Thursday, September 16, 2021

Housing Market in Latvia

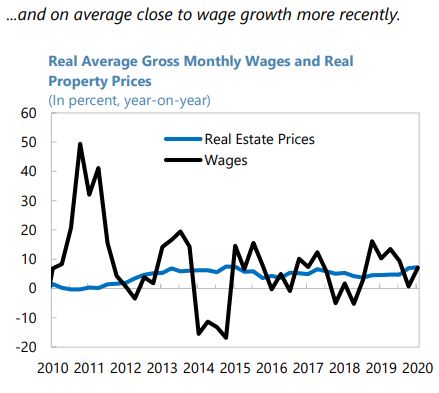

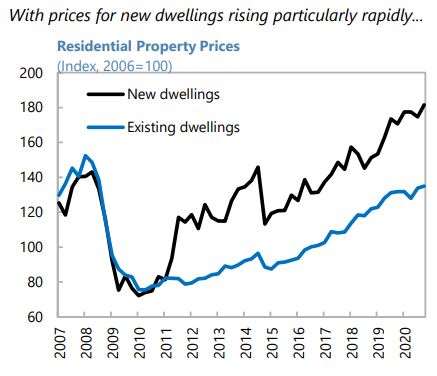

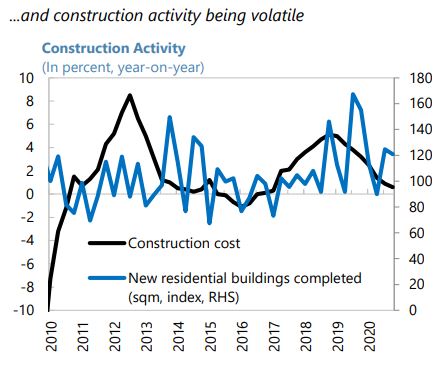

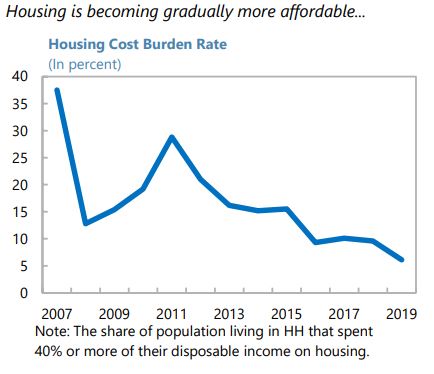

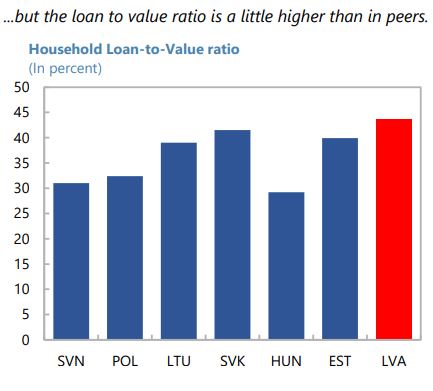

From the IMF’s latest report on Latvia:

“While real estate prices have been on a prolonged uptrend, robust wage growth and similar price dynamics in regional peers suggest that house prices remain broadly aligned with fundamentals. However, the expected surge in construction, backed by a large inflow of EU-investment funds, could renew overvaluation concerns in property prices.”

From the IMF’s latest report on Latvia:

“While real estate prices have been on a prolonged uptrend, robust wage growth and similar price dynamics in regional peers suggest that house prices remain broadly aligned with fundamentals. However, the expected surge in construction, backed by a large inflow of EU-investment funds, could renew overvaluation concerns in property prices.”

Posted by at 11:24 AM

Labels: Global Housing Watch

Housing Market in Croatia

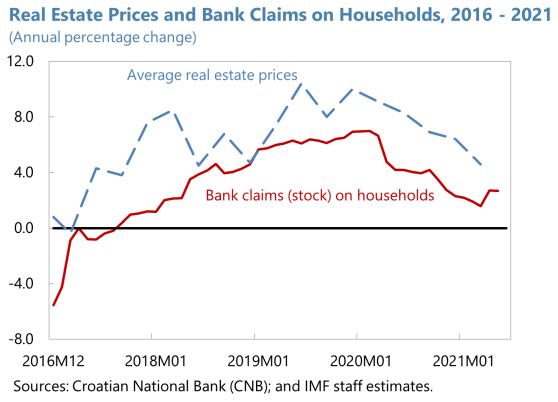

From the IMF’s latest report on Croatia:

“Housing loans remained strong during the pandemic. In 2020, about 10 percent of the households negotiated a debt-service moratorium. Most had expired by March 2021. Uncollateralized general-purpose cash loans declined. The increasing NPL ratio for these loans may be an opportunity to revisit some of the credit scoring models. Conversely, housing loans have continued to grow, underpinned by low interest rates, favorable taxation, and the support scheme for first time buyers.

