Monday, September 17, 2018

Urban Revitalization: The View from the Trenches

Global Housing Watch Newsletter: September 2018

Why social responsibility matters for urban revitalization? How does a developer provide city center affordable housing? How can a developer involve the community in a urban revitalization process? What challenges do developers face? These are some of the questions that Keyes Christopher “KC” Hardin tackles in this interview. KC is the co-founder and CEO of Conservatorio SA—a real estate development company based in Panama City, Panama. He is also a Fellow of the Aspen Institute’s Central American Leadership Initiative, and a Research Associate at MITs Community Innovators Laboratory.

The company…

Hites Ahir: What is Conservatorio SA and what does it do?

KC Hardin: Conservatorio SA is a real estate development company dedicated to sustainable urban revitalization. We started Conservatorio SA fourteen years ago to fix up a couple of historic buildings in Panama City’s UNESCO Heritage site, and it’s grown into a company that builds just about every category of product you can find in a downtown—hotels, condos, offices, multi-family, even cultural infrastructure like theatres.

We call our brand of real estate “sustainable urban revitalization” which is basically mixed-use, mixed-income urban core redevelopment with a heavy social inclusion component. Within all those categories we also build just about every level. We have hotels that are $17 US dollars per night and hotels that are over $300 US dollars. We build apartments that sell for $80,000 US dollars and others for $2 million US dollars. All within a few blocks of each other. We tend to hold on to commercial property for the long-term but we like to sell apartments because it allows us to recycle capital and we think that neighborhoods work better when people have a chance to own their own homes.

Hites Ahir: Why social responsibility matters to Conservatorio SA?

KC Hardin: On a personal level, I grew up in Miami until the 1990s and then in New York until 2003. For whatever reason I was always in neighborhoods that were either revitalizing or deteriorating. So, I had a sense for the good and the bad of an urban revitalization cycle. I saw how much better cities worked when their cores became vibrant and safe, but I also came to understand that there was a question of “better for whom?” So Conservatorio SA was founded on the question of whether it is possible to have the good of urban revitalization while minimizing its two big negative externalities: displacement and cultural homogenization.

That question has taken us down a long road of learning how to balance our responsibility to capital with our responsibility to community. Along the way we’ve picked up what I think is a pretty deep understanding of the mechanisms of social and economic exclusion, the long-term value of authenticity and how to co-create with communities.

The historic district of Panama City…

Hites Ahir: How has Casco Viejo and the surrounding area evolved over the years?

KC Hardin: The Spanish laid out Casco Viejo’s fantastic street grid in the 1500s, and it has been transforming ever since, through numerous booms and busts. As Panama most recently boomed in the 2000s, Casco Viejo lagged the rest of the city. I think this is because very few investors understood how revitalization works back then. When we started Conservatorio SA in 2004 more than 80 percent of the building inventory was unrestored, there were four gangs that controlled the district, and raw sewage leaked onto the streets, just to name a few issues. But there were preservationists who fought hard to protect the area, and pioneers who started reigniting it culturally. It is now able to support a very high quality of life, and is a point of pride for the country.

Hites Ahir: What has happened to house prices?

KC Hardin: Housing prices have risen from being about 30 percent lower than the best parts of the city in 2007 to being about 30 percent higher now. I think that premium is due to limited supply, higher construction costs, and a unique lifestyle that doesn’t exist in other parts of the city. On the rental side, the change has been even more dramatic because it has gone from a neighborhood where most people lived in condemned buildings paying little or no rent to one of the city’s most expensive. So, in terms of relevance to the city and pricing, the neighborhood has gone full cycle from its last peak in the 1950s.

But that revitalization has come at a human cost because much of the population that moved in during the decline was not given a real opportunity to stay. There was a direct tension between public policies designed to restore heritage and create economic growth on one side, and the social need of preventing widespread displacement on the other. There were well-intentioned but isolated efforts to balance these tensions but going forward we need better public policy and a deeper understanding of the long-term value of authenticity in the private sector.

Hites Ahir: How do you go about providing affordable housing in the area?

