Friday, May 13, 2022

Housing Market in New Zealand

From the IMF’s latest report on New Zealand:

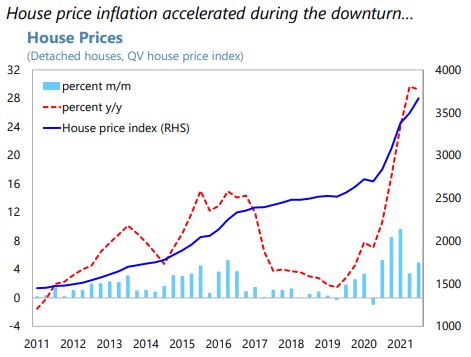

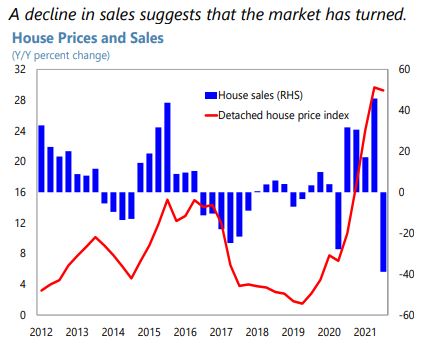

“House prices have peaked and are expected to correct. The market is turning given that important drivers over previous years, such as low mortgage rates and easy credit availability, are now reversing (…). The recent trend of falling sales volumes and mortgage lending is expected to continue, supporting a house price correction, although the period and intensity are difficult to estimate.

Rising mortgage rates and recent policy actions are curbing demand. In response to actual and expected withdrawal of monetary stimulus, standard mortgage rates rose by between 40 and 150 bps in 2021H2. The removal of property investors’ tax deductibility of mortgage interest and the extension of the minimum holding period to exempt capital gains on investment properties from income tax have contributed to a decline in investor demand. The RBNZ re-introduced loan-to-value ratio (LVR) limits on mortgages in March 2021 and tightened them in May and November. The December 2021 amendments to the Credit Contracts and Consumer Finance Act (CCCFA), designed to protect borrowers and strengthen the consumer credit regulatory regime, had the unintended effect of tightening credit conditions further. These developments contributed to a significant decline in mortgage lending (-31 percent y/y in March 2022), with new loans to investors and highly leveraged buyers (LVR exceeding 80 percent) declining more rapidly (-44 percent and -56 percent y/y, respectively). The RBNZ intends to implement additional MPMs for potential future use to broaden its toolkit. A framework to introduce DTI ceilings will be released by end-2022 for implementation by mid-2023. The RBNZ is also looking at the possible use of a floor on test interest rates to assess borrowers’ ability to meet debt service obligations.

Efforts are ongoing to improve housing supply. A NZ$3.8 billion (around 1.1 percent of GDP) allocation was made to the Housing Acceleration Fund to increase housing supply and improve affordability. Amendments to the Resource Management Act (RMA) in October 2021 allow for higher-density housing construction without requiring resource consent, making it easier to build new homes. However, these measures will take time to bear fruit: a cost-benefit appraisal by the Treasury estimated that about 75,000 additional dwellings would be built in the next 5-8 years, with more than 200,000 additional dwellings available in 20 years. The government is also in the process of reforming the RMA, which should streamline planning processes. There are plans to boost effective land supply by incentivizing local authorities to approve new housing projects faster.

Staff Views

Tackling housing imbalances requires a comprehensive approach, and recent initiatives will help address these imbalances. Achieving long-term housing sustainability and affordability depends critically on freeing up land supply, improving planning and zoning, and fostering infrastructure investments to enable fast-track housing developments and lower construction costs. There is a need for continued spending on land, infrastructure, and housing, including financial incentives that enable and incentivize local councils and iwi (Māori tribal organizations) to provide infrastructure for new developments. Increasing the stock of social housing also remains important in the near term, while supply constraints are addressed over time.

A moderation of prices is widely expected, and macroprudential policy should be adjusted commensurate with the evolution of financial stability risks. The use of macroprudential measures to address the financial stability impact of surging house prices has been appropriate. LVR restrictions have been effective in making lending for housing more cautious. Restrictions could be relaxed in case of a stronger-than-expected downturn in the housing market. Financial stability risks from a sharp downturn in the housing market are limited given high bank capitalization, but pockets of vulnerability, particularly among recent borrowers, may exist. More broadly, in case of a sharp downturn, potentially reinforced by a faster rise in interest rates, there could be a significant impact on consumption through wealth and confidence effects. A more extensive MPM toolkit, including the ability to readily implement DTI ceilings and loan serviceability test interest rate requirements when warranted, would be useful in addressing future risks.

Authorities’ Views

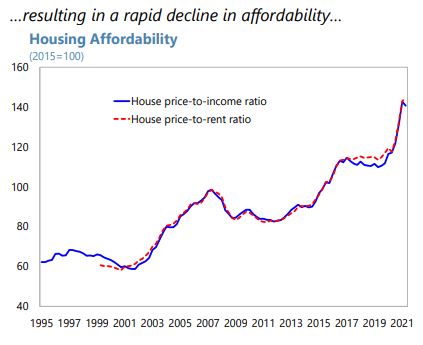

The authorities stressed that, while the housing cycle had likely turned, improving affordability remained a key priority. While prices are expected to decline in 2022, this only partially reverses the very large increases of recent years and will therefore not make a significant impact on affordability. A comprehensive approach covering the demand and supply sides of housing is underway, with more initiatives planed under the wider review of the RMA and laid out in the National Policy Statement on Urban Development. The Housing Acceleration Fund will provide funding at the local level for infrastructure development, and the first tranche of projects is likely to be approved soon. The authorities emphasized their commitment to invest in social housing. They agreed that the CCCFA amendments may have impacted credit conditions, though the effect is hard to quantify. They noted that clarifications have already been issued, with further changes being considered in consultation with the industry.”

Posted by at 6:49 PM

Labels: Global Housing Watch

Subscribe to: Posts