Wednesday, November 17, 2021

When Residential Real Estate Turned Commercial: Working from Home

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

The size of the shift is remarkable. Janice C. Eberly, Jonathan Haskel and Paul Mizen discuss “Potential Capital: Working From Home, and Economic Resilience” (NBER Working Paper 29431, October 2021, subscription needed). They compare the drop in economic output from the workplace in the first two quarters of 2020 to the overall drop in economic output: in the US economy, for example, they find that output in the workplace fell by about 17%, but total economic output actually fell about 9%. Work done outside the conventional workplace made up the difference.

This built-in resilience of the economy may now seem pretty obvious, but it wasn’t obvious (at least to me) before the pandemic hit. The magnitudes here are enormous. According the US Bureau of Economic Analysis, the value of residential real estate in 2020 was almost $25 trillion. Privately owned nonresidential structures were worth almost $16 trillion, while the equipment in those structures was another $7 trillion. In short, trillions of dollars of residential capital replaced trillions of dollars of nonresidential capital in a very short time. The transition was far from seamless or painless, of course, but the fact that it happened at all is worth a gasp.”

Continue reading here.

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

Posted by at 6:34 AM

Labels: Global Housing Watch

The post-war rise of popular wealth

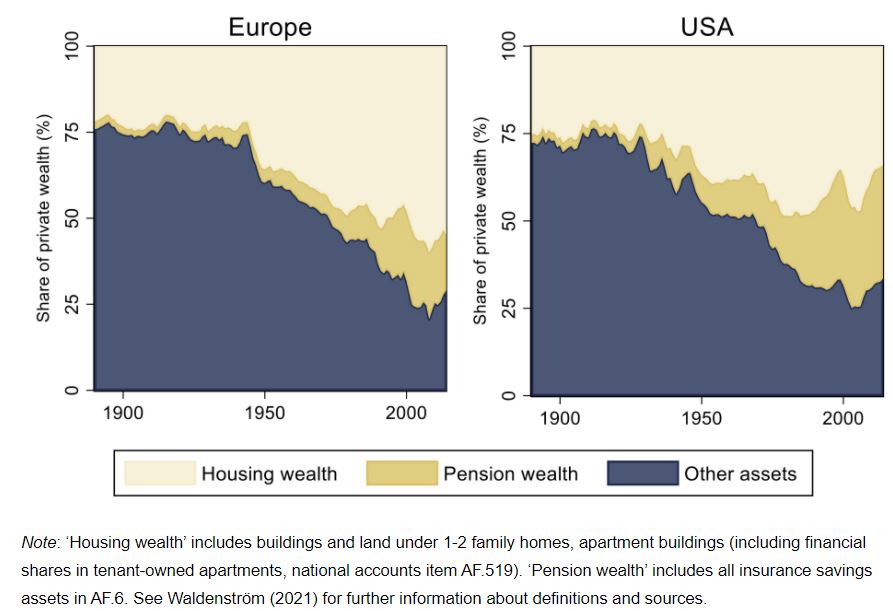

From a VoxEU post by Daniel Waldenström:

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich. During the post-war period, wealth accumulation came mainly in housing and funded pensions, which are assets held by ordinary people. This compositional trend had important distributional implications.”

Figure 3 Decomposing aggregate wealth-income ratios since 1890

Continue reading here.

From a VoxEU post by Daniel Waldenström:

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich.

Posted by at 6:30 AM

Labels: Global Housing Watch

Tuesday, November 16, 2021

Macrofinancial Causes of Optimism in Growth Forecasts

New IMF Working paper by Yan Carrière-Swallow and José Marzluf

“We analyze the causes of the apparent bias towards optimism in growth forecasts underpinning the

design of IMF-supported programs, which has been documented in the literature. We find that

financial variables observable to forecasters are strong predictors of growth forecast errors. The

greater the expansion of the credit-to-GDP gap in the years preceding a program, the greater its

over-optimism about growth over the next two years. This result is strongest among forecasts that

were most optimistic, where errors are also increasing in the economy’s degree of liability

dollarization. We find that the inefficient use of financial information applies to growth forecasts more

broadly, including the IMF’s forecasts in the World Economic Outlook and those produced by

professional forecasters compiled by Consensus Economics. We conclude that improved

macrofinancial analysis represents a promising avenue for reducing over-optimism in growth

forecasts.”