KC Hardin: Conservatorio SA has an internal policy of building one affordable housing unit for every high-end unit. We keep them affordable by keeping them compact, making parking optional, and sharing social areas and other amenities among several adjacent buildings. In many buildings, we mix market rate with affordable, so there are often a few units where the price is subsidized by those market rate units. There is also a government subsidy on interest rates for apartments that are under $120,000 US dollars, which helps keep the monthly payment affordable. For example, the monthly payment on a two bedroom can be as low as $380 US dollars, meaning that it is affordable for a minimum wage couple. That still leaves out a lot of people in our community so we need the government to address this gap.

Building an inclusive neighborhood…

Hites Ahir: What are some of the social projects that you have implemented to help, and involve the community?

KC Hardin: Besides building affordable housing, our primary social mission is to nurture an eco-system of social and economic inclusion programs. We believe that homeownership is a critical determinate of social outcomes, but we have learned that in historically marginalized communities the opportunity to buy, or even to move into a formal rental, no matter how affordable, is a very high rung on the ladder for many people. So investment in human development is the other key to minimizing displacement.

We invest in programs that address a multitude of interrelated problems like violence, teenage pregnancy, education, and poverty. We have also learned that all of those problems are just symptoms of a dysfunctional system. To create any sustainable change, those programs have to be tied together with a larger process of community organization, and empowerment that will hopefully push the community back into balance over the long-term. To help that process, we worked with the Community Innovators Lab at MIT to create a leadership development program called LiderazCo, which is short for “Leaders who Co-Create Community”.

Hites Ahir: If you had to pick one social project that has had the most significant impact in the district, which one would it be?

KC Hardin: Resolving gang tensions was critical. We invested heavily in a program to integrate gang members into the broader community. The outcomes at the individual level varied widely, but I think it had the effect of not only reducing violence, but also changing perceptions in the public and private sector about what was possible. In Latin America there is a strong bias towards repressive policies towards gangs that is probably counter-productive in the long run, so one of the program’s goals was to build bridges between sectors that don’t normally connect.

Hites Ahir: In your drive to build inclusive city center housing, what are the top three challenges that you are facing?

KC Hardin: I see three big challenges for inclusive housing. First is antiquated zoning that requires expensive parking and generally encourages lower priced detached housing out on the periphery of the city. The rules are conceived around an ideal of city center apartments for middle-to-upper income nuclear families who have two cars and two incomes. That leaves out a lot of people and makes it hard to innovate with new housing models, though lately the city has been receptive to proposals.

The second problem is a strict bank financing criteria that generally filters out people who are self-employed and those who are in the informal economy.

The final challenge is the high degree of marginalization in our society. The lack of investment in human development has made it extremely difficult for a lot of people to break into the formal economy, especially here where the big job growth is in the service sector.

What is next?

Hites Ahir: What is next for Consevatorio SA?

KC Hardin: In terms of lines of business, we are rapidly pushing further into bottom-of-the-pyramid, urban core housing solutions. We feel that affordable, multi-family housing with imbedded social services can be a profitable, and a key step in the ladder to equity. We are also working with our academic partners on some interesting commercial models around formalizing informal commerce. Geographically, we are now in Honduras and want to create urban core-focused joint ventures with like-minded developers throughout Latin America.

Global Housing Watch Newsletter: September 2018

Why social responsibility matters for urban revitalization? How does a developer provide city center affordable housing? How can a developer involve the community in a urban revitalization process? What challenges do developers face? These are some of the questions that Keyes Christopher “KC” Hardin tackles in this interview. KC is the co-founder and CEO of Conservatorio SA—a real estate development company based in Panama City,

Posted by at 5:00 AM

Labels: Global Housing Watch

Sunday, September 16, 2018

RIP Deena Khatkhate, far-sighted IMF and RBI economist

Deena Khatkhate, who raised the quality of economic discourse through his work at the Reserve Bank of India and the IMF and his editorship of World Development, has passed away. A review of one of his books by Charles Collyns and myself gives a flavor of Deena’s intellectual contributions and independence of mind.

