Tuesday, February 19, 2019

Housing Market in Nepal

From the IMF’s latest report on Nepal:

“Existing macroprudential measures, including the loan-to-value ratios on car loans and residential real estate, and limits on real estate sector exposure have helped to contain credit growth, but need to be tightened further. Staff welcomes the authorities’ stated intention to

adhere to the ceiling on the loan-to-deposit (LTD) ratio—so-called credit-to-core capital cum deposit (CCD) ratio.2 Several carve-outs have been introduced over time to provide more room for credit growth. These carve-outs, including the recent decision to allow funds obtained through interbank borrowing to count as deposits, should be phased out and the authorities should resist banks’ pressures for further effective relaxation of the CCD ratio and other macroprudential rules.”

From the IMF’s latest report on Nepal:

“Existing macroprudential measures, including the loan-to-value ratios on car loans and residential real estate, and limits on real estate sector exposure have helped to contain credit growth, but need to be tightened further. Staff welcomes the authorities’ stated intention to

adhere to the ceiling on the loan-to-deposit (LTD) ratio—so-called credit-to-core capital cum deposit (CCD) ratio.2 Several carve-outs have been introduced over time to provide more room for credit growth.

Posted by at 3:23 PM

Labels: Global Housing Watch

Labour mobility and adjustment to shocks in the euro area: The role of immigrants

From a new VOX post on the role of immigrants:

“The response of labour supply to negative shocks is different across regions due to varying levels of labour mobility. This column shows that the elasticity of labour supply in response to economic shocks is lower in the euro area than in the US, suggesting that a lack of labour mobility may be an obstacle to labour market adjustments in the euro area. Policies aimed at reducing the complexities of migrating for jobs could help ease this mobility gap.”

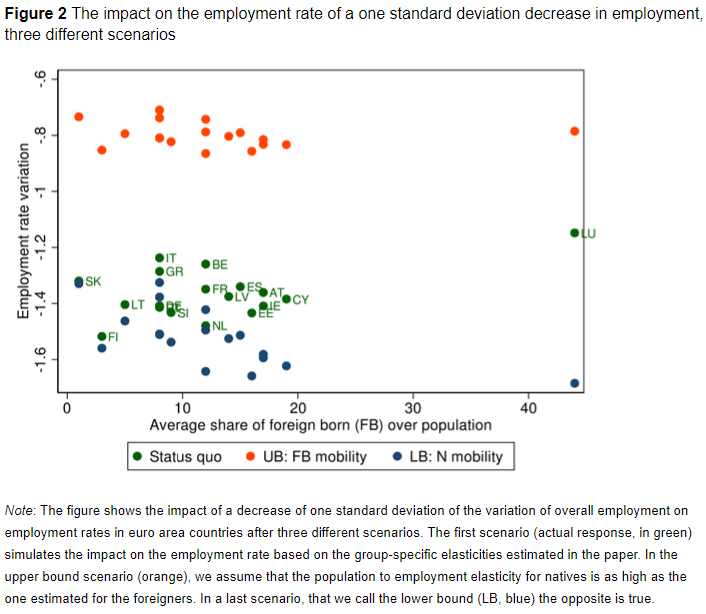

“The higher mobility of migrants implies that they can act as a buffer and reduce the fluctuations of the employment rate in response to regional shocks to employment. A simple counterfactual exercise can help appreciate the magnitude of such contribution. We first simulate the impact of a 1.9% decrease in the level of employment on the employment rate in each euro area country using the elasticities estimated for natives and foreign-born (the value is equal to one standard deviation of the series of overall employment variations). In this status quo scenario, the employment rate falls in all countries by 13% on average (the green dots in Figure 2). We then focus on two alternative scenarios, and simulate the same impact assuming that all individuals had the natives’ (low) elasticity or the foreigners’ (high) elasticity.

Comparing the first (lower bound) scenario to the status quo informs us on the current contribution of mobile foreign-born individuals in absorbing the shock – our estimates suggest that they help reduce its impact on employment rates at the country level by around 7% (to 1.4% on average, see the blue dots). And if all individuals had the same propensity to move as foreigners (as in the second, upper bound scenario), the impact of the negative employment shock would be halved (orange dots). These patterns are common to all euro area countries.”

From a new VOX post on the role of immigrants:

“The response of labour supply to negative shocks is different across regions due to varying levels of labour mobility. This column shows that the elasticity of labour supply in response to economic shocks is lower in the euro area than in the US, suggesting that a lack of labour mobility may be an obstacle to labour market adjustments in the euro area.

