Sunday, January 16, 2022

The US Economy as 2022 Begins

From Conversable Economist:

“The Federal Reserve Bank of New York puts out a monthly publication called “U.S. Economy in a Snapshot,” a compilation of figures and short notes about the most recently available major macroeconomic statistics. As we take a deep breath and head into 2022, it seemed a useful time to consult pass along some these figures as as a way of showing the path of the US economy since the two-month pandemic recession of March and April 2020.

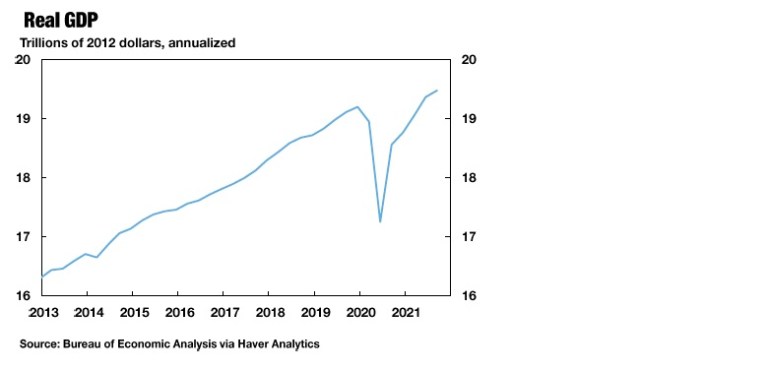

Here’s the path of GDP growth. It has clearly bounced back from the worse of the recession, but it still remains about 2% below the trend-line from before the recession occurred.

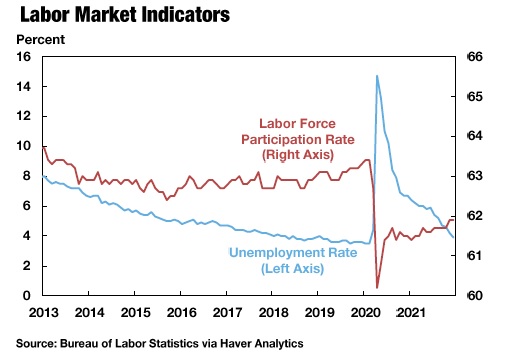

Part of the reason why GDP has not rebounded more fully lies in what is being called the “Great Resignation”–that is, people who left the workforce during the pandemic and have not returned. Just to be clear, to be counted as officially “unemployed” you need to be both out of a job and actively looking for a job. If you are out of a job but not looking, then you are “out of the labor force.” Thus, you can see that while the unemployment rate based on those out of a job and actively looking for work is back down to pre-pandemic levels, the labor force participation rate–which combines those who have job and the unemployed who are looking–has not fully rebounded. A smaller share of the labor force working will typically translate into a smaller GDP. When or if these potential workers return to the workforce will have a big effect on the future evolution of the economy and public policy.”

From Conversable Economist:

“The Federal Reserve Bank of New York puts out a monthly publication called “U.S. Economy in a Snapshot,” a compilation of figures and short notes about the most recently available major macroeconomic statistics. As we take a deep breath and head into 2022, it seemed a useful time to consult pass along some these figures as as a way of showing the path of the US economy since the two-month pandemic recession of March and April 2020.

Posted by at 8:03 AM

Labels: Macro Demystified

Saturday, January 15, 2022

The Inflation Outlook

As described by the tagline of this blog post, it dives deeper into CPI figures for the USA for December 2021 and then discusses their implications. CPI rose by 7 percent year on year in December and 0.5 percent since November 2021, although the rise in demand causing it wasn’t all uniform. The pattern of uneven growth of consumer expenditure on manufactured goods and durables rather than services has been discussed in greater detail, besides issues like inhouse oil production in the US which also exert some influence on the general price level.

Looking ahead, it elaborates upon visible signs that signal a quickly abating inflation using measures like wage growth, prevailing inflation expectations in the market, and the state of aggregate spending in the economy.

Click here to read the full blog.

