Wednesday, February 2, 2022

Why, and Where, are Housing Prices Rising?

From Econofact:

“The Issue:

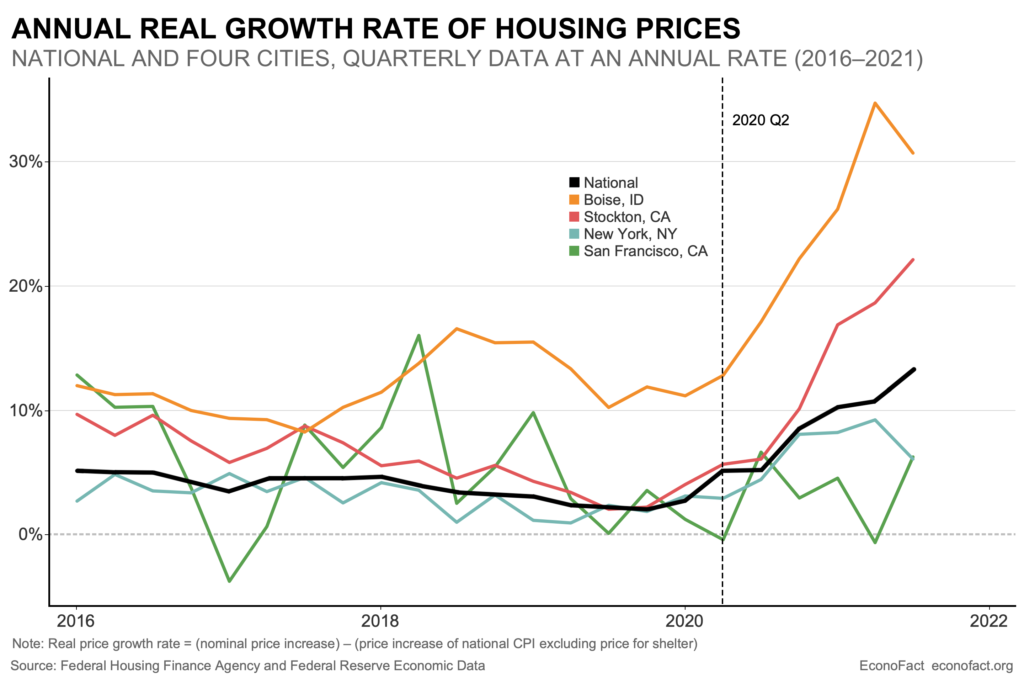

The price of housing has a special importance because housing is both a basic necessity and a key component of wealth. Around the start of the pandemic, some experts predicted a protracted collapse in housing prices and the housing market. For example, in April 2020 the staff at Freddie Mac projected home prices would fall by 0.5 percent over the next year. In fact, the opposite happened: The Case Shiller National Home Price Index rose by 15 percent between April 2020 and April 2021 while home sales hit a 15 year high in the calendar year 2021. This stands in stark contrast to the Great Recession when the price index fell 44 percent between May 2007 and May 2009. But one similarity across the Great Recession and the COVID downturn is the wide differences in housing price changes across different parts of the United States. What has happened to housing prices during the COVID pandemic and why? And what are the broader economic implications of this?

The Facts:

House sales and housing construction fell at the outset of the pandemic in March 2020. The total housing inventory on the market, including newly constructed houses and those being resold, was down 10.2 percent between March 2019 and March 2020. Between February 2020 and March 2020 housing starts declined by 22.3 percent, perhaps reflecting builders’ bleak expectations for future demand. Total existing-home sales fell 8.5 percent in March 2020 compared with the prior month and tumbled a further 17.8 percent in April.”

Continue reading here.

From Econofact:

“The Issue:

The price of housing has a special importance because housing is both a basic necessity and a key component of wealth. Around the start of the pandemic, some experts predicted a protracted collapse in housing prices and the housing market. For example, in April 2020 the staff at Freddie Mac projected home prices would fall by 0.5 percent over the next year.

Posted by at 2:03 PM

Labels: Global Housing Watch

Slowing Women’s Labor Force Participation: The Role of Income Inequality

Source: NBER Working Paper

Historically, the number and wages of women in the labor force grew at a significant pace during the 1970s and 1980s but began stalling in the early 1990s, especially for college graduates.

In this paper, the authors have argued that this discontinued growth since the 1990s is a consequence of growing inequality. They show that slowdown in participation and wage growth was concentrated among women married to highly educated and high-income husbands, whose earnings grew dramatically over the period under study. Through a model of household labor supply, they qualitatively analyze the above-mentioned effect and account for the rise in the gender wage gap for college graduates.

