Tuesday, June 15, 2021

Housing Market in Denmark

From the IMF’s latest report on Denmark:

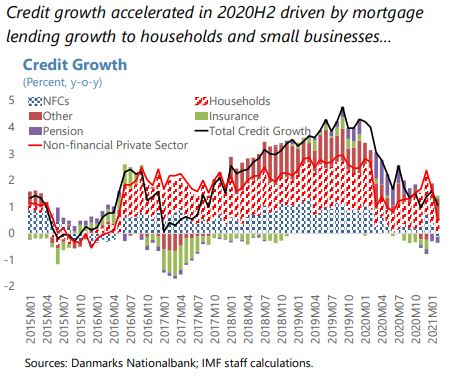

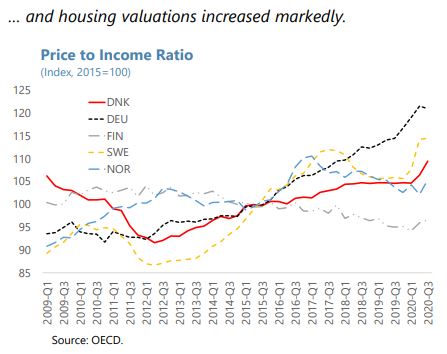

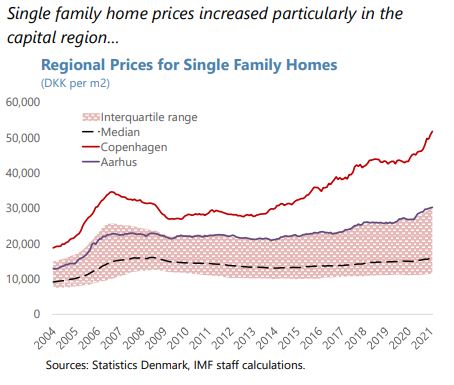

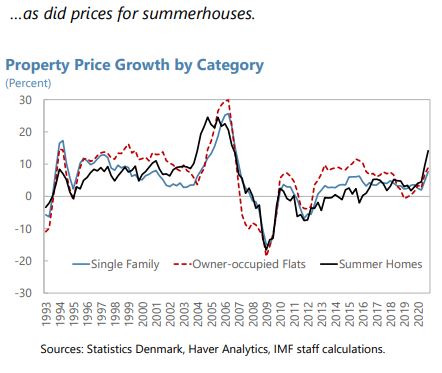

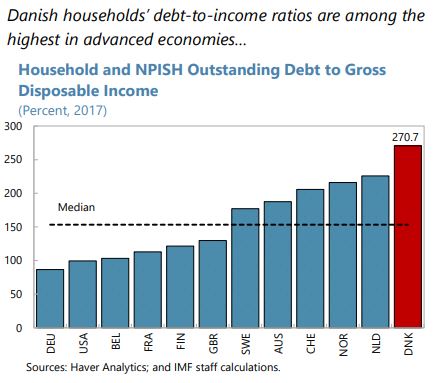

“Credit to households and house price growth accelerated during the pandemic. Before the pandemic, household leverage was high. Credit growth stalled at the onset of the pandemic but strongly recovered in 2020H2, driven primarily by mortgage lending. Residential property prices rose sharply in 2020H2, particularly for summer-houses, likely partially influenced by a temporary increase in tax deductions for summerhouse owners (…).

