Thursday, January 23, 2020

As California comes to grips with housing crisis, Texas real estate rises in 2020

From Curbed:

“Housing availability and affordability will help determine these states’ trajectories this year

Texas and California represent opposite poles on the spectrum of government ideology—the Golden State’s Democratic supermajority versus the conservative Lone Star State’s regulation-averse independent streak—and in recent years, starkly different results when it comes to housing policy and production.

Predictions for this coming year highlight the divide. According to the recently released Texas A&M Real Estate Center’s outlook for 2020, the state’s homebuilding industry will still have a banner year, despite forecasts for muted economic growth.

“Both the Texas and U.S. economy will likely slow in 2020 yet still register solid growth,” says Real Estate Center research economist Luis Torres. “With uncertainty around trade wars and the current crude oil trajectory, two of the strongest economic drivers for Texas will decrease economic momentum. In contrast, one of the star performers of the 2020 economy will be the housing market, with double-digit growth in new home construction for the first time since 2017.”

California flips that idea on its head. Instead of attracting residents with a surfeit of new housing options despite low growth, it’s posting job growth above the national average, even beating the economies of many European nations when it comes to growth and performance metrics, yet still pushing away many residents—making it harder for lower- and middle-income residents to stay—as a result of soaring housing prices and continued difficulty building new supply.”

Continue reading here.

From Curbed:

“Housing availability and affordability will help determine these states’ trajectories this year

Texas and California represent opposite poles on the spectrum of government ideology—the Golden State’s Democratic supermajority versus the conservative Lone Star State’s regulation-averse independent streak—and in recent years, starkly different results when it comes to housing policy and production.

Predictions for this coming year highlight the divide. According to the recently released Texas A&M Real Estate Center’s outlook for 2020,

Posted by at 9:53 AM

Labels: Global Housing Watch

Wednesday, January 22, 2020

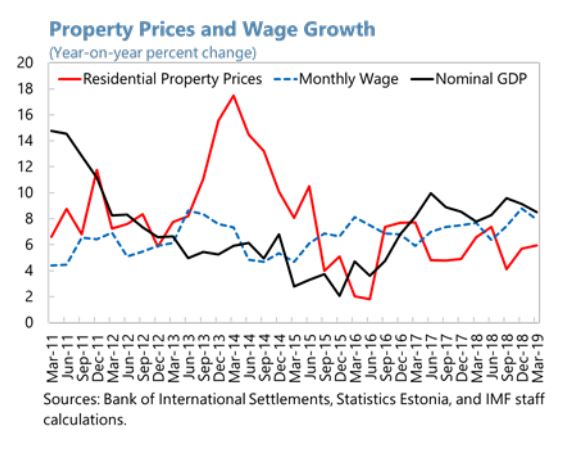

House prices in Estonia

From the IMF’s latest report on Estonia:

“Real estate market activity has moderated, and prices remained anchored to incomes. Transactions in the housing market slowed by 1.6 percent (y/y) in 2018, compared to an increase of 8.2 percent the previous year. House prices increased by 5.7 percent in 2018, driven by the rising share of new houses (…). Furthermore, the ratio of total liabilities to gross wages and salaries declined further from 114 percent in 2017 to 109 percent last year, suggesting a continued reduction in household leverage. Overall price trends remain strong, but aligned to income growth. During 2019H1, there were similar transactions overall compared to 2018H1, but fewer transactions for new apartments. The average price increased by 5.9 percent as new dwellings are being added at a slower pace.”

From the IMF’s latest report on Estonia:

“Real estate market activity has moderated, and prices remained anchored to incomes. Transactions in the housing market slowed by 1.6 percent (y/y) in 2018, compared to an increase of 8.2 percent the previous year. House prices increased by 5.7 percent in 2018, driven by the rising share of new houses (…). Furthermore, the ratio of total liabilities to gross wages and salaries declined further from 114 percent in 2017 to 109 percent last year,

Posted by at 9:57 AM

Labels: Global Housing Watch

Tuesday, January 21, 2020

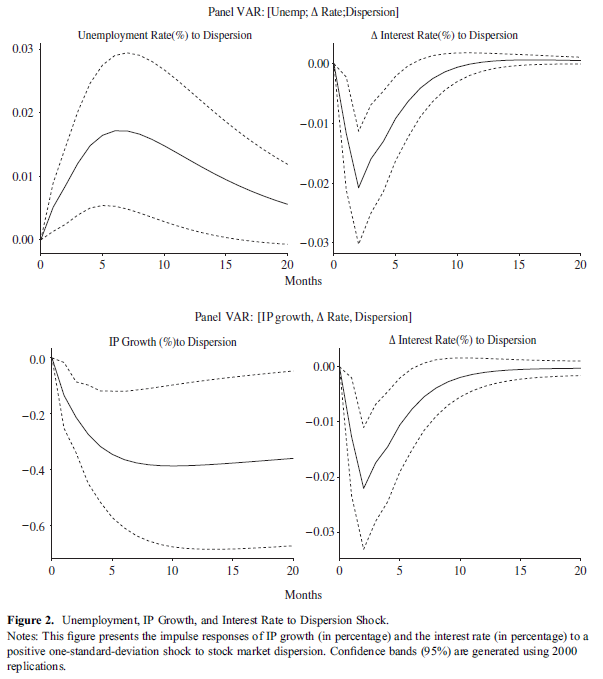

International Effects of Stock Market Dispersion

From a new paper on the effects of stock market dispersion:

“We study the extent to which stock market dispersion is related to unemployment and output growth for 16 countries over 20 years. Using panel vector-auto-regressions and panel dynamic regressions, we find increases in stock market dispersion across industries to induce future increases in unemployment and

future decreases in industrial production (IP) growth. Moreover, the responses of unemployment and IP growth following a positive shock to stock market dispersion are persistent and are robust to various controls, sample periods, and estimation methods. Our article provides cross-country evidence in support of the hypothesis that shifts in demand across industries negatively affect employment.”

