Friday, March 1, 2019

Housing Market in Malta

From the IMF’s latest report on Malta:

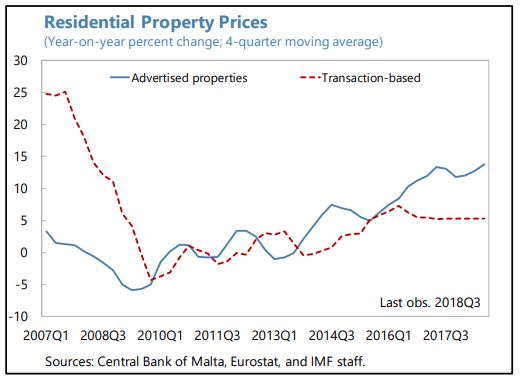

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

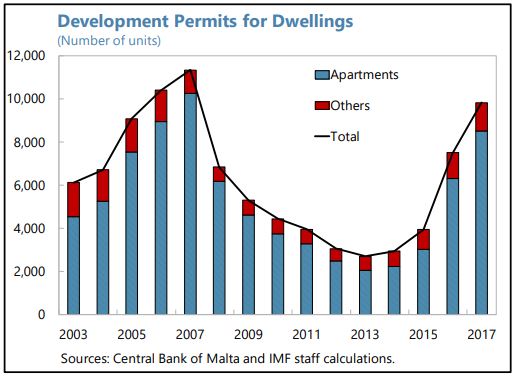

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge, recent house price trends can largely be explained by fundamentals such as e.g., strong immigration flows, rising disposable income, portfolio rebalancing towards property investment and a delayed supply response. Other factors such as the extension of the first-time home-buyer stamp duty relief, the reduced tax rate on rental income, surging demand for tourist accommodation and, for the high-end segment, the IIP may also have played a role (but are not directly controlled for in the empirical analysis conducted in Annex I).

Banks’ exposure to housing-market-related risks is high and increasing, and the introduction of macroprudential measures should proceed as planned. All the more so that households’ indebtedness is relatively high, low income households are vulnerable to housing price corrections and flexible interest rate on mortgages are prevalent.7 Against this backdrop, recent efforts to close data gaps (loan-level data collection) and the planned introduction of borrowerbased macroprudential measures such as caps to loan-to-value (LTV) ratios at origin, stressed debt service-to-income (DSTI) limits, and amortization requirements are steps in the right direction (see text table).

To be more effective, the new borrower-based measures could be refined in due course and exemptions to the LTV limit could be narrowed. To avoid excessive risk concentration, speed limits should be defined in terms of the total value of new loans, not in terms of the number of new loans, and speed limits for loans against secondary and buy-to-let properties, the likely most speculative segment, should be lowered as soon as concerns about any initial disruptions dissipate. Finally, the scope of the new borrower-based measures should be extended to also cover non-bank mortgage loans.

Rapidly rising housing costs are affecting vulnerable households. The government recently relaxed the eligibility requirements for rent subsidies, but the scheme should be periodically reviewed to ensure it remains targeted on low-income households. Further efforts should also be envisaged to accelerate the provision of social housing, including by fiscally incentivizing private investments.

Authorities’ Views

Rapidly rising property prices are viewed by the authorities as mainly reflecting economic fundamentals. Inflows of foreign labor and higher income in general are fueling housing demand. The authorities also see the impact of tax benefits for first and second-time home buyers, the reduced tax rate on rental income and the IIP as marginal. They stressed that the planned borrower-based macroprudential measures were carefully calibrated to have minimal market impact upon their introduction. The authorities have agreed that there is room for refinement, in due course, and emphasized that they can easily recalibrate the measures to mitigate financial stability risks emanating from the housing market in a timely and effective manner. The authorities also recognize the growing importance of making housing more affordable for vulnerable households. They emphasized the progressive nature of the new rent subsidy scheme. Projects are underway to increase the stock of social and affordable housing.”

