Wednesday, October 13, 2021

Why the U.S. Housing Boom Isn’t a Bubble

Wharton’s Benjamin Keys explains why the red-hot U.S. real estate market isn’t a bubble that’s ready to burst. Home prices are likely to stay high for years to come:

“In Philadelphia, the median home price has risen 48% in the last decade. In Atlanta, the median sale price of a metro home hit an all-time high in June of $372,500. Not to be outdone by big cities, Boise, Idaho, recently ranked as the nation’s most overvalued market, where homes are selling for nearly 81% more than they should.

While the red-hot real estate market is finally showing signs of cooling, its meteoric rise has many Americans wondering if housing prices are a bubble that is about to burst, much like the collapse that triggered the Great Recession.

Wharton real estate and finance professor Benjamin Keys says that’s not the case.

“I come down very strongly against that view. I don’t think that it’s likely that we’re going to see a bubble burst in the way that we saw in 2008, 2009, and 2010,” he said during an interview with Wharton Business Daily on SiriusXM. (Listen to the podcast above.)

Although the frenzied buying and inflated prices are reminiscent of the run-up to the recession, Keys said there are several factors that make the current market different. First, loan standards that were loosened during the bubble are much tighter now, with stringent requirements for good credit, complete documentation, and a sizeable down payment. In contrast, the pre-recession years were pocked with subprime mortgages, low teaser interest rates that ballooned, weak underwriting, negatively amortized construction, and other questionable practices.

Second, the boom of the early 2000s was also driven by a surge in home construction that led to abundant supply. But there’s been a building shortage over the last 10 years, especially in cities with high demand. The result is a supply-demand mismatch that can’t be resolved quickly or easily.

“I think there was a bit of a hangover coming out of that 2000 boom and bust, and we’re underbuilt in a lot of cities where there’s demand for jobs, where there’s demand for housing,” Keys said.”

Continue reading here.

Wharton’s Benjamin Keys explains why the red-hot U.S. real estate market isn’t a bubble that’s ready to burst. Home prices are likely to stay high for years to come:

“In Philadelphia, the median home price has risen 48% in the last decade. In Atlanta, the median sale price of a metro home hit an all-time high in June of $372,500. Not to be outdone by big cities, Boise, Idaho, recently ranked as the nation’s most overvalued market,

Posted by at 10:03 AM

Labels: Global Housing Watch

Tuesday, October 12, 2021

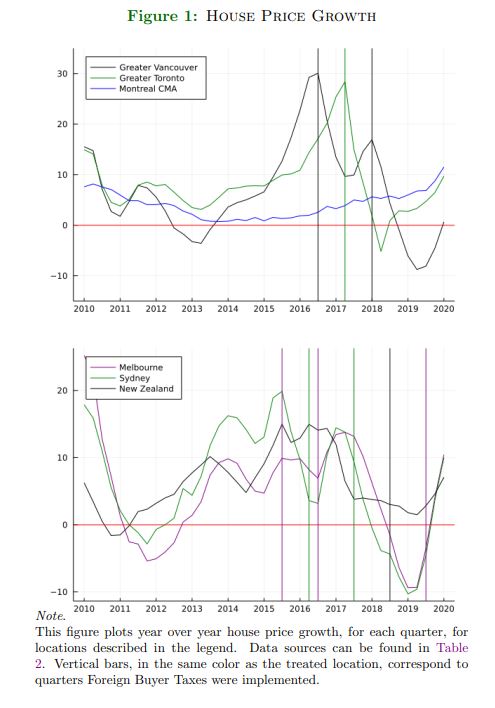

Do Foreign Buyer Taxes Affect House Prices?

From a new paper by Jonathan S. Hartley, Li Ma, Susan Wachter and Albert Alex Zevelev:

“This paper studies the impact of foreign buyer taxes on house prices using recent law changes in Canada, Australia, and New Zealand. Counterfactual house prices are estimated for each treated location combining prediction techniques from machine learning with inference methods from the Synthetic Control Method literature. In general, foreign buyer taxes have negative, large, and persistent effects on house price growth. We find bigger effects in locations with bigger taxes and with higher immigrant shares. Alternative outcome variables, including population growth, GDP growth, and unemployment rates were either unaffected or slightly affected in ways that do not confound our results.”

From a new paper by Jonathan S. Hartley, Li Ma, Susan Wachter and Albert Alex Zevelev:

“This paper studies the impact of foreign buyer taxes on house prices using recent law changes in Canada, Australia, and New Zealand. Counterfactual house prices are estimated for each treated location combining prediction techniques from machine learning with inference methods from the Synthetic Control Method literature. In general, foreign buyer taxes have negative, large, and persistent effects on house price growth.