“We present the impulse responses of the unemployment rate and the change in the interest rate to a positive one-standard-deviation shock to stock market dispersion in the upper subfigure of Figure 2. […] Overall, we find an increase in stock market dispersion to have a negative impact on the labor market in the short term, as evidenced by the positive response of the unemployment rate. Specifically, the unemployment rate increases by 0.02% following a positive one-standard-deviation shock to stock market dispersion. This increase peaks after the seventh month and gradually fades away after 15–20 months. Despite its modest magnitude at peak (0.02%), the impact of stock market dispersion on the unemployment rate is relatively long-lived, with the responses lasting beyond the 20-month horizon. Our result is consistent with previous studies that use U.S. data (e.g., Loungani, Rush, and Tave 1990, and more recently Angelidis, Sakkas, and Tessaromatis 2015) in the sense that unemployment significantly depends on the lags of stock market dispersion.”

From a new paper on the effects of stock market dispersion:

“We study the extent to which stock market dispersion is related to unemployment and output growth for 16 countries over 20 years. Using panel vector-auto-regressions and panel dynamic regressions, we find increases in stock market dispersion across industries to induce future increases in unemployment and

future decreases in industrial production (IP) growth. Moreover, the responses of unemployment and IP growth following a positive shock to stock market dispersion are persistent and are robust to various controls,

Posted by at 10:00 AM

Labels: Inclusive Growth

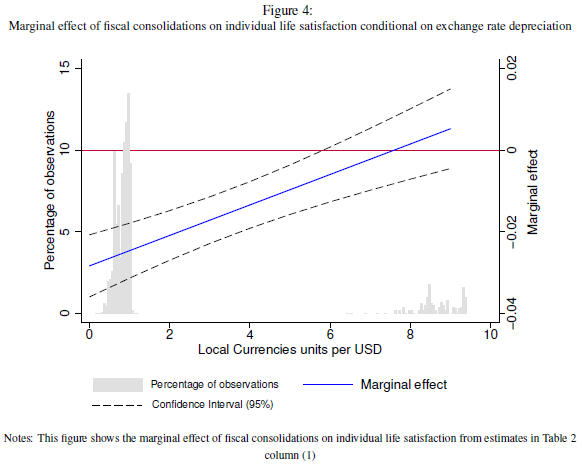

The (Subjective) Well-Being Cost of Fiscal Policy Shocks

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition, we show that accompanying monetary and exchange rate policies (disinflation, depreciations and the liberalization of capital flows) mitigate the well-being cost of fiscal consolidations. Finally, we investigate the well-being consequences of the two well-knowns expansionary fiscal consolidations episodes taking place in the 80s (in Denmark and Ireland). We find that even expansionary fiscal consolidations can have well-being costs. Our results may therefore shed some light on why some governments may choose to consolidate through taxes even at the cost of economic growth. Indeed, if spending cuts are to generate a large well-being loss, they can trigger an opposition and protest against a fiscal consolidation plan and hence making it politically costly.”

“Figure 4 depicts the effect of a 1 percentage point of GDP increase in the size of a fiscal consolidation conditional on being accompanied by different level of depreciation in the sample. Figure 4 shows that for higher levels of depreciation, that is for ratios of at least 6 units of local currencies per USD, fiscal consolidations do not have any statistically significant effect on well-being.”

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition,

Posted by at 9:55 AM

Labels: Inclusive Growth

Friday, January 17, 2020

Predicting Downside Risks to House Prices and Macro-Financial Stability

From an IMF working paper by Andrea Deghi, Mitsuru Katagiri, Sohaib Shahid, and Nico Valckx:

“This paper predicts downside risks to future real house price growth (house-prices-at-risk or HaR) in 32 advanced and emerging market economies. Through a macro-model and predictive quantile regressions, we show that current house price overvaluation, excessive credit growth, and tighter financial conditions jointly forecast higher house-prices-at-risk up to three years ahead. House-prices-at-risk help predict future growth at-risk and financial crises. We also investigate and propose policy solutions for preventing the identified risks. We find that overall, a tightening of macroprudential policy is the most effective at curbing downside risks to house prices, whereas a loosening of conventional monetary policy reduces downside risks only in advanced economies and only in the short-term.”

From an IMF working paper by Andrea Deghi, Mitsuru Katagiri, Sohaib Shahid, and Nico Valckx:

“This paper predicts downside risks to future real house price growth (house-prices-at-risk or HaR) in 32 advanced and emerging market economies. Through a macro-model and predictive quantile regressions, we show that current house price overvaluation, excessive credit growth, and tighter financial conditions jointly forecast higher house-prices-at-risk up to three years ahead. House-prices-at-risk help predict future growth at-risk and financial crises.

Posted by at 5:37 PM

Labels: Global Housing Watch

Subscribe to: Posts