Monday, November 15, 2021

Housing Market in Netherlands

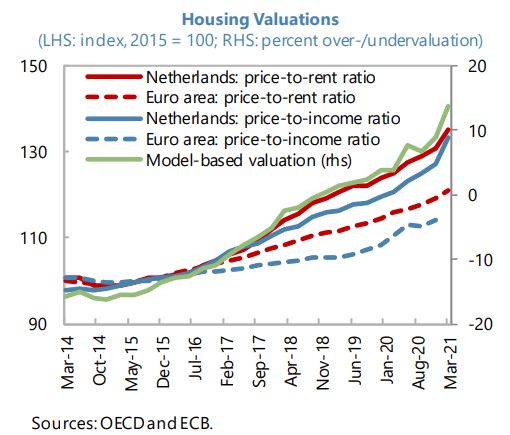

From the IMF’s latest report on Netherlands:

“Real estate markets call for heightened vigilance and the pursuit of policies to address near-term risks and long-term challenges confronting residential and commercial properties. Prices – and valuations – for housing have continued to soar during the pandemic (see chart), reflecting longstanding supply bottlenecks, low interest rates, and the favorable tax treatment of owner-occupied housing. Existing vulnerabilities have been exacerbated by a further rise in already elevated levels of mortgage debt, with some households exceedingly stretching their debt servicing capacity. Consequently, the activation of floors for risk weights applied to mortgage lending from 2022 is welcome and may be complemented by measures such as an additional reduction in eligible loan-to-value ratios, and reviewing the taxation of owner-occupied housing. In addition, efforts to improve the elasticity of the housing supply appear warranted, as structural rigidities, such as distorted planning incentives and restrictive building or zoning laws, maintain imbalances. Such policies will also support macroeconomic stability by lessening households’ exposure to house-price fluctuations, which can significantly affect consumer spending.

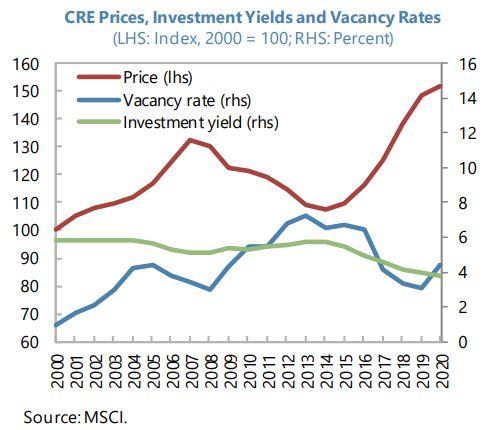

Vacancy rates for commercial properties have increased due to the recession yet with little effect on prices as investment yields have stayed attractive in relation to other assets. With banks maintaining comparatively large exposures, valuation has become a concern, especially since long-term structural change may prevent the full recovery of some property segments. The authorities should contemplate options to better steer the investment cycle of commercial real estate to avoid a build-up of financial stability risks, potentially modelled on policies in place for owner-occupied dwellings. Furthermore, incentivizing climate-friendly modernization or the rededication of obsolete structures should help preserve the value of existing buildings.”

From the IMF’s latest report on Netherlands:

“Real estate markets call for heightened vigilance and the pursuit of policies to address near-term risks and long-term challenges confronting residential and commercial properties. Prices – and valuations – for housing have continued to soar during the pandemic (see chart), reflecting longstanding supply bottlenecks, low interest rates, and the favorable tax treatment of owner-occupied housing. Existing vulnerabilities have been exacerbated by a further rise in already elevated levels of mortgage debt,

Posted by at 11:30 AM

Labels: Global Housing Watch

Credit, crises, and inequality

In a recent working paper of the Bank of England (2021), authors Jonathan Bridges, Georgina Green, and Mark Joy evaluate a panel dataset of 26 developed nations over 5 decades preceding the Covid-19 pandemic to show that inequality rises following recessions, and rapid credit growth in the time until downturn exacerbates that effect. This growth, whether financial or normal in nature, increases unemployment and inequality effects. They observe that “one standard deviation credit boom leads to a 40% amplification of the distributional fallout in the bust that follows”.

