“Nevertheless, challenges are building. Nearly half of legacy NPLs were terminated five years earlier, potentially requiring sizable write-downs (Annex VI). Foreclosures have been suspended until end-July for smaller, collateralized loans and proposals under discussion in Parliament are expected to weaken the framework (¶22, third bullet). More than 80 percent of bank loans are to highly leveraged households and SMEs, concentrated in sectors like accommodation, food and retail, implying a high risk of an escalation of default rates and lower recovery value of assets after the expiry of loan repayment and foreclosure moratorium (Box 1). Banks are also exposed to property market risks through real estate holdings and collateral valuation. Although regulatory forbearance and fiscal support have prevented an immediate surge in loan impairments, a new wave of defaults as loan repayment obligations resume amidst tapering fiscal support could quickly consume the capital buffers of banks. Based on a stylized scenario with a 10 percent increase10 in NPLs that would push the latter to some 19.5 percent of total loans from the current 17.7 percent, staff estimates that restoring capital and provisions to pre-pandemic levels would entail capital needs of 1.5 percent of GDP.

(…)

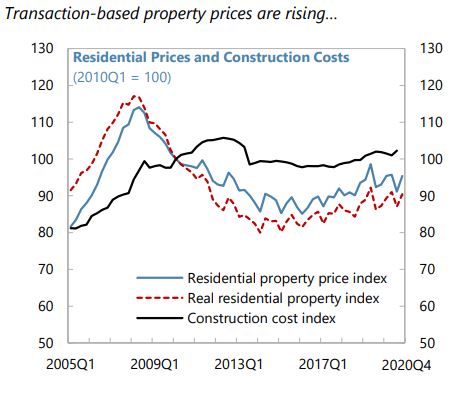

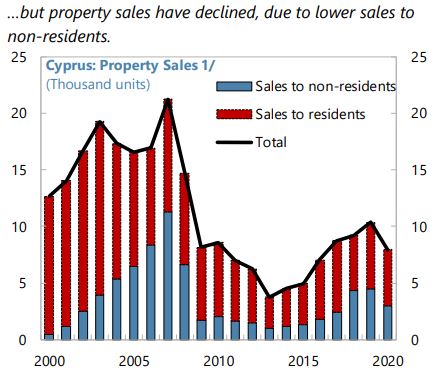

Macro-financial risks from possible declines in property prices should be closely monitored, especially given the continued active use of debt-to-asset swaps in NPL resolution by banks and CACs. Risks appear limited for now given stable residential price developments (Text Figure 5 and Figure 8) and limited size of commercial real estate transactions. To ensure proper collateral valuation, results of actual sales transactions of repossessed collateral properties should be used by banks and CACs to review adequacy of valuation methodologies of these assets. Supervisory guidance to prevent excessive holding of repossessed collateral assets by banks should be maintained.”

“Nevertheless, challenges are building. Nearly half of legacy NPLs were terminated five years earlier, potentially requiring sizable write-downs (Annex VI). Foreclosures have been suspended until end-July for smaller, collateralized loans and proposals under discussion in Parliament are expected to weaken the framework (¶22, third bullet). More than 80 percent of bank loans are to highly leveraged households and SMEs, concentrated in sectors like accommodation,