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge,

Posted by at 10:52 AM

Labels: Global Housing Watch

A profile of Branko Milanovic, a leading scholar of inequality

Chris Wellisz profiles Branko Milanovic, a leading scholar of inequality for the March 2019 issue of Finance & Development:

“As a child growing up in Communist Yugoslavia, Branko Milanovic witnessed the protests of 1968, when students occupied the campus of the University of Belgrade and hoisted banners reading “Down with the Red bourgeoisie!”

Milanovic, who now teaches economics at the City University of New York, recalls wondering whether his own family belonged to that maligned group. His father was a government official, and unlike many Yugoslav kids at the time, Milanovic had his very own bedroom—a sign of privilege in a nominally classless society. Mostly he remembers a sense of excitement as he and his friends loitered around the edge of the campus that summer, watching the students sporting red Karl Marx badges.

“I think that the social and political aspects of the protests became clearer to me later,” Milanovic says in an interview. Even so, “1968 was, in many ways, a watershed year” in an intellectual journey that has seen him emerge as a leading scholar of inequality. Decades before it became a fashion in economics, inequality would be the subject of his doctoral dissertation at the University of Belgrade.

Today, Milanovic is best known for a breakthrough study of global income inequality from 1988 to 2008, roughly spanning the period from the fall of the Berlin Wall—which spelled the beginning of the end of Communism in Europe—to the global financial crisis.

The 2013 article, cowritten with Christoph Lakner, delineated what became known as the “elephant curve” because of its shape (see chart). It shows that over the 20 years that Milanovic calls the period of “high globalization,” huge increases in wealth were unevenly distributed across the world. The middle classes in developing economies—mainly in Asia—enjoyed a dramatic increase in incomes. So did the top 1 percent of earners worldwide, or the “global plutocrats.” Meanwhile, the lower middle classes in advanced economies saw their earnings stagnate.

The elephant curve’s power lies in its simplicity. It elegantly summarizes the source of so much middle class discontent in advanced economies, discontent that has turbocharged the careers of populists from both extremes of the political spectrum and spurred calls for trade barriers and limits on immigration.”

Continue reading here.

Chris Wellisz profiles Branko Milanovic, a leading scholar of inequality for the March 2019 issue of Finance & Development:

“As a child growing up in Communist Yugoslavia, Branko Milanovic witnessed the protests of 1968, when students occupied the campus of the University of Belgrade and hoisted banners reading “Down with the Red bourgeoisie!”

Milanovic, who now teaches economics at the City University of New York, recalls wondering whether his own family belonged to that maligned group.

Posted by at 10:44 AM

Labels: Inclusive Growth

Housing View – March 1, 2019

On cross-country:

- Social rental intermediation. How private landlords can contribute to solve the housing crisis? – Housing Europe

- What are some of the primary driving forces behind the Urban Housing Crunch? – Forbes

- What if the future of housing means accepting that a home isn’t permanent? – Quartz

- Macroprudential approaches to non-performing loans – ESRB

On the US:

- How Monetary Policy Shaped the Housing Boom – New York University

- Inside the Rise and Fall of a Multimillion-Dollar Airbnb Scheme – New York Times

- Rents Are Up? That Depends on Where You Live – New York Times

- California housing crisis podcast: Will a boom in building make housing more affordable? – Los Angeles Times

- UCLA Ziman Program – a First Nationwide – Teaches Affordable Housing Development – UCLA

- U.S. housing outlook stuck in a lull as economy dulls: Reuters poll – Reuters

- Home Prices in 20 U.S. Cities Rise by Least in Four Years – Bloomberg

- Real House Prices and Price-to-Rent Ratio in December – Calculated Risk

- Trouble In The Housing Market – Forbes

- Slowing Home Price Growth and Construction Hit Housing Market – Wall Street Journal

- Is Housing in Your City Getting Unaffordable? Here’s How You Can Help – Citylab

