Friday, July 19, 2019

Housing View – July 19, 2019

On cross-country:

- House prices up by 4.0% in both the euro area and the EU – Eurostat

On the US:

- Is rent control making a comeback? – Brookings

- Tackling zoning to help the middle class: 5 policy approaches – Brookings

- Survey Shows Decline in Foreign Investment in U.S. Residential Real Estate – National Association of Realtors

- 5 Lessons from Cities On Affordable Housing – Politico

- Can Robots Solve the Affordable Housing Crisis? – Politico

- Only Washington Can Solve the Nation’s Housing Crisis – New York Times

- Amazon HQ2 Is Upending Northern Virginia’s Already Unstable Housing Market – New York Times

- Property taxes stunt Chicago’s house price growth – Financial Times

- Is California’s apartment market broken? – Brookings

- Housing Affordability and Zoning Reform – Cato

- Wave of Hispanic Buyers Boosts U.S. Housing Market – Wall Street Journal

- A Home Builder Perspective on Housing Affordability and Construction Innovation – Harvard Joint Center for Housing Studies

- Gentrification ‘benefits local residents’, research finds – Financial Times

- Housing’s ‘Missing Middle’ Keeps Shrinking – Bloomberg

- Steep Slowdown Projected in Home Improvements – Harvard Joint Center for Housing Studies

On other countries:

- [China] When Affordable Housing in Shanghai Is a Bed in the Kitchen – Citylab

- [Netherlands] “Mortgage Interest Tax Deduction in the Netherlands: A Welcome Relief” – Netherlands Bank

- [Puerto Rico] Puerto Rico’s housing market improving – Global Property Guide

- [Qatar] Qatar’s housing market is recovering – Global Property Guide

- [United Arab Emirates] UAE’s property prices fall further – Global Property Guide

- [United States]S. housing market gradually cooling – Global Property Guide

*Please note that the Housing View will be on hiatus until September 8.

On cross-country:

- House prices up by 4.0% in both the euro area and the EU – Eurostat

On the US:

- Is rent control making a comeback? – Brookings

- Tackling zoning to help the middle class: 5 policy approaches – Brookings

- Survey Shows Decline in Foreign Investment in U.S. Residential Real Estate – National Association of Realtors

- 5 Lessons from Cities On Affordable Housing – Politico

- Can Robots Solve the Affordable Housing Crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 18, 2019

Why Is Inflation Low Globally?

From the Federal Reserve Bank of San Francisco:

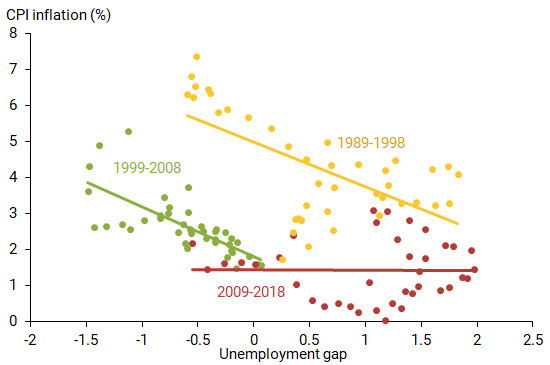

“A hot economy eventually boosts inflation. Such is the simple wisdom of the Phillips curve. Yet inflation across developed countries has been remarkably weak since the 2008 global financial crisis, even though unemployment rates are near historical lows. What is behind this recent disconnect between inflation and unemployment? Contrasting the experiences of developed and developing economies before and after the financial crisis shows that broader factors than monetary policy are at play. Inflation has declined globally, and this trend preceded the financial crisis.

The world economies have mostly recovered from the 2008 financial crisis. In the United States, United Kingdom, and Germany, for example, the unemployment rate is now below 4%, lower than it has been in decades. Tight labor markets are usually a symptom of a healthy economy and thus a rising demand for goods and services. To satisfy such demand, businesses usually raise prices—the basic mechanism underlying the standard economic relationship known as the Phillips curve. Yet, 10 years after the financial crisis, inflation has held remarkably steady. Some researchers therefore argue that the Phillips curve is no longer a useful descriptor of inflation dynamics (Coibion and Gorodnichenko 2015).

In this Economic Letter, we investigate whether the financial crisis has changed the long-standing inner workings of the Phillips curve. We extend the analysis in our previous Economic Letter (Jordà et al. 2019) to include developing economies and analyze three components of the Phillips curve to assess where the links appear to be broken.