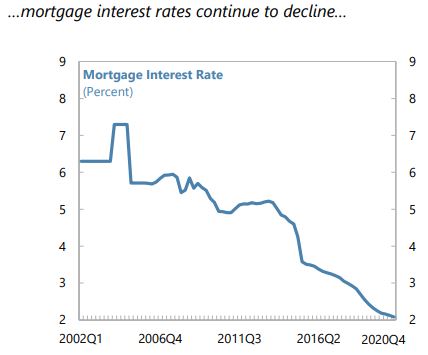

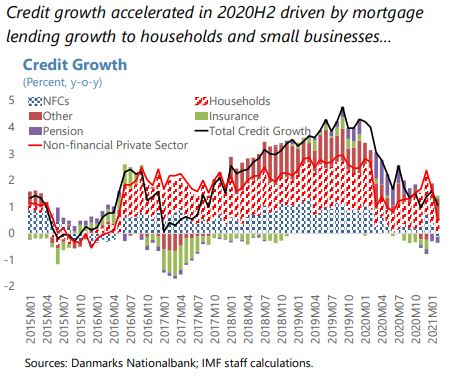

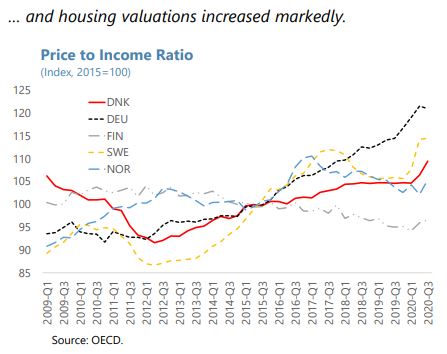

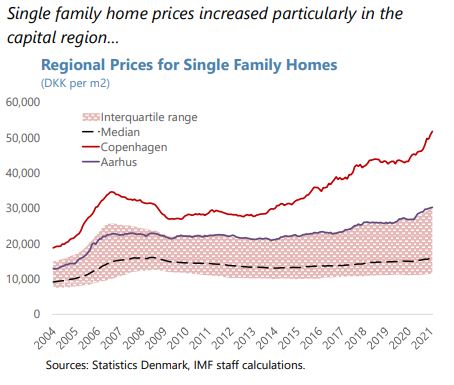

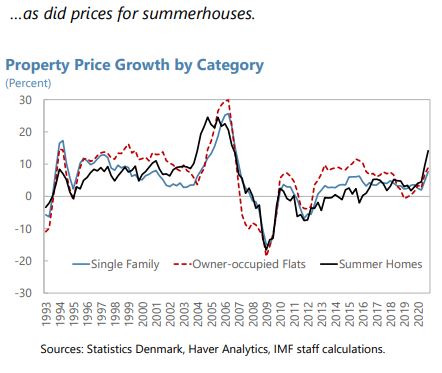

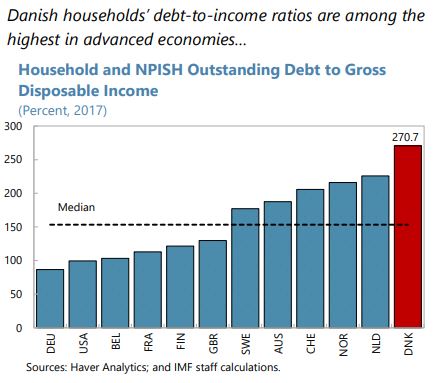

“Credit to households and house price growth accelerated during the pandemic. Before the pandemic, household leverage was high. Credit growth stalled at the onset of the pandemic but strongly recovered in 2020H2, driven primarily by mortgage lending. Residential property prices rose sharply in 2020H2, particularly for summer-houses, likely partially influenced by a temporary increase in tax deductions for summerhouse owners (…).