Posted by at 10:53 AM

Labels: Inclusive Growth

The forecasting record

From a new post:

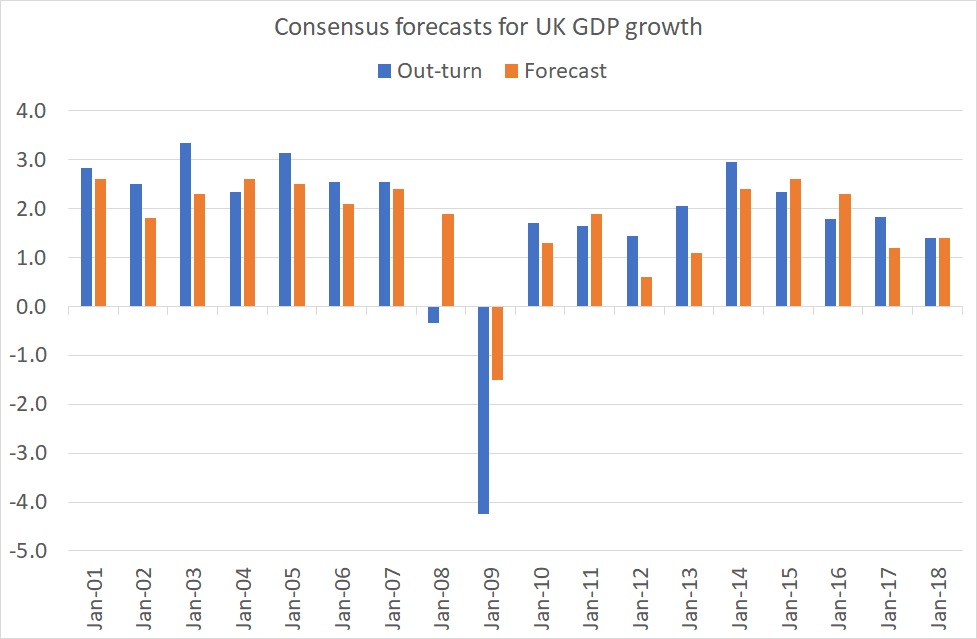

“The ONS says GDP grew by 1.4% last year. 1.4% is a significant number: it is exactly what the private sector economists surveyed by the Treasury predicted in December 2017 that growth would be in 2018.

Granted, this bulls-eye might not survive future revisions to GDP estimates. But it reminds us that economists’ forecasts for growth are often not too bad.

My chart shows the point. It compares forecasts made in December for growth the following year to actual growth since 2001. Most of the time, the forecasts aren’t too far out. Where they go badly wrong is in recessions. Economists don’t see these coming. In December 2007 they forecast that GDP would grow 1.9 per cent in 2008. In fact it shrank. And even in December 2008 – after the banking crisis – they grossly under-predicted the depth of the recession.

This fitted the pattern. Back in 2000 Prakash Loungani wrote:

The record of failure to predict recessions is virtually unblemished. Only two of the 60 recessions that occurred around the world during the 1990s were predicted a year in advance. That may seem like a tough standard to impose on forecast accuracy. Maybe so—but two-thirds of those recessions remained un-detected seven months before they occurred.

In December 1990, for example, UK economists forecast growth of 0.3% in 1991. In fact, we got a 1% drop.

Economic forecasts, then, are reasonably OK except when we really need them.

Why? One possibility, suggested by Loungani, is that economists are slow to update their forecasts in light of news. One bit of evidence for this is that they also under-predicted the boom of 1988 (probably because they over-estimated the adverse effect of the 1987 stock market crash). Another possibility is that mainstream forecasters lack incentives to break with the consensus and predict recessions: it’s better to be wrong in a crowd. It’s for this reason that it is mavericks and those wanting to make a name for themselves who predict doom.

I suspect, though, that there’s something else. It’s that recessions are caused by things which are hard for macroeconomists to discern. For example, Xavier Gabaix shows how they can be caused by failures at large firms. And Daron Acemoglu and colleagues have described how they can be amplified by network effects: trouble at a firm at the centre of a hub can spill over into other firms whereas trouble at a spoke does not. These are both part of the story of the 2008-09 crisis.

Macroeconomists are tolerably good at predicting fluctuations in aggregate demand. It is other things – such as supply shocks, network and peer effects or banking crises – they’re not so good at foreseeing.

It doesn’t automatically follow, however, that recessions are wholly unpredictable. US evidence strongly suggests that inverted yield curves lead (with a variable lag) to economic downturns. I suspect this is for the same reason that consumption-wealth ratios help predict bad times. It’s because such data aggregates the dispersed and fragmentary knowledge of countless individuals. There some specific conditions when the wisdom of crowds works better than experts.”

From a new post:

“The ONS says GDP grew by 1.4% last year. 1.4% is a significant number: it is exactly what the private sector economists surveyed by the Treasury predicted in December 2017 that growth would be in 2018.

Granted, this bulls-eye might not survive future revisions to GDP estimates. But it reminds us that economists’ forecasts for growth are often not too bad.

My chart shows the point.

