Monday, June 3, 2019

Stranded! How Rising Inequality Suppressed US Migration and Hurt Those Left Behind

From an IMF working paper by Tamim Bayoumi and Jelle Barkema:

“Using bilateral data on migration across US metro areas, we find strong evidence that increasing house price and income inequality has reduced long distance migration, the type most linked to jobs. For those migrating uphill, from a less to a more prosperous location, lower mobility is driven by increasing house price inequlity, as the disincentives from higher house prices dominate the incentives from higher earnings. By contrast, increasing income inequality drives the fall in downhill migration as the disincentives from lower earnings dominate the incentives from lower house prices. The model underlines the plight of those trapped in decaying metro areas—those “left behind”.”

From an IMF working paper by Tamim Bayoumi and Jelle Barkema:

“Using bilateral data on migration across US metro areas, we find strong evidence that increasing house price and income inequality has reduced long distance migration, the type most linked to jobs. For those migrating uphill, from a less to a more prosperous location, lower mobility is driven by increasing house price inequlity, as the disincentives from higher house prices dominate the incentives from higher earnings.

Posted by at 5:08 PM

Labels: Inclusive Growth

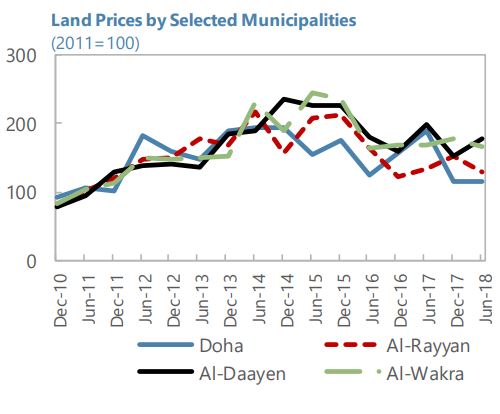

Qatar: Property Market Update

From the IMF’s latest report on Qatar:

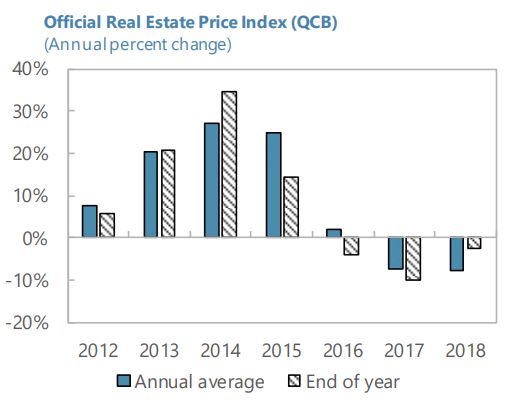

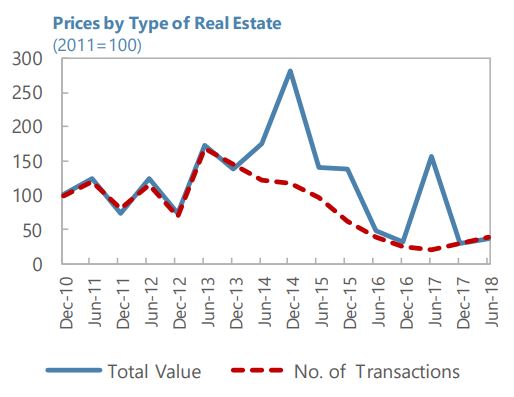

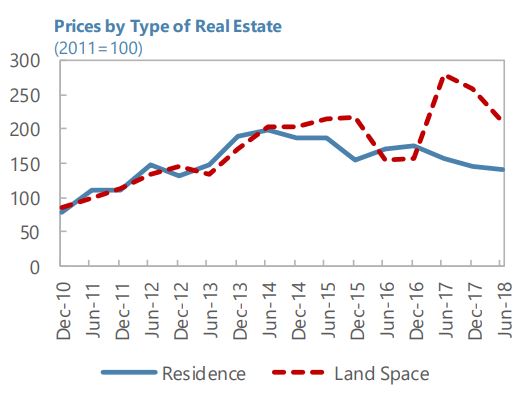

“After a period of rapid growth, real estate prices in Qatar are adjusting to new levels. According to the real estate price index developed by QCB, following an 82 percent increase during 2012–16, real estate prices fell by 15 percent during 2017–18. Data produced by the Ministry of Justice indicate the following trends:

- Both the volume and number of transactions are down since 2013–2014 peak. As prices have decreased, some owners seem to be holding off to their properties rather than selling at depressed prices.