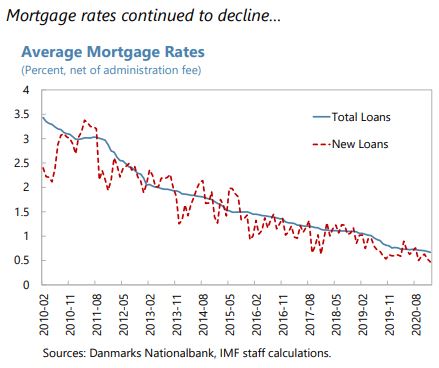

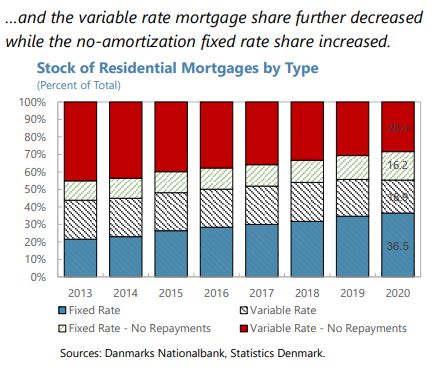

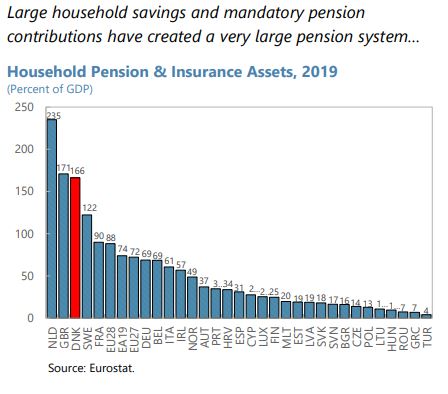

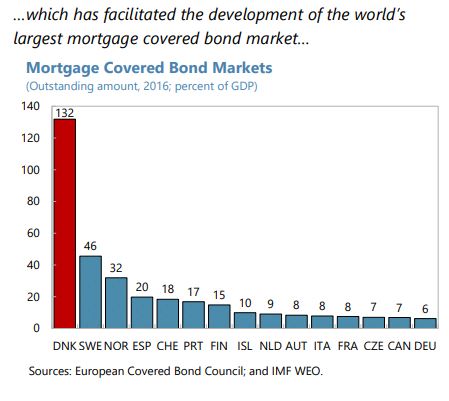

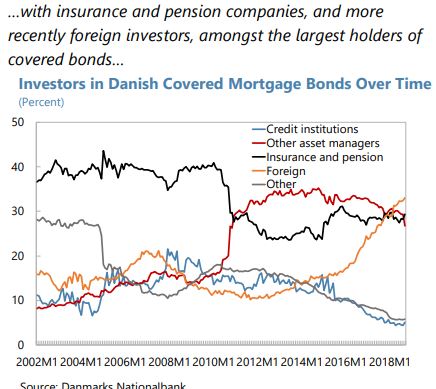

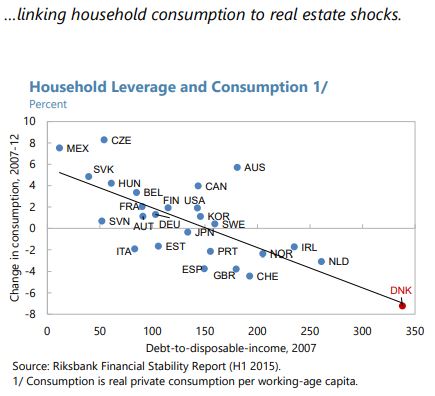

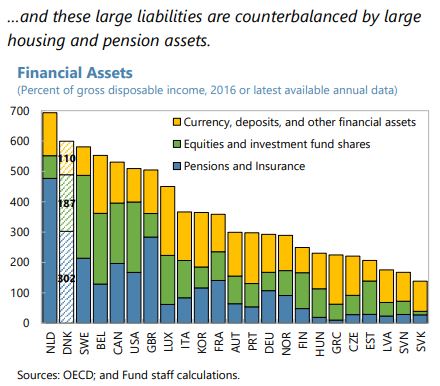

Macrofinancial vulnerabilities due to high and increasing household leverage amid high house valuations warrant close monitoring. High debt, combined with illiquid assets (concentrated in real estate via housing and pension assets) exposes households to price and interest rate shocks that can impact their balance sheet asymmetrically and spillover to aggregate demand. Continued strong house price growth increases the likelihood of a revaluation that could harm highly-leveraged households, particularly those who purchased in overvalued urban areas and low-income households. These vulnerabilities are compounded by the still large proportion of variable-rate and interest-only mortgages in the system (…). Moreover, MCIs and pension and insurance companies are highly interconnected and dependent on the health of the housing sector.

Recent developments warrant tightening prudential tools while deploying coordinated tax and housing supply policies.

–Macroprudential policy. The authorities should shift focus toward income-based measures, including tightening debt-to-income (DTI), LTI, and debt-service-to-income caps would help address high leverage and encourage faster amortization, as loan-to-value (LTV) constraints are less binding in the current environment with high house price growth. The authorities should tighten DTI restrictions for all loans, irrespective of their LTV ratios. DTI caps could be differentiated based on borrowers’ riskiness. Highly-leveraged households should be subject to mandatory amortization, regardless of maturity- and rate-type (SIP 2018). Tighter limits on income-based measures for interest-only and floating-rate mortgages or higher minimum down-payment requirements should also be considered. The proposed risk-based prudential framework could be combined with the macroprudential setup to facilitate calibration of these measures, especially for lower risk groups, e.g., first-time home buyers.

–Tax policy. The tax treatment of owner-occupied housing remains favorable relative to other savings and compared to most OECD countries. Taking advantage of the current low rate environment, MID should be reduced in a manner consistent with the overall tax framework.48 Staff recommend prioritizing reforms to better link property taxes to current market valuations. Balancing tax incentives for pension contributions could release resources for larger down-payments.