As described by the tagline of this blog post, it dives deeper into CPI figures for the USA for December 2021 and then discusses their implications. CPI rose by 7 percent year on year in December and 0.5 percent since November 2021, although the rise in demand causing it wasn’t all uniform. The pattern of uneven growth of consumer expenditure on manufactured goods and durables rather than services has been discussed in greater detail, besides issues like inhouse oil production in the US which also exert some influence on the general price level.

Posted by at 9:08 AM

Labels: Macro Demystified

Nonprofits in Good Times and Bad Times

Source: NBER Working Paper (2022)

Abstract– “Need fluctuates over the business cycle. We conduct a survey revealing a desire for nonprofit activities to countercyclically expand during downturns. We then demonstrate, using comprehensive US nonprofit data drawn from millions of tax returns, that the public’s hopes are disappointed. Nonprofit expenditure, revenue, and balance sheets fluctuate procyclically: contracting during national and local downturns. This finding is evident even for a narrow group of nonprofits the public most wishes would expand during downturns, e.g., those providing critical needs like food or housing. Our new facts contribute to the charitable giving, nonprofit, and business cycle literatures (sic).”

Source: NBER Working Paper (2022)

Abstract– “Need fluctuates over the business cycle. We conduct a survey revealing a desire for nonprofit activities to countercyclically expand during downturns. We then demonstrate, using comprehensive US nonprofit data drawn from millions of tax returns, that the public’s hopes are disappointed. Nonprofit expenditure, revenue, and balance sheets fluctuate procyclically: contracting during national and local downturns. This finding is evident even for a narrow group of nonprofits the public most wishes would expand during downturns,

Posted by at 8:40 AM

Labels: Inclusive Growth

Friday, January 14, 2022

Do Exchange Rate Movements Equalize Yields?

Source: Econbrowser

“Fama (JME, 1984), and Tryon (1979) demonstrated that changes in the exchange rate do not equal the forward premium, in what came to be known as the forward premium puzzle. Since the forward premium equals the interest differential in the absence of current and incipient capital controls and in the absence of default risk — this finding is equivalent to the result that interest rates, after accounting for exchange rate changes, are not equalized on average. In other words, if the yield on the US default-risk-free bond is 2% and the yield on a UK default-risk-free bond is 5%, then the US dollar does not on an average appreciate by 3% against the pound in order to equalize returns.“

While this puzzle has largely persisted for a long time, it disappeared during and after the global financial crisis, until reappearing recently. In this blog, the authors have propounded explanations for the same. Read on to know more.

Source: Econbrowser

“Fama (JME, 1984), and Tryon (1979) demonstrated that changes in the exchange rate do not equal the forward premium, in what came to be known as the forward premium puzzle. Since the forward premium equals the interest differential in the absence of current and incipient capital controls and in the absence of default risk — this finding is equivalent to the result that interest rates, after accounting for exchange rate changes,

Posted by at 7:06 AM

Labels: Macro Demystified

How democracy causes growth: Evidence from Indonesia

Source: VoxDev

Authors of this article (2022), Baafra Abeberese, A. et al describe their study and its results as follows:

“We study how democratisation affects firm productivity — a critical micro-driver of economic growth. We do so in the context of Indonesia, which had been under the dictatorial rule of Soeharto for three decades, until the unexpected collapse of his regime in 1998. Using the exogenous timing of when each district in the country transitioned to a democracy, we estimate the causal effect of democratisation on firm productivity. We combine data on the timing of democratisation with an annual census of manufacturing firms over two decades to analyse the impact of democratisation on firms using an event study design. Our findings suggest that democratic leaders are less likely to impose socially inefficient regulations or engage in rent-seeking and, hence, enhance firm productivity.”

Related Reading

Revisiting the causal effect of democracy on long-run development

Source: VoxDev

Authors of this article (2022), Baafra Abeberese, A. et al describe their study and its results as follows:

“We study how democratisation affects firm productivity — a critical micro-driver of economic growth. We do so in the context of Indonesia, which had been under the dictatorial rule of Soeharto for three decades, until the unexpected collapse of his regime in 1998. Using the exogenous timing of when each district in the country transitioned to a democracy,

Posted by at 6:43 AM

Labels: Inclusive Growth

Subscribe to: Posts