Thursday, July 18, 2019

Why Is Inflation Low Globally?

From the Federal Reserve Bank of San Francisco:

“A hot economy eventually boosts inflation. Such is the simple wisdom of the Phillips curve. Yet inflation across developed countries has been remarkably weak since the 2008 global financial crisis, even though unemployment rates are near historical lows. What is behind this recent disconnect between inflation and unemployment? Contrasting the experiences of developed and developing economies before and after the financial crisis shows that broader factors than monetary policy are at play. Inflation has declined globally, and this trend preceded the financial crisis.

The world economies have mostly recovered from the 2008 financial crisis. In the United States, United Kingdom, and Germany, for example, the unemployment rate is now below 4%, lower than it has been in decades. Tight labor markets are usually a symptom of a healthy economy and thus a rising demand for goods and services. To satisfy such demand, businesses usually raise prices—the basic mechanism underlying the standard economic relationship known as the Phillips curve. Yet, 10 years after the financial crisis, inflation has held remarkably steady. Some researchers therefore argue that the Phillips curve is no longer a useful descriptor of inflation dynamics (Coibion and Gorodnichenko 2015).

In this Economic Letter, we investigate whether the financial crisis has changed the long-standing inner workings of the Phillips curve. We extend the analysis in our previous Economic Letter (Jordà et al. 2019) to include developing economies and analyze three components of the Phillips curve to assess where the links appear to be broken.

Our analysis suggests that news of the death of the Phillips curve in developed economies appears premature. Fluctuations in labor market conditions have been largely offset with appropriate interest rate changes by central banks. Under such conditions, the influence of past inflation has faded, and expectations for future inflation have gravitated toward the central bank’s stated target. On the surface, inflation appears stable at all levels of labor market slack, and the Phillips curve link appears broken. Underneath, however, the Phillips curve could still be at work. The inflation dynamics that we observe could also be explained by a central bank that successfully offsets fluctuations in slack to keep inflation at the target. In less developed economies, central banks often operate under constraints that prevent full monetary policy offsets, which has given a bigger role to feedback from past inflation. That said, inflation has been trending down for the past two decades across developed and developing economies alike. The inevitable conclusion is that there are global forces putting downward pressure on inflation, and it is not just the result of better monetary policy.”

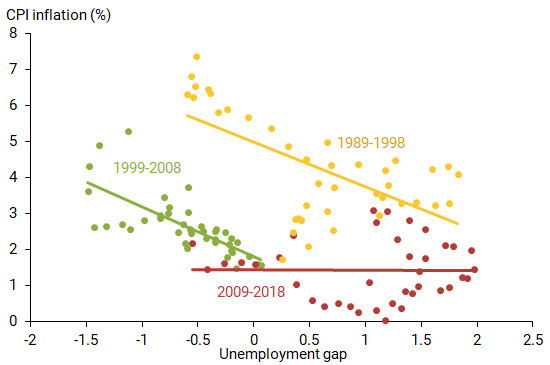

Figure 1

Phillips curve across OECD countries by decade

Continue reading here.

Posted by at 10:37 AM

Labels: Macro Demystified

Subscribe to: Posts