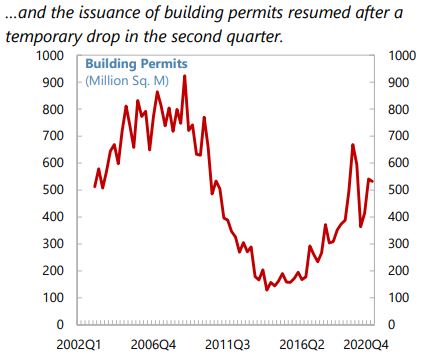

–Housing supply. Rent controls in Denmark are high relative to peer countries and should be reduced to stimulate the rental market, while protecting the interests of the most vulnerable. Review of urban area restrictions on the size of new apartments should continue to improve demand-supply mismatches. Streamlined zoning and planning procedures across municipalities could increase supply, thereby alleviating price pressures.”

“Credit to households and house price growth accelerated during the pandemic. Before the pandemic, household leverage was high. Credit growth stalled at the onset of the pandemic but strongly recovered in 2020H2, driven primarily by mortgage lending. Residential property prices rose sharply in 2020H2, particularly for summer-houses, likely partially influenced by a temporary increase in tax deductions for summerhouse owners (…).

Macrofinancial vulnerabilities due to high and increasing household leverage amid high house valuations warrant close monitoring.

