Wednesday, August 3, 2022

Visions of Mahbub

From an article in Tribune by Murtaza Syed:

“Mahbub ul Haq taught me all I know about economics that is ultimately worth knowing. In a nation cruelly short of heroes, Mahbub, my first boss, was a shining light. As Chief Economist of the Planning Commission in the 1960s, he punctured the celebrated high growth rates of the Ayub era. He showed an enraptured domestic audience that state resources had been misused to create powerful monopolies that stifled entrepreneurship and only survived because of subsidies. As a result, the benefits of this growth had been hijacked by a handful of families, who controlled the majority of the country’s land and industrial wealth.

Later, as an adviser to World Bank President Robert McNamara, Mahbub launched a frontal assault on the false god of economic growth and its cathedral on earth, the free play of market forces. He pointed out that across the world, too, growth often fails to translate into better lives for ordinary people. Moreover, he argued that the mythical forces of demand and supply do not work when people are shackled by low purchasing power or a handful has monopoly power. To address this, he saw a vital role for the state in kick-starting the process of growth and ensuring it was equitably shared. Through these insights, he pioneered the paradigm of human development, and with it the vastly influential human development index which looks beyond GDP to capture other vital dimensions of human well-being like decent education, good health, political freedom, cultural identity, personal security, community participation, and environmental security.

Mahbub was a man ahead of his time. His eloquence reverberated on the world stage. He emerged as the spokesperson of the developing world, incessantly appealing to the conscience of richer nations. He is missed every day. Today, a quarter century after his untimely passing, his beloved homeland remains mired in desperate poverty and massive inequality. While most of our neighbours have taken off, we remain stuck at a per capita income of a little over $1,000 and every third person lives on less than $3 a day. Almost half our people are illiterate and less than a quarter of our women work.

Much like in Mahbub’s time, the fault still lies in the engines of our growth and the fickleness of our public policies. Our politicians are obsessed with growth at any cost but pull the wrong levers to achieve it time and time again: lazy, short-term stimulus that inevitably leads to painful busts as opposed to the long and winding road of structural reforms that unleashes prolonged growth through higher productivity and innovation. Short-termism associated with political cycles and an unfortunate lack of preparation and imagination among the economic teams of political parties is to blame.

Pakistan today is a country that can barely grow above 4-5% without finding itself hobbled by a current account deficit it cannot finance. Its growth model is too reliant on consumption, which accounts for a staggering 95% of overall output, while investment and exports make up just 15 and 10%, respectively. As a result, the country runs a perennial current account deficit, in stark contrast to the surpluses generated by the high-saving Asian tigers of the 1970s and 1980s.’

Continue reading here.

From an article in Tribune by Murtaza Syed:

“Mahbub ul Haq taught me all I know about economics that is ultimately worth knowing. In a nation cruelly short of heroes, Mahbub, my first boss, was a shining light. As Chief Economist of the Planning Commission in the 1960s, he punctured the celebrated high growth rates of the Ayub era. He showed an enraptured domestic audience that state resources had been misused to create powerful monopolies that stifled entrepreneurship and only survived because of subsidies.

Posted by at 9:40 AM

Labels: Macro Demystified

Monday, August 1, 2022

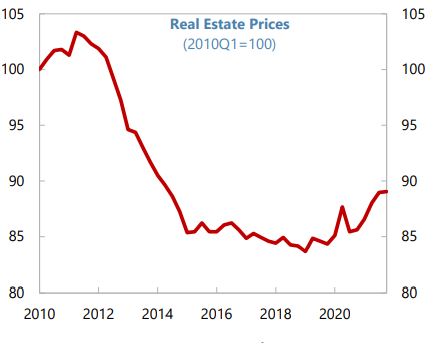

House Prices in Italy

Posted by at 8:34 AM

Labels: Global Housing Watch

Is this a recession?

From Econbrowser:

