Thursday, September 16, 2021

Housing Market in Croatia

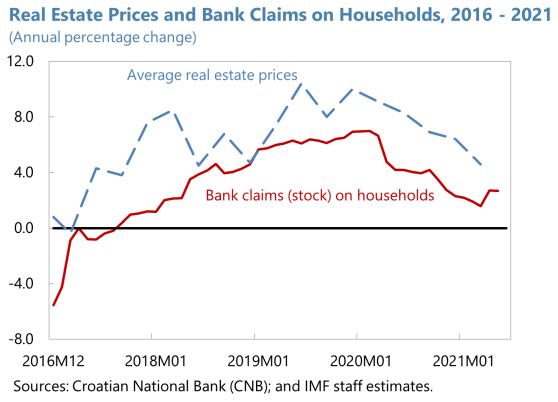

From the IMF’s latest report on Croatia:

“Housing loans remained strong during the pandemic. In 2020, about 10 percent of the households negotiated a debt-service moratorium. Most had expired by March 2021. Uncollateralized general-purpose cash loans declined. The increasing NPL ratio for these loans may be an opportunity to revisit some of the credit scoring models. Conversely, housing loans have continued to grow, underpinned by low interest rates, favorable taxation, and the support scheme for first time buyers.

The growth of real estate prices decelerated, and the number of transactions declined during the pandemic. The Airbnb markets in the capital area and on the coast proved relatively resilient. The CNB estimates that the composite real-estate price index is now slightly above what is warranted by fundamentals. The two earthquakes and increasing prices on construction materials have added to the cost pressures. Although some transactions are credit financed, others are driven by foreigners (mainly on the coast) and wealthy Croatians with higher savings. Still, if housing prices accelerate further beyond fundamentals, macroprudential measures should be considered. The current implicit debt-service-to-income (DSTI) ratio only refers of housing loans and cash loans with maturities of five years and longer. A formal DSTI should ideally cover all debt-service, including leasing. The strengthened macroprudential authority granted to the CNB and its new granular database should help both monitoring and calibration of possible borrower-based macro-prudential measures in the event of a credit-driven housing boom.”

Posted by at 11:16 AM

Labels: Global Housing Watch

Subscribe to: Posts