Posted by at 8:19 PM

Labels: Global Housing Watch

House Prices and Consumer Price Inflation

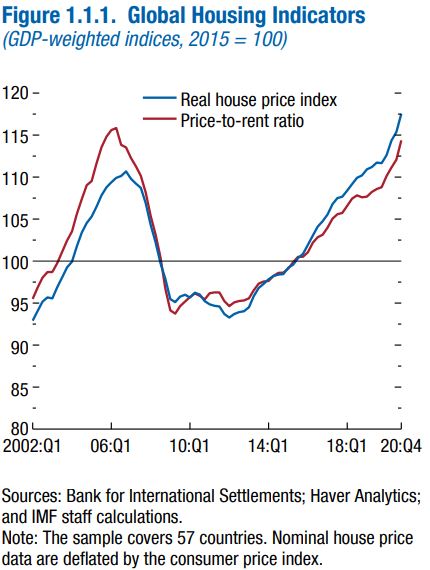

From new work by IMF Colleagues (Nina Biljanovska, Chenxu Fu, and Deniz Igan):

“Contrary to the expectation that house prices would decline during recessions (Igan and others 2011; Duca, Muellbauer, and Murphy, forthcoming), real house prices rose by 5.3 percent, on average, globally in 2020 as the pandemic-induced economic downturn took hold. Perhaps more strikingly, this was the highest annual growth rate observed in the past 15 years (Figure 1.1.1). While house price growth has breezed ahead, residential rents have grown at a slower rate, rising by 1.8 percent, on average, across countries over the same period.

Implications of a hot housing market for consumer prices

The house price surge comes at a time when questions are mounting over post-pandemic inflation dynamics (see Chapter 2). House prices matter for inflation because—through an asset pricing equation—they are linked to two measures of housing costs that could enter the CPI. One is the actual rent paid by tenants. The other is the imputed rent, or owner’s equivalent rent, which is an estimate of how much homeowners would need to pay were they to rent their own house. Overall, the rent component accounts, on average, for about 20 percent of the CPI.

How much of an increase in inflation is expected?“

Continue reading here.

From new work by IMF Colleagues (Nina Biljanovska, Chenxu Fu, and Deniz Igan):

“Contrary to the expectation that house prices would decline during recessions (Igan and others 2011; Duca, Muellbauer, and Murphy, forthcoming), real house prices rose by 5.3 percent, on average, globally in 2020 as the pandemic-induced economic downturn took hold. Perhaps more strikingly, this was the highest annual growth rate observed in the past 15 years (Figure 1.1.1). While house price growth has breezed ahead,

Posted by at 2:14 PM

Labels: Global Housing Watch

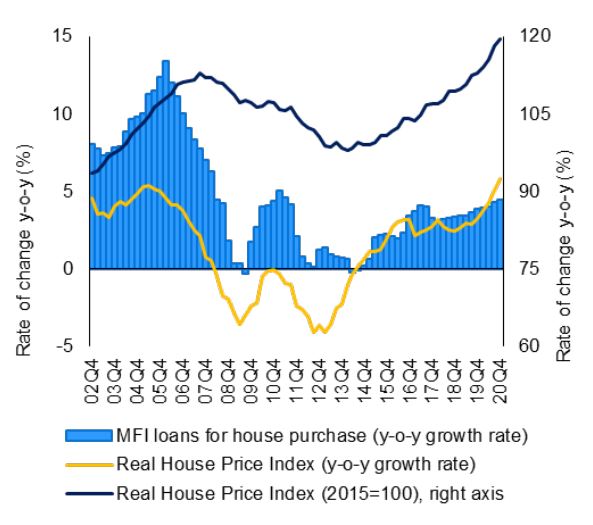

Euro Area Housing Markets: Trends, Challenges and Policy Responses

From a new paper by Vítor Martins, Alessandro Turrini, Bořek Vašíček, and Madalina Zamfir:

“The paper discusses the relevance of housing markets for macroeconomic developments from a euro area perspective, reviews trends in house prices and mortgage credit, and discusses policy approaches to prevent housing booms and deal with busts. After years of unsustainably strong house price growth in several Member States in a context of easing credit conditions, downward house price corrections took place after the 2008 financial crisis. A recovery in house prices started after 2013 under different conditions compared with the pre-financial crisis context. The house price recovery appeared to be driven to a greater extent by structural factors and to a lesser extent by buoyant household loans, as credit growth has been lagging behind house price growth in most countries. Prospects for house price growth after the COVID-19 outburst are clouded by uncertainty in light of the changing outlook when economic fundamentals and policy responses play in opposite directions. The current context is also different compared with the period before the global financial crisis because macro-prudential frameworks have been strengthened and macroprudential tools are increasingly used across the euro area. The effectiveness of policy tools needed to address risks linked to boom-bust dynamics in the real estate sector depends on their interaction, design and timely implementation. Policy composition and policy design also appear crucial in dealing with possible trade-offs among policy objectives, including between macro-financial stability and housing affordability.”

From a new paper by Vítor Martins, Alessandro Turrini, Bořek Vašíček, and Madalina Zamfir:

“The paper discusses the relevance of housing markets for macroeconomic developments from a euro area perspective, reviews trends in house prices and mortgage credit, and discusses policy approaches to prevent housing booms and deal with busts. After years of unsustainably strong house price growth in several Member States in a context of easing credit conditions, downward house price corrections took place after the 2008 financial crisis.