The growth of real estate prices decelerated, and the number of transactions declined during the pandemic. The Airbnb markets in the capital area and on the coast proved relatively resilient. The CNB estimates that the composite real-estate price index is now slightly above what is warranted by fundamentals. The two earthquakes and increasing prices on construction materials have added to the cost pressures. Although some transactions are credit financed, others are driven by foreigners (mainly on the coast) and wealthy Croatians with higher savings. Still, if housing prices accelerate further beyond fundamentals, macroprudential measures should be considered. The current implicit debt-service-to-income (DSTI) ratio only refers of housing loans and cash loans with maturities of five years and longer. A formal DSTI should ideally cover all debt-service, including leasing. The strengthened macroprudential authority granted to the CNB and its new granular database should help both monitoring and calibration of possible borrower-based macro-prudential measures in the event of a credit-driven housing boom.”

From the IMF’s latest report on Croatia:

“Housing loans remained strong during the pandemic. In 2020, about 10 percent of the households negotiated a debt-service moratorium. Most had expired by March 2021. Uncollateralized general-purpose cash loans declined. The increasing NPL ratio for these loans may be an opportunity to revisit some of the credit scoring models. Conversely, housing loans have continued to grow, underpinned by low interest rates, favorable taxation, and the support scheme for first time buyers.

Posted by at 11:16 AM

Labels: Global Housing Watch

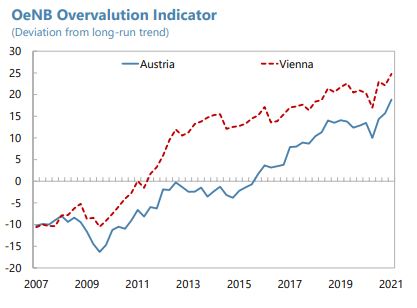

House Prices in Austria

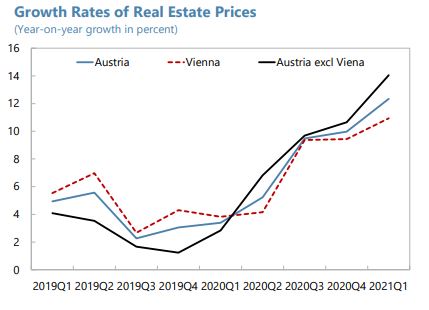

From the IMF’s latest report on Austria:

“Growing vulnerabilities in the housing sector call for a stricter enforcement of prudential guidelines. According to the OeNB analysis, house prices continue to decouple from fundamentals and a share of new lending does not comply with the sustainability recommendations by the Financial Market Stability Board (FMSB). Given the continued build-up of risks and to curtail further pressures on the housing market during the recovery phase, the authorities should make binding the existing prudential guidelines for lending. In addition, as vacant inventories in office and retail stores have increased during the crisis with the shift to tele-working and online sales, the rising vulnerabilities in the commercial real estate sector warrant close monitoring of banks’ real estate exposures. To this end, the current development of granular data on the commercial real estate (CRE) is a good step to allow a close monitoring of risks.”

From the IMF’s latest report on Austria:

“Growing vulnerabilities in the housing sector call for a stricter enforcement of prudential guidelines. According to the OeNB analysis, house prices continue to decouple from fundamentals and a share of new lending does not comply with the sustainability recommendations by the Financial Market Stability Board (FMSB). Given the continued build-up of risks and to curtail further pressures on the housing market during the recovery phase,

Posted by at 11:08 AM

Labels: Global Housing Watch

Housing Market in the US

From the IMF’s latest report on the US:

“The housing market appears to be on a vigorous upward path which could raise financial stability concerns in the event of a reversal. The rate of increase of house prices has tripled relative to before the pandemic, spurred by falling mortgage rates, robust growth in disposable income, and shifting housing preferences, also raising concerns about housing affordability and access to the housing market. However, mortgage debt has grown by a fairly modest amount (around 5 percent y/y) and lending has been concentrated in households with high credit scores. Furthermore, even for vulnerable households that were hit hardest by the pandemic, federal and private sector efforts to temporarily defer loan payments have provided important support and has resulted in a decline of mortgage delinquencies.”

From the IMF’s latest report on the US:

“The housing market appears to be on a vigorous upward path which could raise financial stability concerns in the event of a reversal. The rate of increase of house prices has tripled relative to before the pandemic, spurred by falling mortgage rates, robust growth in disposable income, and shifting housing preferences, also raising concerns about housing affordability and access to the housing market.

Posted by at 11:00 AM

Labels: Global Housing Watch

Subscribe to: Posts