Friday, January 17, 2020

Finance and Inequality

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

At the same time, we observe rising or high disparities in income and wealth within many countries. New data also show that economic mobility—the ability of the less well-off to improve their economic status—has stalled in recent decades. No wonder then that inequality of income, wealth, and opportunities is giving rise to populism and anti-globalization sentiments in some countries.

Can the financial sector play a role in reducing inequality? This study makes the case that it can, complementing redistributive fiscal policy in mitigating inequality. By expanding the provision of financial services to low-income households and small businesses, it can serve as a powerful lever in helping create a more inclusive society but—if not well managed—it can also amplify inequalities.

Our study examines empirical relationships between income inequality and three features of finance: depth (financial sector size relative to the economy), inclusion (access to and use of financial services by individuals and firms), and stability (absence of financial distress). We ask three questions.

First, does greater financial depth mean lower or higher inequality within countries? Building on new data sets, our analysis suggests that initially financial depth is associated with lower inequality, but only up to a point, after which inequality rises.

Second, does greater financial inclusion mean lower inequality within countries? We find that greater financial inclusion is associated with reductions in inequality. For payment services, we find evidence that benefits from inclusion are greater for those at the low end of the income distribution, reducing inequality. Both men and women benefit from financial inclusion, but inequality falls more when women have greater access. As regards access to and use of credit, the results are mixed.

Third, is there a relationship between stability and inequality within countries? Our study finds that higher inequality is associated with greater financial risks. Increases in inequality tend to be accompanied by higher growth in credit. For example, in the United States, too much credit, including to lower-income households, contributed to the 2008 crisis. Crises, in turn, lead to higher default rates, making lower-income households worse off and increasing inequality after a crisis.

Our key takeaway is that finance can help reduce inequality but is also associated with greater inequality if the financial system is not well managed. Our findings have five policy implications. First, financial inclusion policies help reduce inequality. Second, there is a case for promoting women’s financial inclusion, as inequality falls even more when policies are inclusive of women. Third, regulatory policies have a role to play in reining in excessive growth of the financial sector. Fourth, provided quality of regulation and supervision is high, financial inclusion and stability can be pursued simultaneously. Fifth, financial sector policies are a complement, not a substitute, for other policy tools—fiscal and macro-structural policies are still needed to help address inequality.”

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

Posted by at 10:58 AM

Labels: Inclusive Growth

Housing View – January 17, 2020

On cross-country:

- Home ownership is the West’s biggest economic-policy mistake – Its obsession with home ownership undermines growth, fairness and public faith in capitalism – The Economist

- Housing is at the root of many of the rich world’s problems – Since the second world war, governments across the rich world have made three big mistakes, says Callum Williams – The Economist

- How housing became the world’s biggest asset class – It is only a recent phenomenon – The Economist

- Politicians are finally doing something about housing shortages. But will it reduce housing costs? – The Economist

- A decade on from the housing crash, new risks are emerging. Shadow banks originate around half America’s mortgages – The Economist

- Owner-occupation is not always a better deal than renting. Each year American owner-occupiers pay around $200bn in maintenance costs on their homes – The Economist

- Home ownership is in decline. That is not a big cause for concern – The Economist

- Governments are rethinking the provision of public housing. Is it better to give people money or build them houses? – The Economist

- What is the future of the rich world’s housing markets? It is plausible that house prices could persistently rise faster than incomes – The Economist

- Global Residential Cities Index – Q3 2019 – Knight Frank

- Around the world, luxury housing is poised to (mostly) strengthen – Los Angeles Times

On the US:

- Capital Income Taxation with Housing – Federal Reserve Bank of Philadelphia

- Affordable housing is in crisis. Is public housing the solution? – Curbed

- What Would It Take to End Homelessness? – Los Angeles Times

- Would Capping Office Space Ease San Francisco’s Housing Crunch? – Citylab

- A Perverse Way To “Solve” California’s Housing Crisis: People Are Leaving The Golden State – Hoover Institution

On other countries:

- [Hong Kong] Hong Kong’s house prices falling – Global Property Guide

- [Indonesia] The housing market in Indonesia rarely makes big moves – Global Property Guide

- [Ireland] Cash offers may lead mortgage customers to make poor decisions – ESRI – The Irish Times

- [Macau] Macau’s housing market slowing sharply – Global Property Guide

- [Netherlands] Amsterdam’s Attempt to Rein In Property Prices Just Got Harder – Bloomberg

- [South Korea] South Korea’s Moon Vows ‘Endless’ Measures to Cap Property Prices – Bloomberg

- [Switzerland] House prices in Switzerland continue to drop – Global Property Guide

- [United Kingdom] Cambridge tech boom blamed for rising property prices – Financial Times

On cross-country:

- Home ownership is the West’s biggest economic-policy mistake – Its obsession with home ownership undermines growth, fairness and public faith in capitalism – The Economist

- Housing is at the root of many of the rich world’s problems – Since the second world war, governments across the rich world have made three big mistakes, says Callum Williams – The Economist

- How housing became the world’s biggest asset class –

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 16, 2020

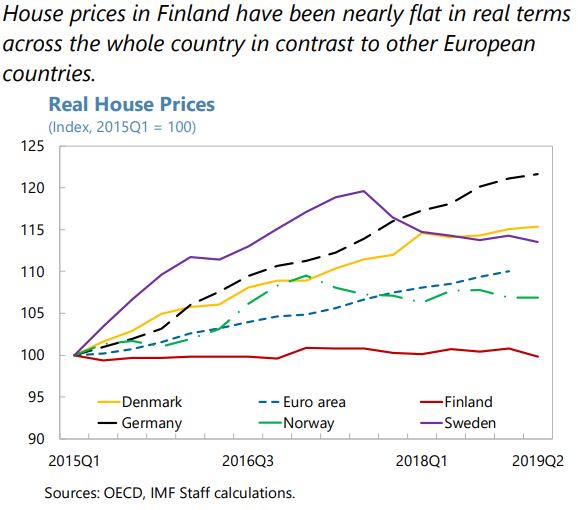

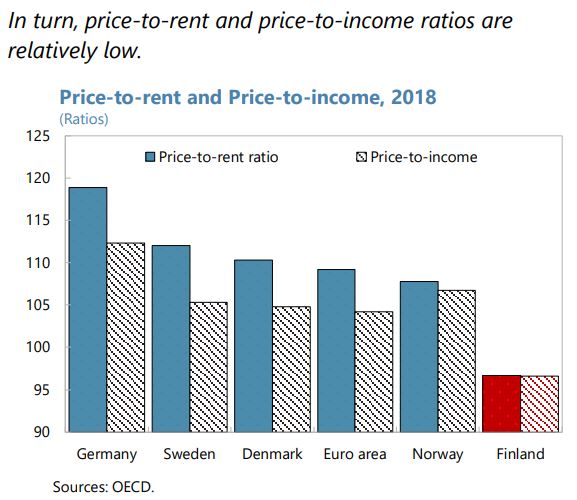

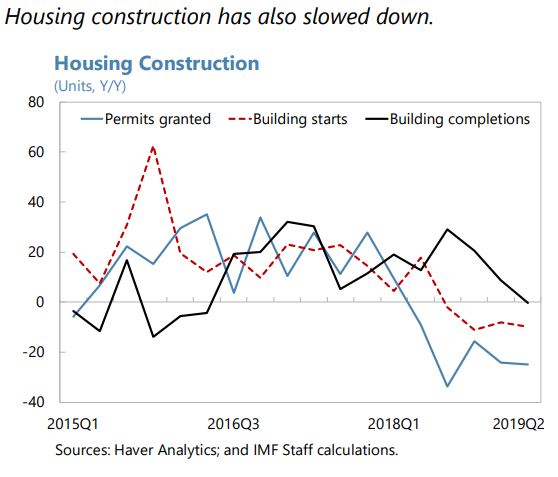

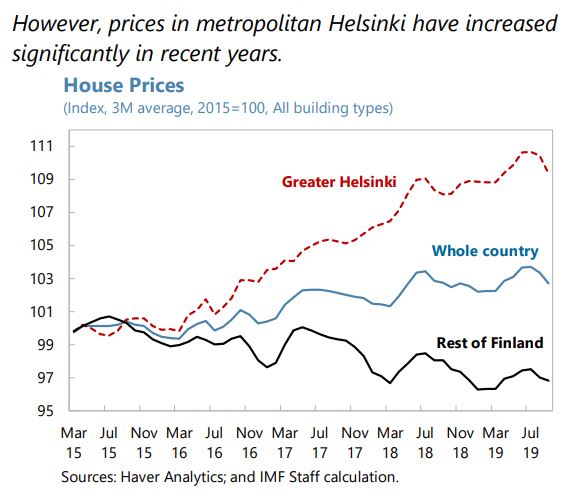

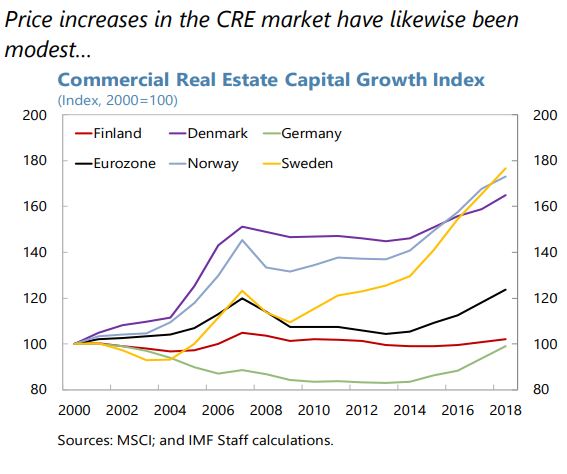

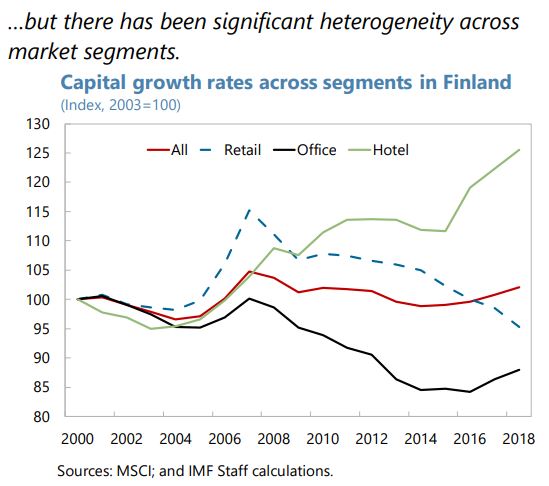

House prices in Finland

From the IMF’s latest report on Finland:

“Finnish banks are highly exposed to real estate, but residential and commercial real estate markets are not obviously overvalued. The exposure of domestic banks to real estate market has grown significantly over the last 20 years. The total volume of credit issued by domestic banks to the real-estate and construction sectors stood at 48.5 billion euros in 2018 (above 20 percent of GDP and 50 percent of banks’ receivables from firms and housing corporations), but rates of non-performing real estate loans remain low. In addition, real estate markets do not seem overheated overall, although there are differences across regions and market segments:

- Residential real estate prices have been nearly flat in real terms across the whole country, priceto-income and price-to-rent ratios are relatively low, and construction of new housing units seems to be slowing. However, housing prices in the Helsinki region have increased steadily while in most other parts of the country prices are falling (…).

- Commercial real estate (CRE) valuations also do not appear stretched overall, but aggregate price dynamics mask significant differences across regions and submarkets. In the prime Helsinki office segment, limited supply means that rents are increasing, but they remain below the levels observed in other European capitals. By contrast, prices of retail properties have declined, given the brisk pace of growth in e-commerce and new supply in the Helsinki area. There are ongoing efforts to collect more data for a more precise assessment of CRE-related vulnerabilities in the financial sector, but data to monitor developments in CRE markets remain insufficient.