**

“Life is lived forwards but understood backwards,” wrote the philosopher Kierkegaard. This collection of a life-time’s work of the Indian economist Deena Khatkhate can be understood as an act of rebellion against much of his intellectual inheritance: socialism and central planning, Keynesian macroeconomics, and an adversarial view of North-South relationships. Instead, these essays put forward a spirited (but not uncritical) defense of capitalism and markets, espouse a macroeconomics as much Friedmanite as Keynesian, and urge a constructive approach to relationships between developing and advanced nations.

The last of these themes is illustrated in arguably the best article in the collection, which is on the brain drain—the emigration of skilled workers from developing to advanced countries. In this article, published in F&D in 1971, Khatkhate challenged the prevalent view of the brain drain as an evil, a form of aid from the poor to the rich. He showed that because most emigration occurred from developing countries with a clear excess supply of skilled workers, it was actually a social safety valve for the poor countries. And because it encouraged the “cross fertilization of ideas” between skilled workers from the poor nations and the richer nations, the brain drain could be “a desirable investment.”

There are examples of this prediction coming to pass, such as the success of software exports from countries like India, Ireland, and Israel to more advanced nations. Ashish Arora, a professor at Carnegie Mellon University, has shown that this success is due in part to “the reserve army of underemployed engineers and scientists in these countries [that] had previously migrated to the United States and the United Kingdom.” Through their work abroad, this diaspora gained experience with the business practices of their future customers—an earlier brain drain had turned into a brain gain, as Khatkhate predicted.

Other essays on North-South relationships in the book include one on “conflict and cooperation in the inter- national monetary system.” Written in 1987, it anticipates many reforms of the IMF and other international agencies—such as giving “greater voice” to the South in decision making—that have taken place or have come to the front of the agenda. To be sure, Khatkhate was one of many making similar suggestions. But, as he notes in the preface, he “received some flak” for this article since he was employed at the IMF at the time. In any event, Khatkhate soon left the IMF, after two decades of service, and went on to become editor of World Development, a scholarly journal.

Prior to joining the IMF, Khatkhate worked for over a decade—from 1955 to 1968—at the Reserve Bank of India, the country’s central bank. Not surprisingly, therefore, a second major theme of the essays is the role of macroeconomic and financial policies in promoting economic growth. In the 1950s, the Keynesian view advocated running fiscal deficits to promote growth in developing countries. The rationale was that since there were underemployed resources in these economies, heavy government spending could lead to employment of those resources without triggering inflation. However, Khatkhate writes that the negative evidence on the actual impact of government spending convinced him that “all that happened as a result of heavy resort to fiscal deficit was inflation, decline in income, saving and investment.” Khatkhate’s views on monetary policy also differed from the 1960s Keynesian view, emphasizing as they did the need for rules to guide the central bank rather than give it too much discretion.

A third theme is the rhetoric vs. the reality of socialism and central planning. Khatkhate blamed socialism for trying to deliver both growth and equity and delivering neither. The real problem in developing countries, he said, was not so much the skewed income distribution but “improving the standard of the whole mass of people, which is possible only with rapid economic growth.” These views were far from the mainstream when Khatkhate wrote them in 1978. He is not, however, an unvarying defender of capitalism and free markets. On the free mobility of capital, for instance, his views are close to that of his compatriot Jagdish Bhagwati in favoring a cautious approach, given the evidence that hasty liberalization can contribute to financial crises.

Deena Khatkhate, who raised the quality of economic discourse through his work at the Reserve Bank of India and the IMF and his editorship of World Development, has passed away. A review of one of his books by Charles Collyns and myself gives a flavor of Deena’s intellectual contributions and independence of mind.

**

“Life is lived forwards but understood backwards,” wrote the philosopher Kierkegaard. This collection of a life-time’s work of the Indian economist Deena Khatkhate can be understood as an act of rebellion against much of his intellectual inheritance: socialism and central planning,