New IMF Working paper by Yan Carrière-Swallow and José Marzluf

“We analyze the causes of the apparent bias towards optimism in growth forecasts underpinning the

design of IMF-supported programs, which has been documented in the literature. We find that

financial variables observable to forecasters are strong predictors of growth forecast errors. The

greater the expansion of the credit-to-GDP gap in the years preceding a program, the greater its

over-optimism about growth over the next two years.

Posted by at 4:26 PM

Labels: Forecasting Forum

The Feminist Building Blocks of Just, Sustainable Economy

In a recent column for Social Europe, a public policy discussion and publication platform, and the IPS-Journal, the reputed development economist Dr. Jayati Ghosh writes about finding a blueprint for an economy that serves the public rather than the other way around.

“Feminist economists have long argued that the purpose of an economy is to support the survival and flourishing of life, in all its forms. This may seem obvious but it turns on its head the prevailing view, which implicitly assumes the opposite causation: the economy runs according to its own laws, which must be respected by mere human actors. In this market-fundamentalist perspective, it is a potential angry god which can deliver prosperity or devastation and must be placated through all sorts of measures—including sacrifices made in its name. “

Ghosh, J. (2021). The feminist building blocks of a sustainable, just economy. Social Europe.

Taking a cue from UN Women’s report titled, Feminist Plan for Sustainability and Social Justice, she writes about expanding the purview of economic valuation to include unpaid care work and environmental costs in it, the need for gender-sensitive institutions, regulations, and policies, and a boost to public investment.

Click here to read the full article.

In a recent column for Social Europe, a public policy discussion and publication platform, and the IPS-Journal, the reputed development economist Dr. Jayati Ghosh writes about finding a blueprint for an economy that serves the public rather than the other way around.

“Feminist economists have long argued that the purpose of an economy is to support the survival and flourishing of life, in all its forms. This may seem obvious but it turns on its head the prevailing view,

Posted by at 7:15 AM

Labels: Inclusive Growth

More than Economists

From a Project Syndicate post by Robert Skidelsky:

“While systematic thinkers close a subject, leaving their followers with “normal” science to fill up the learned journals, fertile ones open their disciplines to critical scrutiny, for which they rarely get credit. Three recent biographies show how this has been the fate of three great economists who were marginalized by their profession.

Jeremy Adelman, Worldly Philosopher: The Odyssey of Albert O. Hirschman, Princeton University Press, 2013.

Charles Camic, Veblen: The Making of an Economist Who Unmade Economics, Harvard University Press, 2020.

Zachary D. Carter, The Price of Peace: Money, Democracy, and the Life of John Maynard Keynes, Random House, 2020LONDON – There are two types of extraordinary economist. The first type includes pioneers of the field such as David Ricardo, William Stanley Jevons, and, in our own time, Robert Lucas. They all aimed to economize knowledge in order to explain the largest possible amount of behavior with the smallest possible number of variables.

The second category, which includes Thorstein Veblen, John Maynard Keynes, and Albert O. Hirschman, sought to broaden economic knowledge in order to understand motives and norms of behavior excluded by mainstream analysis but important in real life. The first type of economist is fiercely exclusive; the second has tried, largely in vain, to make economics more inclusive.

The first type of economist rather than the second has come to define the field, owing partly to the successful drive to professionalize the production of knowledge. Economics and other social sciences are heirs of the medieval guilds, each jealously preserving its chosen method of creating intellectual products. It also reflects the increasing difficulty in a secular age of developing moral content for the social sciences in general. We lack an agreed standpoint from outside “the science” by which to judge the value of human activity.”

Continue reading here.

From a Project Syndicate post by Robert Skidelsky:

“While systematic thinkers close a subject, leaving their followers with “normal” science to fill up the learned journals, fertile ones open their disciplines to critical scrutiny, for which they rarely get credit. Three recent biographies show how this has been the fate of three great economists who were marginalized by their profession.

Jeremy Adelman, Worldly Philosopher: The Odyssey of Albert O.

Posted by at 6:40 AM

Labels: Profiles of Economists

Subscribe to: Posts