Source: NBER Working Paper

Historically, the number and wages of women in the labor force grew at a significant pace during the 1970s and 1980s but began stalling in the early 1990s, especially for college graduates.

In this paper, the authors have argued that this discontinued growth since the 1990s is a consequence of growing inequality. They show that slowdown in participation and wage growth was concentrated among women married to highly educated and high-income husbands,

Posted by at 7:39 AM

Labels: Inclusive Growth

Tuesday, February 1, 2022

The Slowdown in Agricultural Productivity Growth

Source: Conversable Economist

In this recent blog, author Timothy Taylor discusses the perplexing question of slowing agricultural growth witnessed in several countries across the world in the past couple of years. He first analyzes what percentage of influence on agricultural growth is exerted by rising overall economic productivity in the country, and discovers that it is mostly low-income countries where the decline has been most profound. The column also provides explanations for this trend that are worth exploring.

Source: Conversable Economist

In this recent blog, author Timothy Taylor discusses the perplexing question of slowing agricultural growth witnessed in several countries across the world in the past couple of years. He first analyzes what percentage of influence on agricultural growth is exerted by rising overall economic productivity in the country, and discovers that it is mostly low-income countries where the decline has been most profound. The column also provides explanations for this trend that are worth exploring.

Posted by at 12:38 PM

Labels: Inclusive Growth

Monday, January 31, 2022

Creative destruction during crises: An opportunity for a cleaner energy mix

Published on Voxeu.org by Pragyan Deb, Davide Furceri, Jonathan D. Ostry, Nour Tawk on 31 January 2022.

“Lockdowns resulting from the COVID-19 pandemic reduced overall energy demand in 2020. However, electricity generation from renewable sources was surprisingly resilient and, as a result, the share of renewables in electricity demand increased in many regions (International Energy Agency 2020). What remains an open question is whether recessions of themselves tend to spur investments in more efficient, greener, energy sources, or instead to continue investing in old coal-based plants. On one hand, the disruption in financing engendered by the crisis may reduce innovation through lower research and development, which is highly procyclical (De Haas et al. 2021). On the other, lower energy demand and associated plant closures brought about by the recession may provide energy producers with an opportunity to improve their efficiency by replacing older environmentally unfriendly plants with renewable sources of energy when demand recovers. The idea that outdated units are destroyed and replaced by newer technological innovations goes back to Joseph A. Schumpeter’s thesis on ‘creative destruction’ (Schumpeter 1939, 1942), with economic disruptions such as the one brought about by the pandemic acting as a time of cleansing (Caballero and Hammour 1994).”

Read more by clicking here.

Published on Voxeu.org by Pragyan Deb, Davide Furceri, Jonathan D. Ostry, Nour Tawk on 31 January 2022.

“Lockdowns resulting from the COVID-19 pandemic reduced overall energy demand in 2020. However, electricity generation from renewable sources was surprisingly resilient and, as a result, the share of renewables in electricity demand increased in many regions (International Energy Agency 2020). What remains an open question is whether recessions of themselves tend to spur investments in more efficient,

Posted by at 2:25 PM

Labels: Energy & Climate Change

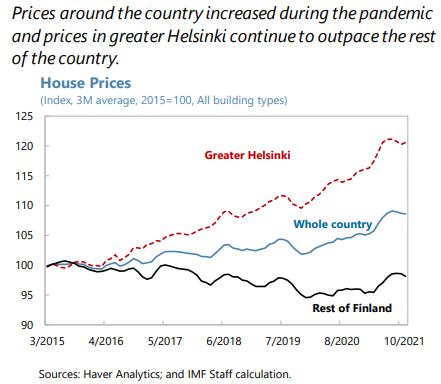

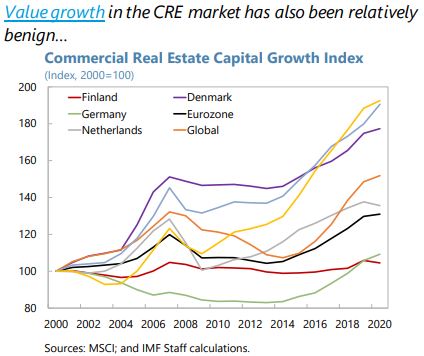

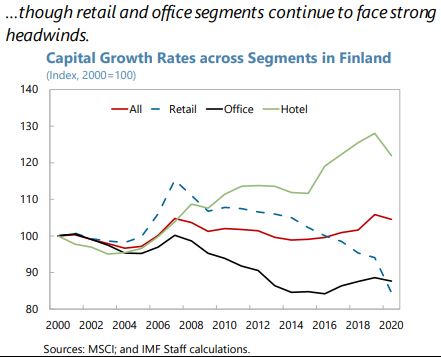

Housing Market in Finland

From the IMF’s latest report on Finland:

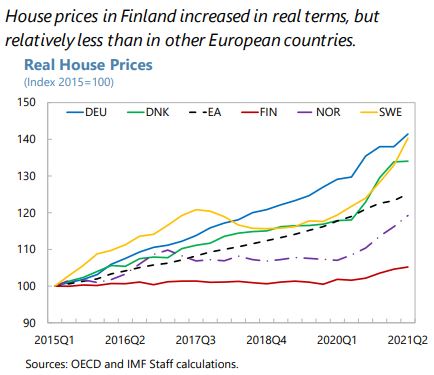

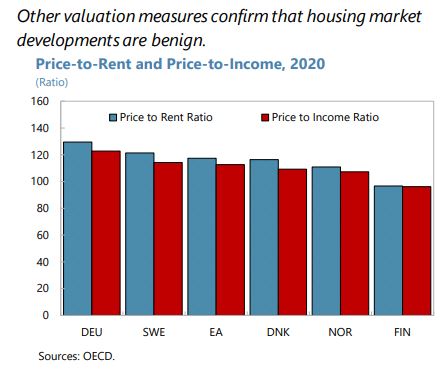

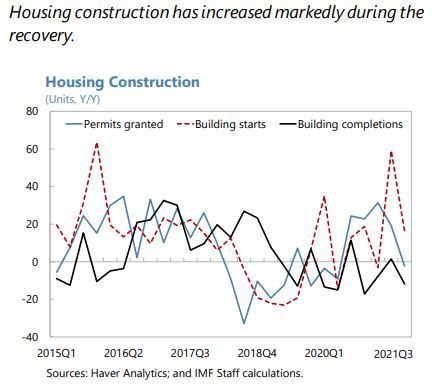

“The increase and changing composition of household debt continues to pose borrower-side vulnerabilities. Pre-pandemic, real estate prices were not overvalued, but household debt was increasing (although still low relative to Nordic peers). Much of this new debt was in the form of housing company loans—loans that finance buying shares of a housing company that may be connected to a specific apartment instead of purchasing it directly—which mask risk exposures for households. Unsecured consumer credit was also on the rise. As the pandemic struck, the authorities relaxed loan-to-collateral (LTC) requirements for housing loans. This was accompanied by an increase in highly leveraged borrowing, and housing valuations rose throughout Finland. Housing price growth has begun to moderate somewhat in the second half of 2021.

(…)

The authorities are taking steps to mitigate vulnerabilities in household finances. Following the recent increase in highly leveraged mortgage borrowing, the authorities tightened the LTC limit to pre-pandemic levels. Parliament will discuss in the spring of 2022 a draft bill on borrower-based macroprudential tools including maturity limits for housing and housing company loans, and loan-to-value (LTV) limits for housing company loans (a debt-to-income (DTI) cap was removed from the draft bill due to strong industry and political opposition). Additionally, an electronic registry of housing company shares should be operational by end-2022, making it easier to assess risks of investing in housing companies. But implementation of the planned comprehensive credit registry has been delayed to 2024 due to technical constraints.

Staff recommend that more steps be taken to enhance the macroprudential toolkit and strengthen macrofinancial resilience. The macroprudential toolkit could be enhanced further to include: (i) a DTI cap in line with recommendations from the government-appointed working group and reflecting growing household debt vulnerabilities; and (ii) supplementing the DTI cap with a debt-service-to-income cap once the new comprehensive credit registry is operational. Features of the tax code that create incentives for investors to favor housing company loans should be addressed so as to mitigate compositional changes in household debt (the recent MOF review concluded that separating the treatment of housing company shareholders’ loans’ amortization costs from interest and other expenses could help balance incentives). In this context, data relating to consumer credit and housing companies should be improved.”

From the IMF’s latest report on Finland:

“The increase and changing composition of household debt continues to pose borrower-side vulnerabilities. Pre-pandemic, real estate prices were not overvalued, but household debt was increasing (although still low relative to Nordic peers). Much of this new debt was in the form of housing company loans—loans that finance buying shares of a housing company that may be connected to a specific apartment instead of purchasing it directly—which mask risk exposures for households.

Posted by at 12:16 PM

Labels: Global Housing Watch

Subscribe to: Posts