Our analysis suggests that news of the death of the Phillips curve in developed economies appears premature. Fluctuations in labor market conditions have been largely offset with appropriate interest rate changes by central banks. Under such conditions, the influence of past inflation has faded, and expectations for future inflation have gravitated toward the central bank’s stated target. On the surface, inflation appears stable at all levels of labor market slack, and the Phillips curve link appears broken. Underneath, however, the Phillips curve could still be at work. The inflation dynamics that we observe could also be explained by a central bank that successfully offsets fluctuations in slack to keep inflation at the target. In less developed economies, central banks often operate under constraints that prevent full monetary policy offsets, which has given a bigger role to feedback from past inflation. That said, inflation has been trending down for the past two decades across developed and developing economies alike. The inevitable conclusion is that there are global forces putting downward pressure on inflation, and it is not just the result of better monetary policy.”

Figure 1

Phillips curve across OECD countries by decade

Continue reading here.

From the Federal Reserve Bank of San Francisco:

“A hot economy eventually boosts inflation. Such is the simple wisdom of the Phillips curve. Yet inflation across developed countries has been remarkably weak since the 2008 global financial crisis, even though unemployment rates are near historical lows. What is behind this recent disconnect between inflation and unemployment? Contrasting the experiences of developed and developing economies before and after the financial crisis shows that broader factors than monetary policy are at play.

Posted by at 10:37 AM

Labels: Macro Demystified

Tuesday, July 16, 2019

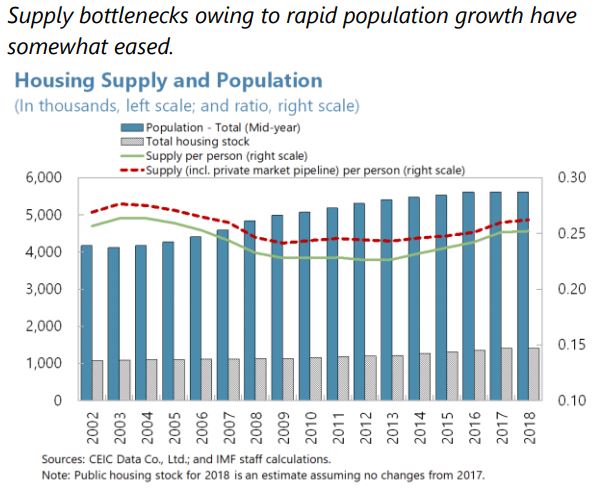

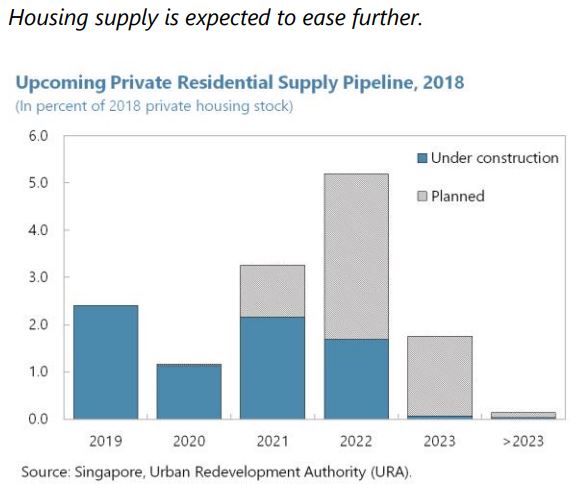

Housing Market in Singapore

From the IMF’s latest report on Singapore:

“The private housing market showed signs of overheating in 2017-18. Average monthly transactions increased by 35 percent in the year through June 2018, compared to the previous two years, and prices increased by 9.1 percent year-on-year in 2018Q2. Developer land purchase activity, including en-bloc purchases, in 2016-2018H1 led to high bidding activity (also implying a rising housing supply over the medium term). The number of foreigners purchasing properties, as well as the transactions values, increased significantly in 2017 and early 2018. In this context, the FSAP analysis found that foreigner residential property purchases had an upward effect on property prices (…).

The authorities tightened macroprudential measures in July 2018 to cool off a rapid increase in real estate prices. In view of rising house prices fueling overvaluation and raising the level of systemic risk, the authorities implemented a package of measures that tightened LTV limits and raised the Additional Buyer’s Stamp Duty (ABSD) for residential property purchases to reduce the risk of a destabilizing price correction. Specifically, for individuals, loan to value (LTV) ratio limits were lowered for all mortgages, and ABSD rates were raised by 5 percentage points, except for Singaporeans and permanent residents buying first properties. For non-individuals, LTVs were lowered and the ABSD was raised by 10 percentage points, with an additional 5 percentage points for housing developers. The differentiation between residents and non-residents in the ABSD was maintained. In response to these policies, house price growth slowed, transactions declined, especially in the private market, and mortgage credit edged down (though remaining high as a share of GDP). Nonetheless, property prices remained moderately overvalued.”