- Can housing reform survive a hall of mirrors? – Boston Globe

- Seattle-area home price cooldown not reaching cheaper parts of housing market – Seattle Times

- California’s housing supply law fails to spur enough construction, study says – Los Angeles Times

On other countries:

- [Australia] Australian Home Lending Now Weakest Since the Mid-1980s – Bloomberg

- [Australia] House price falls in Sydney and Melbourne not all bad, Reserve Bank head says – The Guardian

- [Australia] Australia’s housing data still terrible across the board – Variant Perception

- [Canada] Affordable housing becomes singular focus of Toronto’s new real estate czar – Globe and Mail

- [Canada] Bank of Canada says housing crunch threatens Canadian economy – Fraser Institute

- [Canada] Canada’s housing market set for years of subdued price rises: Reuters poll – Reuters

- [Canada] Another budget, another missed opportunity to tackle B.C.’s housing shortage – Fraser Institute

- [China] Capital Gains Tax would see house prices fall as investors flee market ahead of tax’s implementation – REINZ – New Zealand Herald

- [China] China’s Huge Number of Vacant Apartments Are Causing a Problem – Citylab

- [Denmark] Danish Study Quantifies Impact of House Prices on Consumption – Bloomberg

- [Hong Kong] Why Hong Kong Is Claiming Golf Greens for New Housing – Citylab

- [India] India Cuts Tax on Housing to Boost Real Estate Before Elections – Bloomberg

- [Ireland] Ireland’s house price rises continue, albeit at a much slower pace – Global Property Guide

- [Israel] Changes in the share of first home buyers among young people, based on income level – Bank of Israel

- [Netherlands] House prices expected to keep rising this year, homeownership unattainable for more and more people – Rabobank

- [New Zealand] New Zealand Locks the Doors From the Inside – New York Times

- [New Zealand] Sale of portable cabins booms in New Zealand amid housing crisis – The Guardian

- [Sweden] Refugees and apartment prices: A case study to investigate the attitudes of home buyers – Regional Science and Urban Economics

- [United Kingdom] No-deal Brexit would take a chip off UK home values – Reuters poll – Reuters

- [United Kingdom] Housing costs: Five surprises explained – BBC

- [United Kingdom] A solution to the housing crisis? – Financial Times

On cross-country:

- Social rental intermediation. How private landlords can contribute to solve the housing crisis? – Housing Europe

- What are some of the primary driving forces behind the Urban Housing Crunch? – Forbes

- What if the future of housing means accepting that a home isn’t permanent? – Quartz

- Macroprudential approaches to non-performing loans – ESRB

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, February 27, 2019

Macro reasons to loath protectionism

From a VoxEU post by Davide Furceri, Swarnali Ahmed Hannan, Jonathan D. Ostry, Andrew Rose:

“It seems an appropriate time to study what, if any, have been the macroeconomic consequences of tariffs in practice. Using a straightforward methodology to estimate flexible impulse response functions, and data that span several decades and 151 countries, this column finds that tariff increases have, on average, engendered adverse macroeconomic and distributional consequences: a fall in output and labour productivity, higher unemployment, higher inequality, and negligible effects on the trade balance (likely owing to real exchange rate appreciation when tariffs rise). The aversion of the economics profession to the deadweight loss caused by protectionism seems warranted.