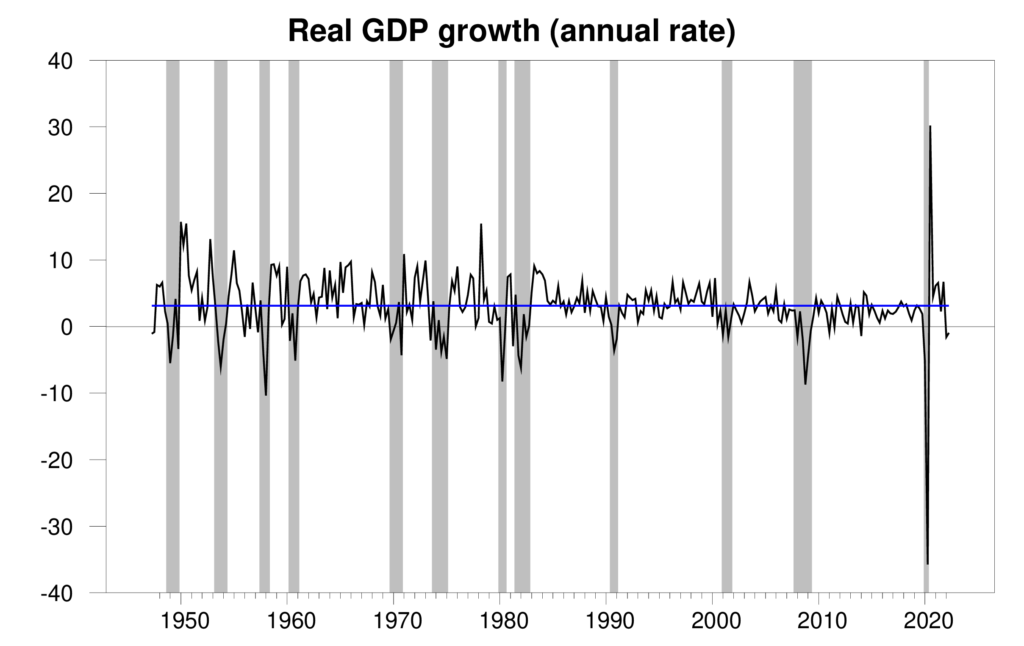

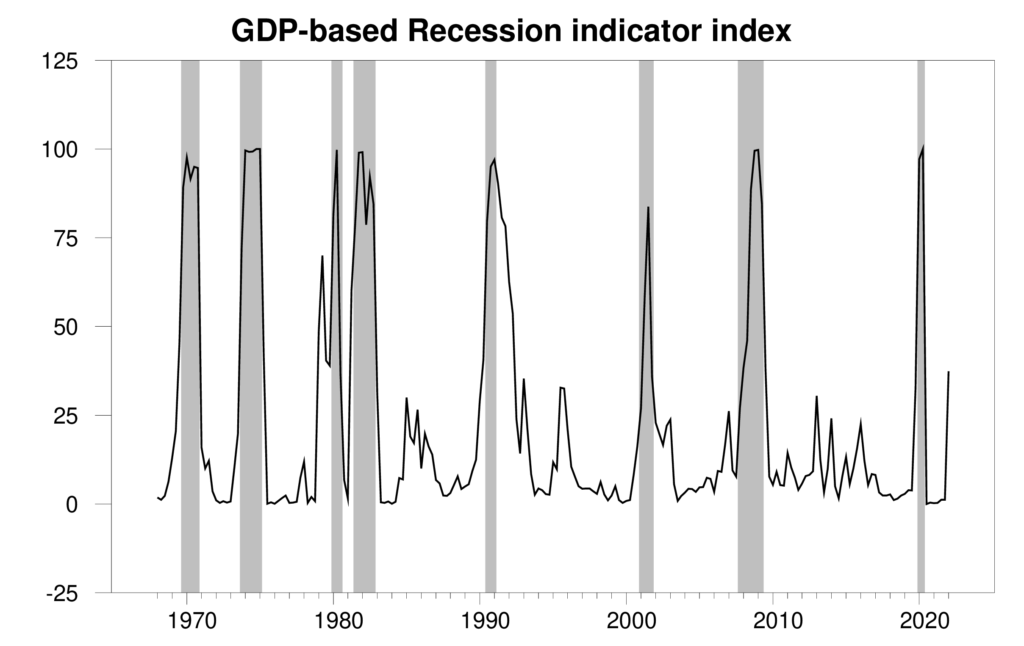

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP fell at a 0.9% annual rate in the first quarter. That makes two quarters in a row of falling real GDP, which is one rule of thumb for declaring the economy to be in a recession. The current economic weakness could certainly develop into a recession. But the evidence isn’t convincing that a recession is already under way.

The new data raised the Econbrowser recession indicator index up to 37.4%, flashing a clear warning sign. This is an assessment of the situation of the economy in the previous quarter (namely 2022:Q1). The index takes into account the fact that we’ve now seen two consecutive quarters of falling GDP, but still finds the evidence inconclusive as to whether the U.S. economy started a recession in the first quarter. When Marcelle Chauvet and I first developed this index 17 years ago, we announced that we would only declare a recession to have started when the index rises to 65% (see pages 14-15 in our original paper). If the Q3 GDP report causes the index to rise above 65%, we would announce a recession at that time, and also use the full range of revised historical data available at that time to determine the date at which the recession likely started. Here at Econbrowser we’ve followed that procedure to the letter as the data unfolded in real time over the last 17 years, successfully dating in real time the beginning and end of the two recessions since we started this blog.”