- Land prices are holding up better than properties with a rebound in prices during 2017 before adjustment in 2018. Residence prices have been on a declining trend since mid-2014, though there are signs that the slowdown is flattening.

- In terms of regions, land prices in Al Daayen are holding on better which could be due to the active development of Lusail City and 2022 World Cup projects. Similarly, land prices in Al Wakra have been stable in the past years due to major infrastructural projects.”

From the IMF’s latest report on Qatar:

“After a period of rapid growth, real estate prices in Qatar are adjusting to new levels. According to the real estate price index developed by QCB, following an 82 percent increase during 2012–16, real estate prices fell by 15 percent during 2017–18. Data produced by the Ministry of Justice indicate the following trends:

- Both the volume and number of transactions are down since 2013–2014 peak.

Posted by at 10:51 AM

Labels: Global Housing Watch

Friday, May 31, 2019

The radical plan to change how Harvard teaches economics

From Vox:

“If Harvard has a most famous course, it’s Economics 10.

The introductory economics class is reliablyone of the most popular courses offered to undergraduates. It’s usually taught in a massive Hogwartsian auditorium, where hundreds of students either dutifully take notes or mess around on laptops as one of the school’s star economists leads them through the basics of supply and demand.

Because Harvard has a tendency to set the pattern for other universities, Ec 10’s textbook is a massive best-seller, used at dozens of other schools, earning its author, professor Greg Mankiw, an estimated $42 million in royalties since it was first released in 1998. Mankiw’s introduction to economics has set the tone not just at Harvard but for how Econ 101 is taught across the country.

Mankiw’s textbook covers the abstract theory that underpins economics as it has been understood for decades. It is about supply and demand, about how prices can be used to match production of a good to its consumption, and about the power of markets as a tool for allocating scarce resources. Students in Ec 10 are asked to plot supply and demand curves, to solve simple word problems about what happens when the mayor of Smalltown, USA, imposes a tax on hotel rooms.

The idea is to impart a basic theory, to lay a foundation for understanding how society works. And that theory strongly implies that markets tend to work without much intervention, and that things like minimum wages might hurt more than help.

But another Harvard economist has a different idea of how to introduce students to economics.

Raj Chetty, a prominent faculty member whom Harvard recently poached back from Stanford, this spring unveiled “Economics 1152: Using Big Data to Solve Economic and Social Problems.” Taught with the help of lecturer Greg Bruich, the class garnered 375 students, including 363 undergrads, in its first term. That’s still behind the 461 in Ec 10 — but not by much.”

Continue reading here.

Raj Chetty, professor of economics at Harvard University, poses for a portrait at the Opportunity Insights offices. (Kayana Szymczak for Vox)

From Vox:

“If Harvard has a most famous course, it’s Economics 10.

The introductory economics class is reliablyone of the most popular courses offered to undergraduates. It’s usually taught in a massive Hogwartsian auditorium, where hundreds of students either dutifully take notes or mess around on laptops as one of the school’s star economists leads them through the basics of supply and demand.

Because Harvard has a tendency to set the pattern for other universities,

Posted by at 4:05 PM

Labels: Profiles of Economists

Housing View – May 31, 2019

On cross-country:

- Financial Stability Review, May 2019 – European Central Bank

- How Housing Supply Became the Most Controversial Issue in Urbanism – CityLab

- Impacts of urban renewal on neighborhood housing prices: predicting response to psychological effects – Journal of Housing and the Built Environment

- “The ‘housing question’ is no longer simply about housing” – Housing Europe

On the US:

- The Fair Housing Act at 50 – Cityspace

- After Amazon HQ2: New York and D.C. Offer a Tale of Two Housing Markets – Yahoo

- Have Changes in Financing Contributed to the Loss of Low-Cost Rental Units and Rent Increases? – Harvard Joint Center for Housing Studies