Posted by at 7:20 AM

Labels: Global Housing Watch

Friday, October 8, 2021

Housing View – October 8, 2021

On cross-country:

- City house prices outpace national markets. Predictions of ‘the death of the city’ now seem a distant memory as cities are now outpacing their national housing markets with prices rising by 9.8% on average in the year to Q2 2021. – Knight Frank

- Berliners Are Angry About Housing. And So Is Much of Europe. Soaring rents and out-of-reach prices have fueled property inequality – Bloomberg

- Sergei Gordeev: the Russian property tycoon betting on prefabricated blocks. Having netted billions of dollars from a housing boom, PIK’s chief executive wants to upend the sector – FT

On the US:

- It Shouldn’t Take 50 Meetings to Build Some Apartments – New York Times

- Why Isn’t There Enough Housing? Zoning And Homeowner Resistance – Forbes

- Eviction Record Expungement Can Remove Barriers to Stable Housing – Center for American Progress

- California’s Smart Plan to Let Homeowners Be Homebuilders. The way to blunt Nimby resistance to badly needed housing construction is to give single-family owners a path to profit from new development. – Bloomberg

- Why Democrats Would Be Fools to Slash Biden’s Housing Plan. Lawmakers will have to make tough decisions to reach a deal on reconciliation. But chopping historic housing investments isn’t the answer. – Politico

- Single-family Zoning: Can History be Reversed? – Harvard Joint Center for Housing Studies

- What Do Runaway Home Prices Mean for the US? – Harvard Joint Center for Housing Studies

- Mortgage Payments Are Getting More and More Unaffordable. Record growth in home prices is erasing savings typically delivered by low interest rates – Wall Street Journal

- The Housing Boom Is Not A Bubble – Forbes

- What’s Driving the Huge U.S. Rent Spike? Rent increases of 20% or more are making life difficult for low-income tenants in many cities, just as eviction bans and unemployment relief are running out. – Bloomberg

- If your rent is going up, this episode is for you – New York Times

On China

- Empty Buildings in China’s Provincial Cities Testify to Evergrande Debacle. The property giant borrowed heavily to develop in out-of-the way places like Lu’an – Wall Street Journal

- China property sector woes intensify after mid-sized developer defaults. Fantasia misses payment as Evergrande keeps investors hanging on share trading suspension – FT

- Beijing crackdown threatens to crush China’s love of London property. Thousands of high-end flats bankrolled by Chinese developers lie unfinished and unsold – FT

- The economic threats from China’s real estate bubble. Property’s great investment boom has reached its limit — the economy needs new drivers of demand – FT

On other countries:

- [Australia] RBA Remains Dovish, Warns on House Prices. The Australian central bank held the official cash rate at 0.1%, where it has stood since late 2020 – Wall Street Journal

- [Australia] Australia’s house price boom: what’s happening and how can it be brought under control? The property frenzy is locking young people out of the market and creating economic risks. Will anything stop it? – The Guardian

- [Australia] Banks given new borrowing rule as Australian house prices soar. Regulator Apra tells lenders to ensure new mortgagees can cope with three percentage point rise in interest rates – The Guardian

- [Australia] Australia’s flying house prices – a catch-22? – EY

- [Croatia] The effect of housing loan subsidies on affordability: Evidence from Croatia – Journal of Housing Economics

- [Hong Kong] Hong Kong’s Lam to Target Housing Crisis in Policy Address – Bloomberg

- [Hong Kong] Carrie Lam policy address: massive housing plan near Hong Kong’s border to play starring role in speech, but vision has its critics. Blueprint calls for expanding on existing plan for New Territories North and will be comparable in scale with Lantau Tomorrow Vision, sources say. Proposal could make it easier for villagers to sell ancestral land, releasing abandoned farmland and earmarking funds to buy private holdings – South China Morning Post

- [Hong Kong] Hong Kong’s Massive Land Reform Unlikely to Tame Prices for Now – Bloomberg

- [Hong Kong] Hong Kong Developers Surge on Lam’s Northern Metropolis Plan – Bloomberg

- [New Zealand] New Zealand raises rates to rein in property prices and inflation worries. Central bank increases lending rate to 0.5% despite Covid lockdown in Auckland – FT

- [United Arab Emirates] Behind the Sizzle of Dubai Home Boom, Key Vulnerability Persists – Bloomberg

- [United Kingdom] Displaced: The Human Cost of London’s Housing Crunch. The story of Davida Dawkins shows how London’s push to build more affordable housing may still not be enough for its most vulnerable residents. – Bloomberg

On cross-country:

- City house prices outpace national markets. Predictions of ‘the death of the city’ now seem a distant memory as cities are now outpacing their national housing markets with prices rising by 9.8% on average in the year to Q2 2021. – Knight Frank

- Berliners Are Angry About Housing. And So Is Much of Europe. Soaring rents and out-of-reach prices have fueled property inequality – Bloomberg

- Sergei Gordeev: the Russian property tycoon betting on prefabricated blocks.

Posted by at 4:53 AM

Labels: Global Housing Watch

Subscribe to: Posts