Continue reading here.

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP fell at a 0.9% annual rate in the first quarter. That makes two quarters in a row of falling real GDP, which is one rule of thumb for declaring the economy to be in a recession. The current economic weakness could certainly develop into a recession. But the evidence isn’t convincing that a recession is already under way.

Posted by at 8:22 AM

Labels: Macro Demystified

Housing Boom and Headline Inflation: Insights from Machine Learning

From a new IMF working paper by Yang Liu, Di Yang, and Yunhui Zhao:

“Inflation has been rising during the pandemic against supply chain disruptions and a multi-year boom in global owner-occupied house prices. We present some stylized facts pointing to house prices as a leading indicator of headline inflation in the U.S. and eight other major economies with fast-rising house prices. We then apply machine learning methods to forecast inflation in two housing components (rent and owner-occupied housing cost) of the headline inflation and draw tentative inferences about inflationary impact. Our results suggest that for most of these countries, the housing components could have a relatively large and sustained contribution to headline inflation, as inflation is just starting to reflect the higher house prices. Methodologically, for the vast majority of countries we analyze, machine-learning models outperform the VAR model, suggesting some potential value for incorporating such models into inflation forecasting.”

From a new IMF working paper by Yang Liu, Di Yang, and Yunhui Zhao:

“Inflation has been rising during the pandemic against supply chain disruptions and a multi-year boom in global owner-occupied house prices. We present some stylized facts pointing to house prices as a leading indicator of headline inflation in the U.S. and eight other major economies with fast-rising house prices. We then apply machine learning methods to forecast inflation in two housing components (rent and owner-occupied housing cost) of the headline inflation and draw tentative inferences about inflationary impact.

Posted by at 8:18 AM

Labels: Global Housing Watch

Adapting to flood risk: Evidence from global cities

From a VoxEU post by Sahil Gandhi, Matthew Kahn, Rajat Kochhar, Somik Lall, and Vaidehi Tandel:

“Climate change is increasing the frequency and intensity of disasters, but the ability to cope varies widely across the globe. This column examines how city death tolls and economic activity are affected by flooding. Richer places with the resources and infrastructure to cope with disasters tend to be more resilient. Compared to cities in low-income countries, those in high-income countries suffered fewer deaths per disaster, adapted over the years to better mitigate the effects of flooding, and recovered faster from economic damage.

The major floods in India and Australia in 2022 have once again drawn attention to the destructive capacity of disasters. Climate change is likely to increase the frequency and intensity of these shocks. At the same time, the ability to cope with disasters will vary widely across places and over time. The living conditions of households in India are very different from those in Australia. In India, a large proportion of urban households live in slums on hillslopes or other unsafe areas. The impact of similar disasters would be different for the two countries. Given that a majority of people around the world now live in cities, it is important to measure the vulnerability and adaptive capacity of such productive areas to disasters.

Cities in developing countries suffer more

Research on the impact of extreme weather predicts that the developing world, especially the poor and vulnerable populations, will be disproportionately affected (Mendelsohn et al. 2000, Mendelsohn et al. 2006, Tol 2009).

In our new paper (Gandhi et al. 2022), we use data on floods for 9,468 cities in 175 countries to examine the differential impact of floods on cities in high- and low-income countries. We combine monthly night light (VIIRS) data for these cities from 2012 to 2018 with a global dataset of geocoded disasters. Figure 1 shows that after a flood event, night lights fall and then recover. Floods disrupt life in cities through temporary power failures, disruption of essential services, damage to property, and temporary closure of offices and factories. These are reflected in the lights seen at night (Kocornik-Mina et al. 2016).”

Continue reading here.

From a VoxEU post by Sahil Gandhi, Matthew Kahn, Rajat Kochhar, Somik Lall, and Vaidehi Tandel:

“Climate change is increasing the frequency and intensity of disasters, but the ability to cope varies widely across the globe. This column examines how city death tolls and economic activity are affected by flooding. Richer places with the resources and infrastructure to cope with disasters tend to be more resilient. Compared to cities in low-income countries,

Posted by at 8:14 AM

Labels: Global Housing Watch

Subscribe to: Posts