One of the most pressing issues on the international agenda these days is protectionism. The US’ trade war with China has created international tension that is infecting stock markets worldwide, exacerbated by other disputes such as the renegotiation of NAFTA, Brexit, and US steel and aluminium tariffs. One ingredient curiously absent from this turbulence is disagreement among the experts on the merits (or lack thereof) on the underlying issue. Indeed, more than on any other issue, there is agreement amongst economists that international trade should be free.1

Economists have been aware of the senselessness of protectionism since at least Adam Smith. In general, economists believe that freely functioning markets best allocate resources, at least absent some distortion, externality or other market failure; competitive markets tend to maximise output by directing resources to their most productive uses. Of course, there are market imperfections, but tariffs – taxes on imports – are almost never the optimal solution to such problems. Tariffs encourage the deflection of trade to inefficient producers and smuggling to evade the tariffs; such distortions reduce productivity, income and welfare. Further, consumers lose more from a tariff than producers gain, so there is ‘deadweight loss’ as well as inequality (if production tends to be owned by the rich). The redistributions associated with tariffs tend to create vested interests, so harms tend to persist. Broad-based protectionism can also provoke retaliation which adds further costs. All these losses to output are exacerbated if inputs are protected, since this adds to production costs.

Discussions of market imperfections and the like are naturally microeconomic in nature (Grossman and Rogoff 1995). Accordingly, most analysis of trade barriers focuses on individual industries. International commercial policy tends not to be used as a macroeconomic tool, probably because of the availability of superior alternatives such as monetary and fiscal policy. In addition, there are strong theoretical reasons that economists abhor the use of protectionism as a macroeconomic policy; for instance, the broad imposition of tariffs may lead to offsetting changes in exchange rates (Dornbusch, 1974). And while the imposition of a tariff could reduce the flow of imports, it is unlikely to change the trade balance unless it fundamentally alters the balance of saving and investment. The findings of recent studies on the impact of trade would imply that tariffs could hurt output and productivity (Feyrer 2009, Alcala and Ciccone 2004). Further, economists think that protectionist policies helped precipitate the collapse of international trade in the early 1930s, and this trade shrinkage was a plausible seed of WWII. So, while protectionism has not been much used in practice as a macroeconomic policy (especially in advanced countries), most economists also agree that it should not be used as a macroeconomic policy.

The here and now

Times change. Some economies – notably the US – have recently begun to use commercial policy seemingly for macroeconomic objectives. So it seems an appropriate time to study what, if any, the macroeconomic consequences of tariffs have actually been in practice. Most of the predisposition of the economics profession against protectionism is based on evidence that is either a) theoretical, b) micro, or c) aggregate and dated. Accordingly, in our recent research (Furceri et al. 2018), we study empirically the macroeconomic effects of tariffs using recent aggregate data.”

Continue reading here.

From a VoxEU post by Davide Furceri, Swarnali Ahmed Hannan, Jonathan D. Ostry, Andrew Rose:

“It seems an appropriate time to study what, if any, have been the macroeconomic consequences of tariffs in practice. Using a straightforward methodology to estimate flexible impulse response functions, and data that span several decades and 151 countries, this column finds that tariff increases have, on average, engendered adverse macroeconomic and distributional consequences: a fall in output and labour productivity,

Posted by at 10:18 AM

Labels: Macro Demystified

Macroeconomic Gains from Reforming the Agri-Food Sector: The Case of France

From an IMF working paper by Nicoletta Batini:

“France is the top agricultural producer in the European Union (EU), and agriculture plays a prominent role in the country’s foreign trade and intermediate exchanges. Reflecting production volumes and methods, the sector, however, also generates significant negative environmental and public health externalities. Recent model simulations show that a well-designed shift in production and consumption to make the former sustainable and align the latter with recommended values can curb these considerably and generate large macroeconomic gains. I propose a policy toolkit in line with the government’s existing sectoral policies that can support this transition.”

From an IMF working paper by Nicoletta Batini:

“France is the top agricultural producer in the European Union (EU), and agriculture plays a prominent role in the country’s foreign trade and intermediate exchanges. Reflecting production volumes and methods, the sector, however, also generates significant negative environmental and public health externalities. Recent model simulations show that a well-designed shift in production and consumption to make the former sustainable and align the latter with recommended values can curb these considerably and generate large macroeconomic gains.

Posted by at 10:15 AM

Labels: Energy & Climate Change

Subscribe to: Posts