However, the increase and the composition of household debt create borrower-side vulnerabilities. While the debt-to-income ratio remains far below that of Denmark, Norway and Sweden, it has increased in recent years, driven by large annual increases in consumer credit and housing company loans. The share of highly indebted households is also elevated relative to levels observed in the past (although it has been stable in recent years). One concern is that financing the purchase of real estate through shares in a housing company masks risks to home owners and can make higher prices appear more affordable than they truly are.10 In addition, the majority of housing loans carry variable rates.

The authorities are taking steps to address these weaknesses. In particular, a government appointed working group has recommended a comprehensive cap on the debt-toincome (DTI) ratio, limits on the indebtedness of housing companies, and shortening the maximum maturity of mortgages and housing company loans. Crucially, the DTI limit would cover all borrower’s debts, including housing company loans. The working group proposes that the DTI limit be 450 percent; anticipating cases in which higher leverage could be affordable for some borrowers, it also proposes an exemption to allow banks a share of borrowers with higher debt ratios. These would be significant improvements and also in line with recent recommendations by the European Systemic Risk Board. The parliamentary discussions on these proposals are set to begin in 2020. In addition to the working group recommendations, an electronic registry of housing company shares is scheduled to be operational by the end of 2022. The registry will include full ownership information and will therefore make it easier to assess risks of investing in housing companies.”

From the IMF’s latest report on Finland:

“Finnish banks are highly exposed to real estate, but residential and commercial real estate markets are not obviously overvalued. The exposure of domestic banks to real estate market has grown significantly over the last 20 years. The total volume of credit issued by domestic banks to the real-estate and construction sectors stood at 48.5 billion euros in 2018 (above 20 percent of GDP and 50 percent of banks’ receivables from firms and housing corporations),

Posted by at 9:44 AM

Labels: Global Housing Watch

Wednesday, January 15, 2020

Central Banks and Climate Change

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies. However, the central bank should retain absolute discretion to interrupt any action if its first-priority objective – price stability – were to be compromised.”

“The big question, however, is whether central banks can use their monetary instruments to actively promote the fight against climate change (Honohan 2019). Over the last decade, central banks have significantly expanded their balance sheets, often by a factor of five or ten. In many countries, those balance sheets are now commensurate to the size of the national economy. With such an imprint on the economy and financial markets, central banks could take a more proactive approach to financing the climate transition.

Two possibilities come to mind, both without significant changes to the current operational framework:

- Reorient their asset purchases towards ‘green’ securities

- Modulate haircuts applied to different kinds of collateral used in refinancing operations, thus creating an incentive to detain some and offload others. “

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies.

Posted by at 1:25 PM

Labels: Energy & Climate Change

Tuesday, January 14, 2020

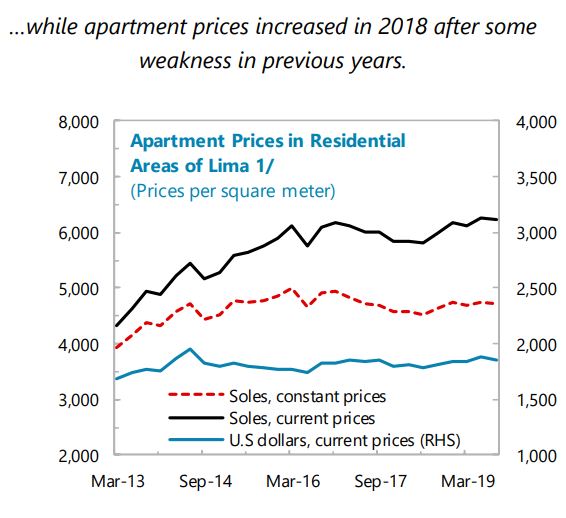

House Prices in Peru

From the IMF’s latest report on Peru:

Posted by at 1:48 PM

Labels: Global Housing Watch

Subscribe to: Posts