning point; Herman’s thesis analyzed the tradeoff between the length of the forecasting lead and the frequency of false signals (Alexander & Stekler, 1959).

In subsequent work, Herman found that forecasters’ record of predicting turning points left a lot to be desired. This was true regardless of the method of forecasting—whether through leading indicators, econometric models or judgmental methods. In the 1960s, he did a consulting project where his ‘”task was to evaluate every econometric model then in existence and determine whether any of them provided accurate forecasts [of turning points]. They did not” (this quote and others in this overview are from an interview with Herman—see Joutz, 2010).

Herman Stekler, a giant in the field of forecasting, has passed away. He was known for insisting that “the cost of a recession is so great that a forecaster should never miss one. Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman shuttled between academia and policy institutions throughout his career.

Posted by at 2:30 PM

Labels: Forecasting Forum

Monday, September 3, 2018

The Measurement and Macro-Relevance of Corruption

From a new IMF working paper:

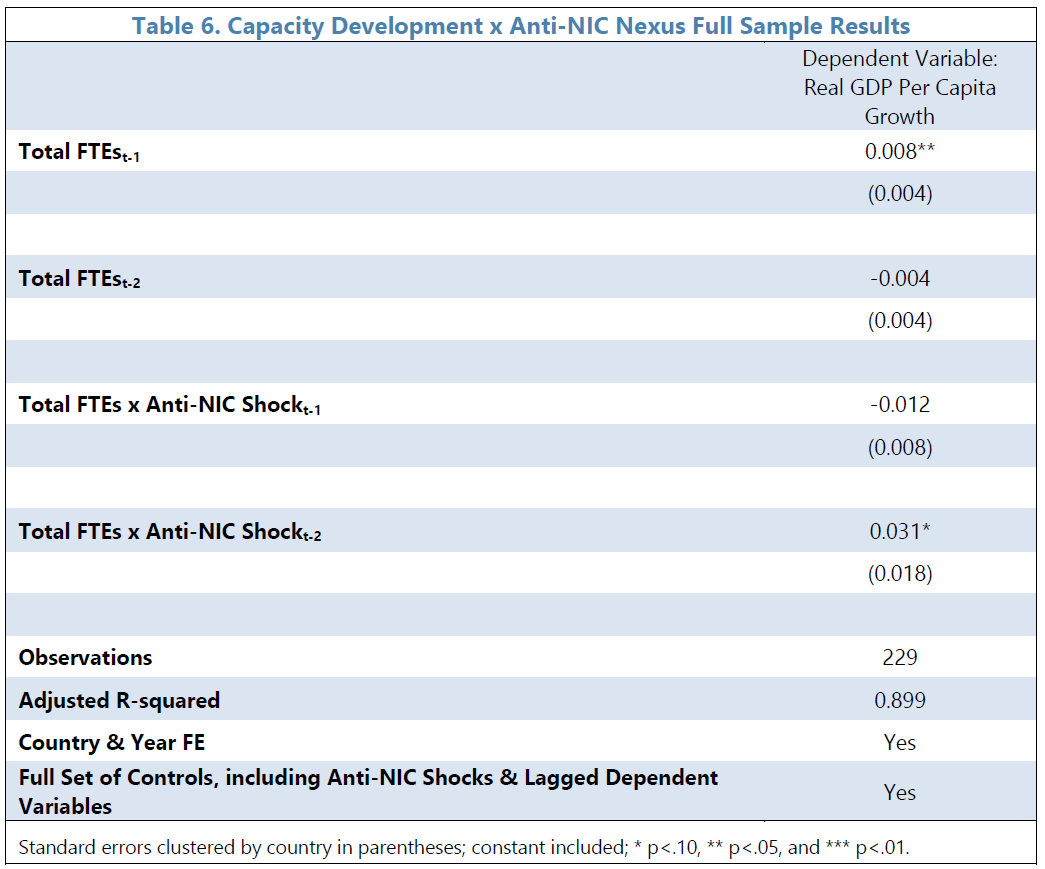

“Corruption is macro-relevant for many countries, but is often hidden, making measurement of it—and its effects—inherently difficult. Existing indicators suffer from several weaknesses, including a lack of time variation due to the sticky nature of perception-based measures, reliance on a limited pool of experts, and an inability to distinguish between corruption and institutional capacity gaps. This paper attempts to address these limitations by leveraging news media coverage of corruption. We contribute to the literature by constructing the first big data, cross-country news flow indices of corruption (NIC) and anti-corruption (anti-NIC) by running country-specific search algorithms over more than 665 million international news articles. These indices correlate well with existing measures of corruption but offer additional richness in their time-series variation. Drawing on theory from the corporate finance and behavioral economics literature, we also test to what extent news about corruption and anti-corruption efforts affects economic agents’ assessments of corruption and, in turn, economic outcomes. We find that NIC shocks appear to negatively impact both financial (e.g., stock market returns and yield spreads) and real variables (e.g., growth), albeit with some country heterogeneity. On average, NIC shocks lower real per capita GDP growth by 3 percentage points over a two-year period, illustrating persistence in the effect of such shocks. Conversely, there is suggestive evidence that anti-NIC efforts appear to have a sustained positive macro impact only when paired with meaningful institutional strengthening, proxied by capacity development efforts.”

From a new IMF working paper:

“Corruption is macro-relevant for many countries, but is often hidden, making measurement of it—and its effects—inherently difficult. Existing indicators suffer from several weaknesses, including a lack of time variation due to the sticky nature of perception-based measures, reliance on a limited pool of experts, and an inability to distinguish between corruption and institutional capacity gaps. This paper attempts to address these limitations by leveraging news media coverage of corruption.

Posted by at 8:05 PM

Labels: Inclusive Growth

Subscribe to: Posts