Posted by at 10:57 AM

Labels: Profiles of Economists

Friday, September 14, 2018

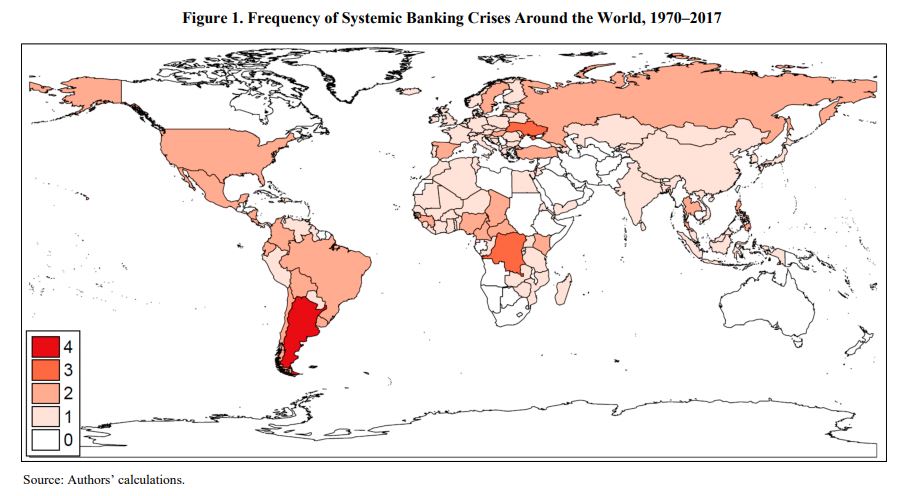

Systemic Banking Crises Revisited

From a new IMF working paper by Luc Laeven and Fabian Valencia:

“This paper updates the database on systemic banking crises presented in Laeven and Valencia (2008, 2013). Drawing on 151 systemic banking crises episodes around the globe during 1970-2017, the database includes information on crisis dates, policy responses to resolve banking crises, and the fiscal and output costs of crises. We provide new evidence that crises in high-income countries tend to last longer and be associated with higher output losses, lower fiscal costs, and more extensive use of bank guarantees and expansionary macro policies than crises in low- and middle-income countries. We complement the banking crises dates with sovereign debt and currency crises dates to find that sovereign debt and currency crises tend to coincide or follow banking crises.”

From a new IMF working paper by Luc Laeven and Fabian Valencia:

“This paper updates the database on systemic banking crises presented in Laeven and Valencia (2008, 2013). Drawing on 151 systemic banking crises episodes around the globe during 1970-2017, the database includes information on crisis dates, policy responses to resolve banking crises, and the fiscal and output costs of crises. We provide new evidence that crises in high-income countries tend to last longer and be associated with higher output losses,

Posted by at 4:26 PM

Labels: Macro Demystified

Housing View – September 14, 2018

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- These May Be the World’s 10 Riskiest Housing Markets – Bloomberg

On the US:

- Ben Carson and HUD Get Ready to Take On the Nimbys – Bloomberg

- Mapping the boom in nonbank mortgage lending—and understanding the risks – Brookings

- Is the housing price-rent ratio a leading indicator? – Federal Reserve Bank of St. Louis

- Americans are now better off renting than buying. Above all, avoid buying in Dallas! – Global Property Guide

- Rental Glut Sends Chill Through the Hottest U.S. Housing Markets – Bloomberg

- Mortgage Fraud Fueled the Financial Crisis—and Could Again – Institute of New Economic Thinking

- Voters Can Keep Housing Affordable – New York Times

- Book Review: High-Risers: Cabrini-Green and the Fate of American Public Housing – The New York Review of Books

- The Financial Crisis Changed Home Buying Forever – Wall Street Journal

- Preserving Affordable Rental Housing – MacArthur Foundation

- The Housing Bubble Burst All Over Reality TV – New York Times

- Maryland’s Biggest County Responds to Full Schools by Halting New Housing – Slate

- City NIMBYS – Furman Center for Real Estate and Urban Policy

On other countries:

- [Australia] Chinese real estate investment in Australia drops by nearly 30% – Macro Business

- [China] How Much Would China’s GDP Respond to a Slowdown in Housing Activity? – Federal Reserve Bank of Kansas City

- [Iceland] Iceland’s house prices continue to rise, albeit at a slower pace – Global Property Guide

- [Ireland] House prices in Ireland continue to rise at breakneck speed – Global Property Guide

- [Portugal] Portugal’s housing market remains robust – Global Property Guide

- [Portugal] Qué son las “visas doradas” y por qué causan polémica en Portugal – BBC