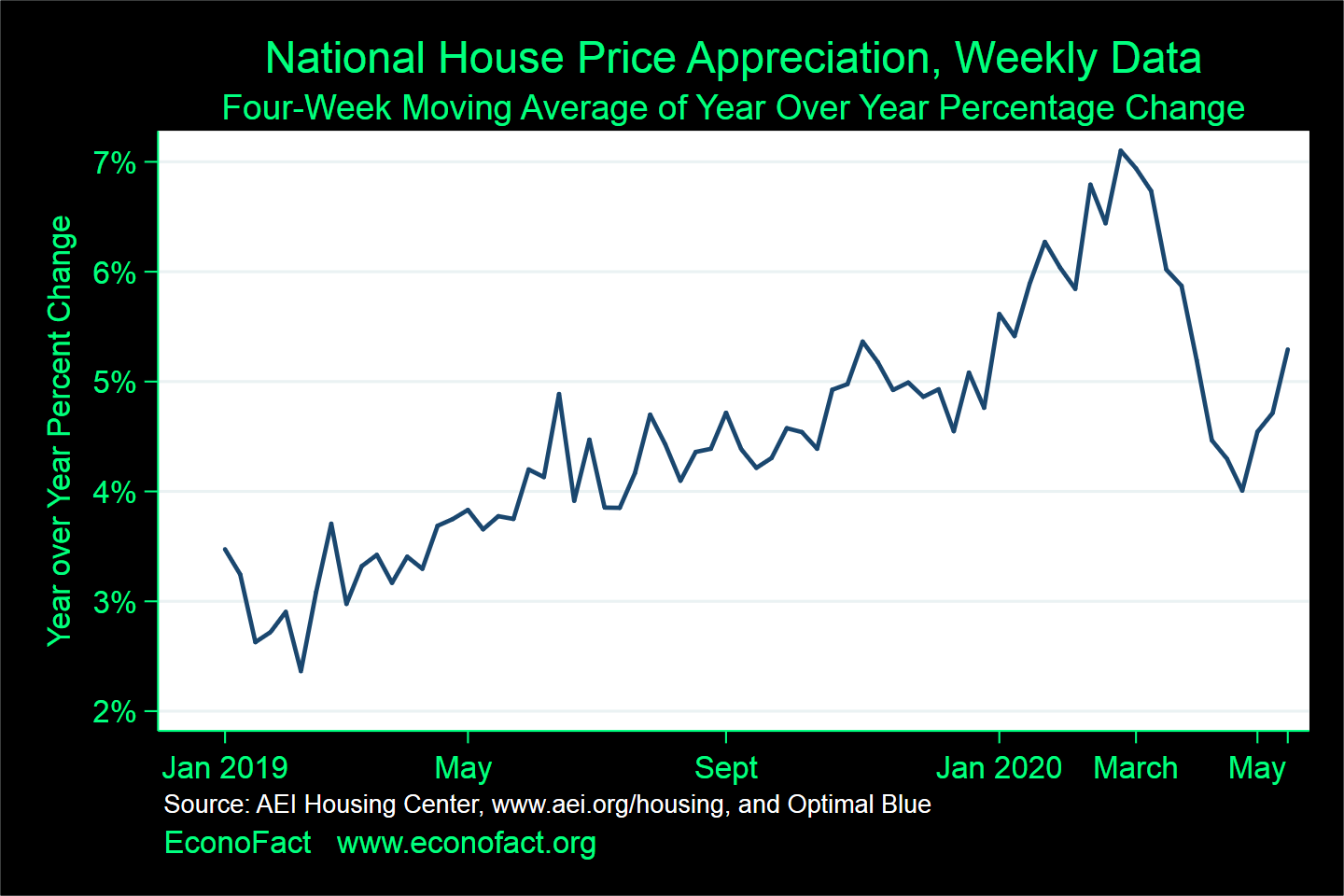

“From EconoFact: The perception of falling prices of single-family homes and record levels of unemployment raise the specter of rising levels of mortgage defaults. Mortgage defaults in the wake of the economic and financial collapse in the Fall of 2008 contributed to the tepid economic recovery from that crisis, as well as personal hardship for those who lost their houses; by 2010, approximately 11.5 percent of single-family residential mortgages were delinquent and more than 2 percent were in foreclosure. There are concerns that similar developments now could derail economic recovery. But drawing parallels between 2020 and 2008 is problematic because conditions differ substantially across the two periods in the run-up to the crisis and in its first few months.” See full brief by Jeff Zabel.

“From EconoFact: The perception of falling prices of single-family homes and record levels of unemployment raise the specter of rising levels of mortgage defaults. Mortgage defaults in the wake of the economic and financial collapse in the Fall of 2008 contributed to the tepid economic recovery from that crisis, as well as personal hardship for those who lost their houses; by 2010, approximately 11.5 percent of single-family residential mortgages were delinquent and more than 2 percent were in foreclosure.

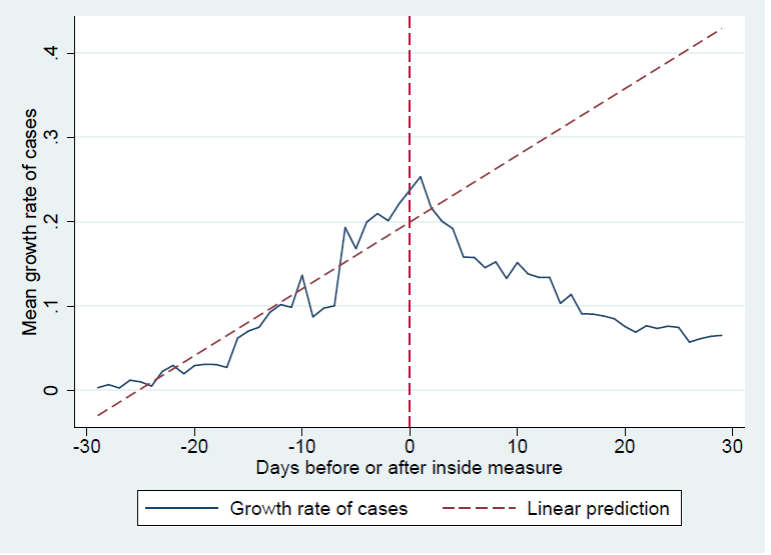

“Reducing movements within countries has been effective in developed economies – averting about 650,000 deaths – but not in developing ones,” according to new research. “Countries that acted fast fared better” and “closing borders has had no appreciable effect, even after 50 days.” The authors studied “various types of lockdowns implemented around the world mitigated the surge in infections and reduced mortality related to the Covid-19, and whether their effectiveness differed in developing versus developed countries.” Their data cover 184 countries from December 31st 2019 to May 4th 2020, and identifies when lockdowns were adopted, along with confirmed cases and deaths. Link to paper: fast and local.

“Reducing movements within countries has been effective in developed economies – averting about 650,000 deaths – but not in developing ones,” according to new research. “Countries that acted fast fared better” and “closing borders has had no appreciable effect, even after 50 days.” The authors studied “various types of lockdowns implemented around the world mitigated the surge in infections and reduced mortality related to the Covid-19, and whether their effectiveness differed in developing versus developed countries.”