From the IMF’s latest report on Singapore:

“The private housing market showed signs of overheating in 2017-18. Average monthly transactions increased by 35 percent in the year through June 2018, compared to the previous two years, and prices increased by 9.1 percent year-on-year in 2018Q2. Developer land purchase activity, including en-bloc purchases, in 2016-2018H1 led to high bidding activity (also implying a rising housing supply over the medium term). The number of foreigners purchasing properties,

Posted by at 1:32 PM

Labels: Global Housing Watch

Monday, July 15, 2019

The effects of global warming on rural–urban migrations

From a VoxEU post by Giovanni Peri, and Akira Sasahara:

“Though the economic consequences of climate change will be felt across the globe, not all populations will be affected equally. This column examines the impact of rising temperatures on migrant communities. Using historical data from three decades (1970-2000), it finds that higher temperatures increased the number of rural-to-urban migrations in middle-income countries while decreasing rural-to-urban migrations in poor countries. The prospect of climate change leaving large rural populations trapped in poverty adds urgency to the case for addressing the asymmetric effects of global warming.

The annual average temperature is projected to increase by up to 4° Celsius in the coming century (World Bank, 2018). Rising temperatures have been shown to influence various aspects of our economies, including GDP growth (Dell et al. 2012), local conflicts (Bosetti et al. 2018), mortality (Burgess et al. 2014), and agricultural and non-agricultural productions (Burke et al. 2015, Garcia-Verdu et al. 2019). Given the economic effects of weather shocks, we can expect the rise in temperatures to significantly affect migration patterns. The goal of this column is to provide new insight on expected migration responses to climate change by exploiting historical variations in temperatures and migrations.

Net migration rates at the grid cell level

We employ grid cell level data at the 0.5 x 0.5 degree resolution, where one grid cell covers the area of 56 km x 56 km at the equator for three decades: 1970-1980, 1980-1990, and 1990-2000. Decennial net migrations (the number of in-migrants minus the number of out-migrants) come from de Sherbinin et al. (2015) and population data are obtained from Yamagata and Murakami (2015). We define net migration rates by dividing net migration during the decade by the population at the beginning of the decade. Figure 1 shows a map of Europe describing net migrations during the 1990s. Red-coloured cells indicate positive net migration rates (meaning that in-migrations were greater than out-migrations) while blue cells indicate negative net migration rates.”

Continue reading here.

From a VoxEU post by Giovanni Peri, and Akira Sasahara:

“Though the economic consequences of climate change will be felt across the globe, not all populations will be affected equally. This column examines the impact of rising temperatures on migrant communities. Using historical data from three decades (1970-2000), it finds that higher temperatures increased the number of rural-to-urban migrations in middle-income countries while decreasing rural-to-urban migrations in poor countries.

Posted by at 9:46 AM

Labels: Energy & Climate Change

Sunday, July 14, 2019

Explaining High Unemployment in ECCU Countries

A new IMF paper explains unemployment in ECCU countries:

“Unemployment rates in Grenada (GRD), St. Lucia (LCA), and St. Vincent and Grenadines (VCT) have been above 20 percent in recent years. Unemployment in Dominica (DMA) has also been high by international standards even before the natural disasters that recently hit the country. While it is likely that weak employment this decade was partly related to the impact of the global economic downturn, unemployment was already high prior to the global crisis in most of these countries, thus suggesting there are structural factors behind it. This paper evaluates factors that could explain high unemployment in ECCU countries, cyclical and structural.1 Our analysis systemically reviews demand, supply, and institutional factors that could foster unemployment. Within this framework, we analyze the potential impact of the global financial crisis, the downfall of the banana/sugar industries, the hurricanes that frequently hit these countries, the relatively rigid wage setting process, as well as factors that could increase reservation wages.”

A new IMF paper explains unemployment in ECCU countries:

“Unemployment rates in Grenada (GRD), St. Lucia (LCA), and St. Vincent and Grenadines (VCT) have been above 20 percent in recent years. Unemployment in Dominica (DMA) has also been high by international standards even before the natural disasters that recently hit the country. While it is likely that weak employment this decade was partly related to the impact of the global economic downturn,

Posted by at 4:36 PM

Labels: Inclusive Growth

Subscribe to: Posts