- Regulations And Failed Governance Are The Root Causes Of California’s Housing Crisis – Hoover Institution

- Monkkonen Guides Discussion of L.A.’s Housing Needs – UCLA

On other countries:

- [Canada] RBC Sidesteps Canada’s Housing Slump With Mortgage Growth – Bloomberg

- [China] Understanding China’s ‘One-Way Bet’ Property Market – Washington Post

- [Hong Kong] Hong Kong Property Back in Bubble Territory, Reinhart Says – Bloomberg

On cross-country:

- Financial Stability Review, May 2019 – European Central Bank

- How Housing Supply Became the Most Controversial Issue in Urbanism – CityLab

- Impacts of urban renewal on neighborhood housing prices: predicting response to psychological effects – Journal of Housing and the Built Environment

- “The ‘housing question’ is no longer simply about housing” – Housing Europe

On the US:

- The Fair Housing Act at 50 – Cityspace

- After Amazon HQ2: New York and D.C.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, May 30, 2019

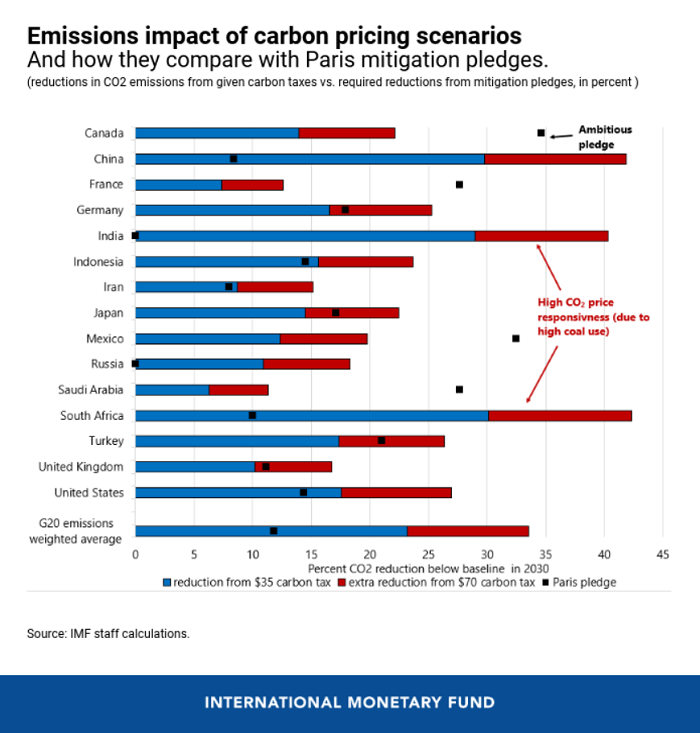

A case for second-best solutions in climate policy

From the Financial Times:

The Greens’ surge in last week’s European Parliament elections confirmed that a growing share of voters want their politicians to do something about climate change. But it is far from clear that the majority is ready to pay the higher energy and fuel prices that would result from any serious effort to limit the rise in global temperatures — and that would hit some groups much harder than others.

Economists, who for years have been debating the best ways to fine-tune carbon pricing mechanisms, are now turning their attention to the bigger challenges of political economy.

A paper by IMF staff, published earlier this month, shows just how far off we are from making carbon as expensive as it needs to be. Many major economies could achieve the emissions cuts pledged under the 2015 Paris accord with a carbon price of $35 per tonne, they calculate — a level that would roughly double coal prices and add 5 per cent to 7 per cent to pump prices for road fuels.

But to contain global warming to 2 degrees centigrade above pre-industrial levels would require a global carbon price of about $70 per tonne, they estimate. At present, despite a proliferation of national and sub-national carbon taxes and trading schemes, the average global carbon price is $2 per tonne.”

Continue reading here.

From the Financial Times:

The Greens’ surge in last week’s European Parliament elections confirmed that a growing share of voters want their politicians to do something about climate change. But it is far from clear that the majority is ready to pay the higher energy and fuel prices that would result from any serious effort to limit the rise in global temperatures — and that would hit some groups much harder than others.

Posted by at 8:47 AM

Labels: Energy & Climate Change

Subscribe to: Posts