Moreover, “low bank capital ahead of a downturn amplifies the inequality increase that follows. These insights add a new dimension to policy cost-benefit analysis, at the distributional level.” The paper’s results indicate that a 55% amplification in the cyclical response of income inequality to a recession if a country enters the recession with bank capital ratios one standard deviation lower than average. The authors note that using the tools established in new macroprudential norms empower economies to safeguard their financial stability using both borrower and lender resilience, but can also lead to distributional costs in the event of an untamed crisis.

“Taken together, these results suggest an important link between credit, crises, and inequality. They demonstrate that tail events for the macroeconomy also represent distributional shocks.” Vulnerabilities like the rapid accumulation of debt, weakening of bank capital, and an increased risk of recession transforming into a full-fledged financial crisis can all contribute to distributional effects and rising inequalities when a crisis actually strikes. While the use of macroprudential policies to address these vulnerabilities has both, associated costs and benefits, entirely avoiding the usage of these policies entirely can lead to severe macroeconomic and distributional ill effects.

Click here to read the full paper.

In a recent working paper of the Bank of England (2021), authors Jonathan Bridges, Georgina Green, and Mark Joy evaluate a panel dataset of 26 developed nations over 5 decades preceding the Covid-19 pandemic to show that inequality rises following recessions, and rapid credit growth in the time until downturn exacerbates that effect. This growth, whether financial or normal in nature, increases unemployment and inequality effects. They observe that “one standard deviation credit boom leads to a 40% amplification of the distributional fallout in the bust that follows”.

Posted by at 9:01 AM

Labels: Inclusive Growth, Macro Demystified

Trade, development and political economy: The life and work of Ronald Findlay, 1935-2021

From a VoxEU post by Douglas Irwin:

“Ronald Findlay, who passed away in October 2021, was one of the great trade theorists of his generation. As this column by one of his former students explains, he will be remembered for his brilliant intellect, his encyclopaedic knowledge of theory and history, and most of all for his modesty, warmth and supportive friendship.

Ronald Findlay, one of the great trade theorists of his generation, passed away in October 2021 at the age of 86. A professor of economics at Columbia University from 1969 to 2013, he anchored the international economics group there for more than four decades. He will be remembered by colleagues and students for his brilliant intellect, his encyclopaedic knowledge of theory and history, and most of all for his modesty, warmth and supportive friendship.

Findlay was born and raised in Burma but was forced to flee the country on foot during the Second World War.1 After the war, he returned and later received an excellent education at the University of Rangoon. A precocious student, Findlay was appointed as a teaching tutor at the age of 19, and he was giving economic advice to the Burmese government in his very early 20s.2

In 1957, Findlay went to graduate school at MIT where Robert Solow was his dissertation adviser. He was also deeply influenced by Charles Kindleberger and “the master” Paul Samuelson. As a graduate student, Findlay published several papers, including his 1959 classic with Harry Grubert, “Factor Intensities, Technological Progress, and the Terms of Trade”. This paper examined the impact of Hicks-neutral and factor-biased technological change on production and factor allocation in a simple two-good, two-factor model. This influential analysis illuminated some important features of that workhorse model, and it continued to be influential when the issue of factor-biased technical change returned to prominence in the 1980s and 1990s.

Findlay completed his PhD in just three years and returned to Burma to teach at Rangoon.3 One early paper stepped into the minefield of the Cambridge versus Cambridge capital theory and sought to formalise Joan Robinson’s model of accumulation, something that had to be done “due to the obscurity of Mrs. Robinson’s literary presentation of what are fairly intricate quantitative relationships” (Findlay 1963). The paper not only elicited a reply from the formidable Cambridge economist, she even made a special trip to Burma (detouring from India) just to “have it out with this young Findlay guy”, as he later put it.

This paper and other early work displayed what was a trademark Findlay approach: to provide a formal model of what was implicit in the non-mathematical writings of economists such as Arthur Lewis and Ragnar Nurkse. The goal was to provide a check on the underlying logical structure of non-traditional approaches and see under what conditions the claims for them might hold. For example, Findlay (1959) showed that a policy of “balanced growth”, as advocated by Lewis and Nurkse, would not solve the problem of increasing the returns to investment and could be counterproductive compared with international specialisation along lines of comparative advantage.

Continue reading here.