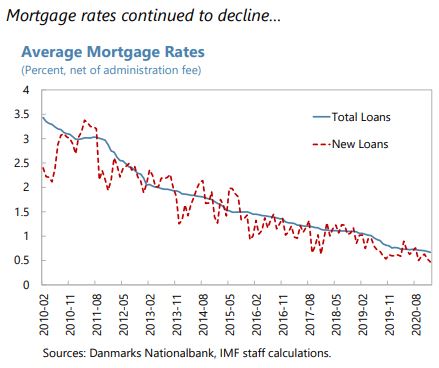

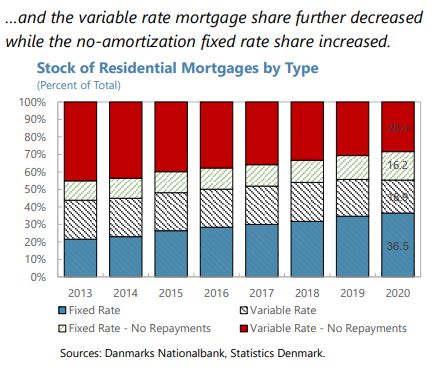

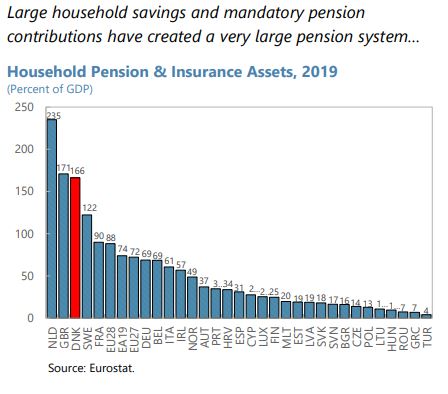

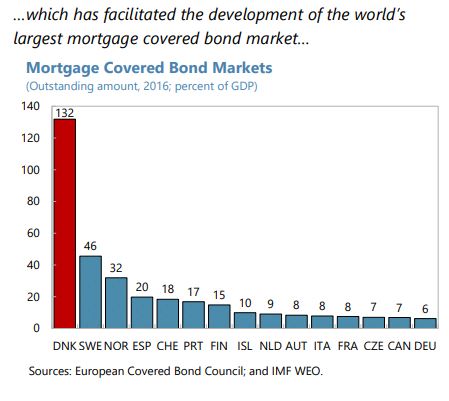

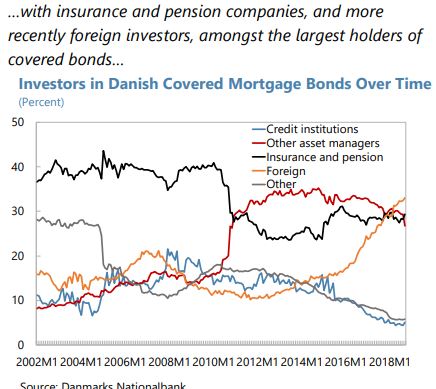

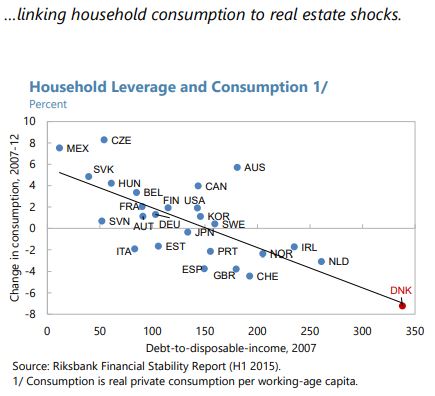

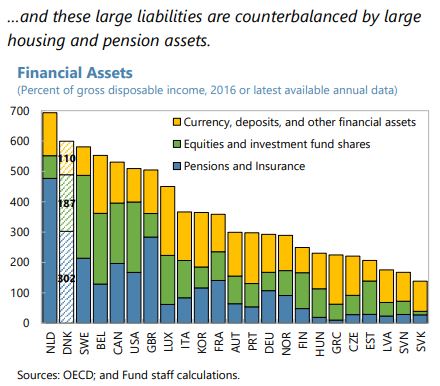

Macrofinancial vulnerabilities due to high and increasing household leverage amid high house valuations warrant close monitoring. High debt, combined with illiquid assets (concentrated in real estate via housing and pension assets) exposes households to price and interest rate shocks that can impact their balance sheet asymmetrically and spillover to aggregate demand. Continued strong house price growth increases the likelihood of a revaluation that could harm highly-leveraged households, particularly those who purchased in overvalued urban areas and low-income households. These vulnerabilities are compounded by the still large proportion of variable-rate and interest-only mortgages in the system (…). Moreover, MCIs and pension and insurance companies are highly interconnected and dependent on the health of the housing sector.

Recent developments warrant tightening prudential tools while deploying coordinated tax and housing supply policies.

–Macroprudential policy. The authorities should shift focus toward income-based measures, including tightening debt-to-income (DTI), LTI, and debt-service-to-income caps would help address high leverage and encourage faster amortization, as loan-to-value (LTV) constraints are less binding in the current environment with high house price growth. The authorities should tighten DTI restrictions for all loans, irrespective of their LTV ratios. DTI caps could be differentiated based on borrowers’ riskiness. Highly-leveraged households should be subject to mandatory amortization, regardless of maturity- and rate-type (SIP 2018). Tighter limits on income-based measures for interest-only and floating-rate mortgages or higher minimum down-payment requirements should also be considered. The proposed risk-based prudential framework could be combined with the macroprudential setup to facilitate calibration of these measures, especially for lower risk groups, e.g., first-time home buyers.

–Tax policy. The tax treatment of owner-occupied housing remains favorable relative to other savings and compared to most OECD countries. Taking advantage of the current low rate environment, MID should be reduced in a manner consistent with the overall tax framework.48 Staff recommend prioritizing reforms to better link property taxes to current market valuations. Balancing tax incentives for pension contributions could release resources for larger down-payments.

–Housing supply. Rent controls in Denmark are high relative to peer countries and should be reduced to stimulate the rental market, while protecting the interests of the most vulnerable. Review of urban area restrictions on the size of new apartments should continue to improve demand-supply mismatches. Streamlined zoning and planning procedures across municipalities could increase supply, thereby alleviating price pressures.”

Posted by at 4:05 PM

Labels: Global Housing Watch

Subscribe to: Posts