Posted by at 10:51 AM

Labels: Forecasting Forum

Two hundred years of health and medical care

From a new VOX post:

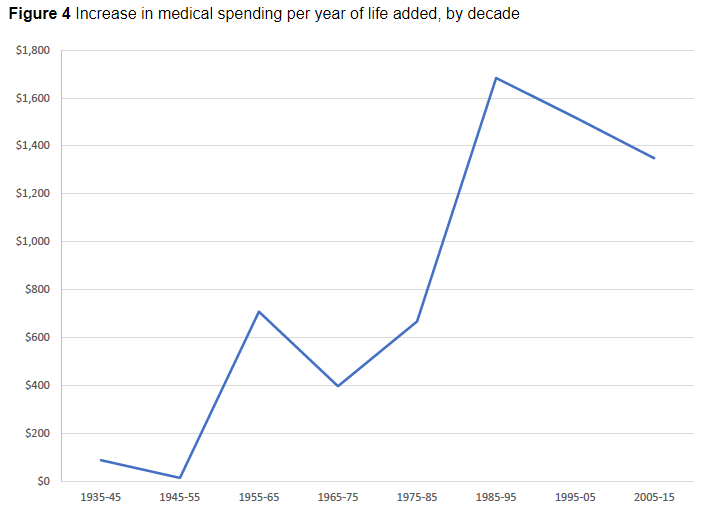

“Growth in life expectancy during the last two centuries has been attributed to environmental change, productivity growth, improved nutrition, and better hygiene, rather than to advances in medical care. This column traces the development of medical care and the extension of longevity in the US from 1800 forward to provide a long-term look at health and health care in the US. It demonstrates that the contribution of medical care to life-expectancy gains changed over time.”

“Researchers agree that there is a recent slowdown in national health expenditures across all age groups (Figure 4), but there is little agreement on exactly why and when it started. Cutler and Sahni (2013) considered the role of the recession and estimated that it accounted for 37% of the slowdown between 2007 and 2012. They noted that a decline in private insurance coverage and cuts to some Medicare payment rates accounted for another 8% of the slowdown, leaving 55% of the spending slowdown unexplained. Researchers who asked whether the Affordable Care Act could explain part of the slowdown reached mixed conclusions about the importance of its contribution (McWilliams et al. 2013, Song et al. 2012, Colla et al. 2012).

Whatever the case may be, the slowdown began in the early 2000s, prior to the implementation of the Affordable Care Act. Chandra et al. (2013) argued that the three main causes for the slowdown were the rise in high-deductible insurance plans, state-level efforts to control Medicaid costs, and a general slowdown in the diffusion of new technology, particularly for use by the Medicare population.

The diffusion of technologies previously used among the elderly to the non-elderly population (e.g. elective hip or knee replacement for people with severe arthritis) might explain some of the relative change but is not the full story. The recent reduction in the relative growth of medical spending on people over 65 and the slowdown in the real growth rate of spending for all citizens remain to be fully understood. ”

From a new VOX post:

“Growth in life expectancy during the last two centuries has been attributed to environmental change, productivity growth, improved nutrition, and better hygiene, rather than to advances in medical care. This column traces the development of medical care and the extension of longevity in the US from 1800 forward to provide a long-term look at health and health care in the US. It demonstrates that the contribution of medical care to life-expectancy gains changed over time.”

Posted by at 10:45 AM

Labels: Inclusive Growth

The China shock and its impact on income inequality in Vietnam

From a new VOX post:

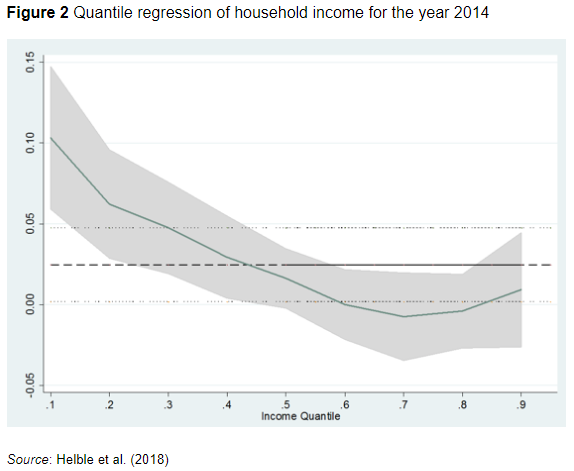

“The sudden rise in trade between China and the US – known as the ‘China shock’ – has been the subject of numerous studies, but the even more dramatic increase in trade between China and developing countries in Asia has been somewhat overlooked. This column studies the impact of the China shock on income inequality in Vietnam. It suggests that increased trade with China reduced income inequality. It resulted in income growth for the lowest income quantiles while higher income groups saw their income decline.”

From a new VOX post:

“The sudden rise in trade between China and the US – known as the ‘China shock’ – has been the subject of numerous studies, but the even more dramatic increase in trade between China and developing countries in Asia has been somewhat overlooked. This column studies the impact of the China shock on income inequality in Vietnam. It suggests that increased trade with China reduced income inequality.

Posted by at 10:39 AM

Labels: Inclusive Growth

Subscribe to: Posts