- [Romania] Romania’s house price growth decelerating sharply – Global Property Guide

- [Spain] The financial transmission of housing bubbles: Evidence from Spain – VoxEU

- [Spain] Te presentamos a tu casero: se llama Blackstone y es dueño de medio Madrid – GQ

- [Sweden] Sweden’s house price boom is officially over – Global Property Guide

- [Switzerland] Holes in Swiss property market ring mortgage alarm bells – Reuters

- [Thailand] Thailand’s house prices rising strongly again – Global Property Guide

- [United Kingdom] Housing affordability: Is new local supply the key? – Sage Journals

Photo by Aliis Sinisalu

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, September 13, 2018

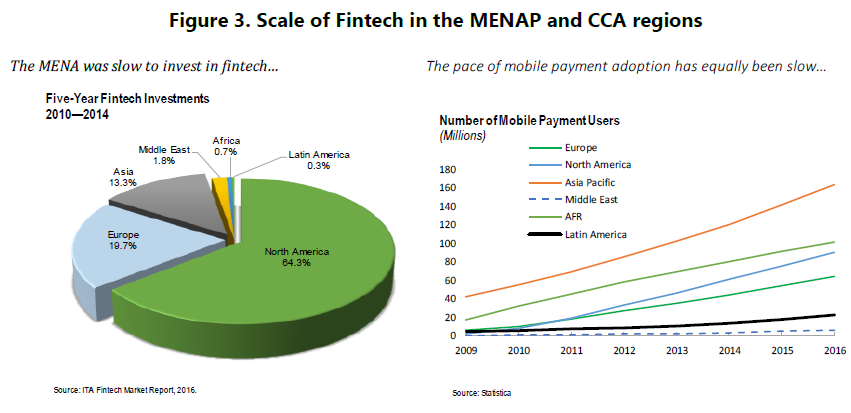

Fintech, Inclusive Growth and Cyber Risks in the MENAP and CCA Regions

From a new IMF working paper:

“Financial technology (fintech) is emerging as an innovative way to achieve financial inclusion and the broader objective of inclusive growth. In addition to improving the speed, convenience, and efficiency of financial services, fintech has potential to promote financial inclusion. More specifically, it can enhance access to affordable financial services for unbanked populations and underserved small and medium sized enterprises (SMEs); reduce delays and costs in cross-border remittances; foster efficiencies and transparency in government operations, which helps reduce corruption, and facilitate social and humanitarian transfers in a manner that preserves human dignity.”

“For the Middle East, North Africa, Afghanistan and Pakistan (MENAP) and Caucasus and Central Asia (CCA) regions, fintech has a particularly valuable role to play as these potential benefits are aligned with the regions’ policy priorities. Both regions have countries with large unbanked populations, SMEs whose growth is constrained by limited access to finance, high youth unemployment, large remittance markets and informal transfers (Hawala), undiversified economies, vulnerabilities to terrorism, large income disparities, large displaced populations, and endemic corruption. Fintech innovations and underlying technologies can contribute to the solutions for many of these challenges.”

“The scale and pace of fintech in MENAP and CCA countries, however, lags other regions, and fintech is yet to foster an inclusive digital economy. Although there is significant diversity in the pace with which countries in both regions are adopting fintech, overall investment into fintech and the uptake of fintech and mobile financial services have been low compared to other regions. There also continues to be a strong preference for cash payments in the Middle East, despite the growth of e-commerce transactions. Consequently, the potential gap remains large in key areas such as financial inclusion, access to SMEs, diversification, reducing informal sector and the broader objective of inclusive growth.”

From a new IMF working paper:

“Financial technology (fintech) is emerging as an innovative way to achieve financial inclusion and the broader objective of inclusive growth. In addition to improving the speed, convenience, and efficiency of financial services, fintech has potential to promote financial inclusion. More specifically, it can enhance access to affordable financial services for unbanked populations and underserved small and medium sized enterprises (SMEs); reduce delays and costs in cross-border remittances;

Posted by at 4:05 PM

Labels: Inclusive Growth

Subscribe to: Posts