Tuesday, October 12, 2021

House Prices and Consumer Price Inflation

From new work by IMF Colleagues (Nina Biljanovska, Chenxu Fu, and Deniz Igan):

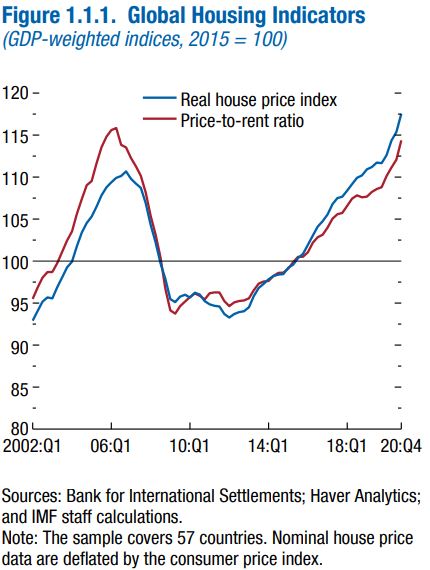

“Contrary to the expectation that house prices would decline during recessions (Igan and others 2011; Duca, Muellbauer, and Murphy, forthcoming), real house prices rose by 5.3 percent, on average, globally in 2020 as the pandemic-induced economic downturn took hold. Perhaps more strikingly, this was the highest annual growth rate observed in the past 15 years (Figure 1.1.1). While house price growth has breezed ahead, residential rents have grown at a slower rate, rising by 1.8 percent, on average, across countries over the same period.

Implications of a hot housing market for consumer prices

The house price surge comes at a time when questions are mounting over post-pandemic inflation dynamics (see Chapter 2). House prices matter for inflation because—through an asset pricing equation—they are linked to two measures of housing costs that could enter the CPI. One is the actual rent paid by tenants. The other is the imputed rent, or owner’s equivalent rent, which is an estimate of how much homeowners would need to pay were they to rent their own house. Overall, the rent component accounts, on average, for about 20 percent of the CPI.

How much of an increase in inflation is expected?“

Continue reading here.

Posted by at 2:14 PM

Labels: Global Housing Watch

Subscribe to: Posts