From a VoxEU post by Douglas Irwin:

“Ronald Findlay, who passed away in October 2021, was one of the great trade theorists of his generation. As this column by one of his former students explains, he will be remembered for his brilliant intellect, his encyclopaedic knowledge of theory and history, and most of all for his modesty, warmth and supportive friendship.

Ronald Findlay, one of the great trade theorists of his generation,

Posted by at 6:05 AM

Labels: Profiles of Economists

Saturday, November 13, 2021

Evaluating Interventions for Public Infrastructure Maintenance and Usage

In their recent study (2021), professors Alex Armand, Britta Augsburg, and Antonella Bancalari examine whether externally incentivizing maintenance can sustainably improve the quality of public infrastructure using interventions adopted for maintaining community toilets in India.

Two different types of interventions were analyzed. Firstly, the ‘maintenance’ intervention which offered a one-off grant at the facility level, followed by a significant bimonthly financial reward to the facility’s caretaker or the person in charge of its maintenance (40% of the caretakers’ monthly salary, conditional on keeping the facility clean). The second type was ‘maintenance plus sensitization’, supplementing the maintenance intervention with an intensive sensitization campaign to raise awareness among potential users about the importance of a well-kept facility and of avoiding free riding to support good services.

It was observed that the maintenance intervention led to improvements in the observed quality of facilities, accompanied by a significant reduction in free riding among users, but incentivizing maintenance had no impact on the value use and attitudes of potential users. As for the other intervention, it was found that the sensitization campaign alone had no effects other than increasing overall health awareness among users.

The column also sheds light on policymakers’ decisions on financing interventions and draws out pertinent policy implications for various approaches.

Click here to read the full article.

In their recent study (2021), professors Alex Armand, Britta Augsburg, and Antonella Bancalari examine whether externally incentivizing maintenance can sustainably improve the quality of public infrastructure using interventions adopted for maintaining community toilets in India.

Two different types of interventions were analyzed. Firstly, the ‘maintenance’ intervention which offered a one-off grant at the facility level, followed by a significant bimonthly financial reward to the facility’s caretaker or the person in charge of its maintenance (40% of the caretakers’ monthly salary,

Posted by at 9:20 AM

Labels: Inclusive Growth

Friday, November 12, 2021

Could clean energy be the answer to China’s demographic woes? Dean Baker answers.

In a column for the Center for Economic and Policy Research, a Washington DC-based think tank, economist Dean Baker writes on the opportunity for China to invest in clean energy to resolve its “demographic crisis”. An excerpt from the article is as follows.

“As Paul Krugman wrote in a recent column, China is going to have to make a massive adjustment in its economy in the years ahead. It has been spending an incredible 43 percent of its GDP on capital formation, either investment goods purchased by businesses, or residential housing. By comparison, the figure for Japan is 24 percent and for the United States less than 22 percent.

This massive spending on capital formation made sense when China was seeing rapid growth in its labor force and also a huge shift in its population from rural to urban. But this process is now reaching an endpoint, both with a decline in its working-age population and the rural to urban shift largely completed.

It is also important to note that China is already heavily invested in clean energy. China is by far the world leader in solar energy, with more than twice as much as the United States, the second-largest user of solar power. It is also by far the world leader in wind energy, again with more than twice as much installed wind power as the United States. And, China also has more than twice as many electric cars on the road as any other country. This means that China has a large domestic clean energy sector which can stand to gain by further spending on reducing greenhouse gas emissions.

If China wants a path through its “demographic crisis,” or, in other words, coping with secular stagnation, devoting substantial resources towards greening its economy would be a great path forward. In the process, they can also give a big hand to the rest of the world, both by sharing the technology and showing how it can be done, as well as reducing the damage they are doing to the planet themselves.”

Source: Baker, D. (2021). CEPR. Combatting Global Warming: The Solution to China’s Demographic “Crisis”.

Click here to read the full article.

In a column for the Center for Economic and Policy Research, a Washington DC-based think tank, economist Dean Baker writes on the opportunity for China to invest in clean energy to resolve its “demographic crisis”. An excerpt from the article is as follows.

“As Paul Krugman wrote in a recent column, China is going to have to make a massive adjustment in its economy in the years ahead. It has been spending an incredible 43 percent of its GDP on capital formation,

Posted by at 7:49 AM

Labels: Energy & Climate Change, Inclusive Growth

Subscribe to: Posts