Tuesday, June 22, 2021

Housing Market in Switzerland

From the IMF’s latest report on Switzerland:

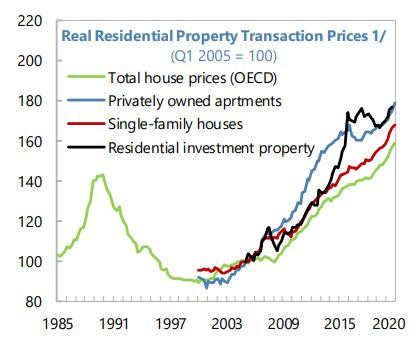

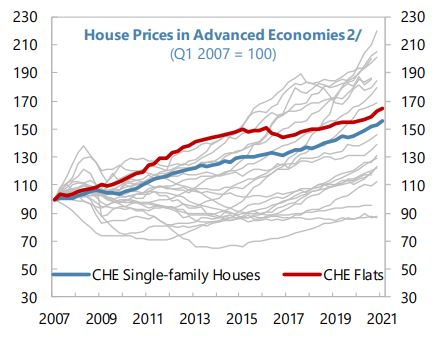

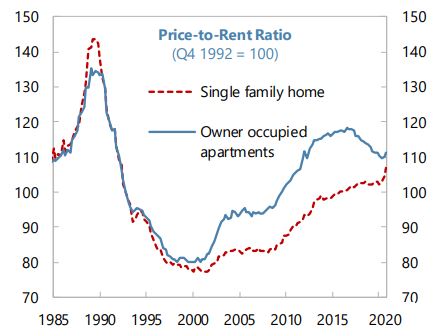

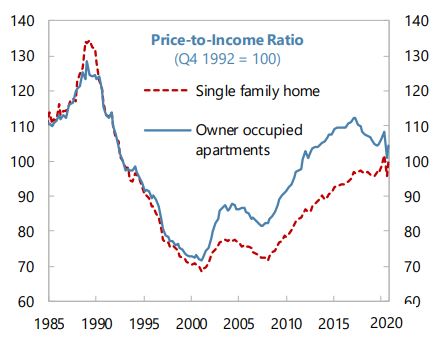

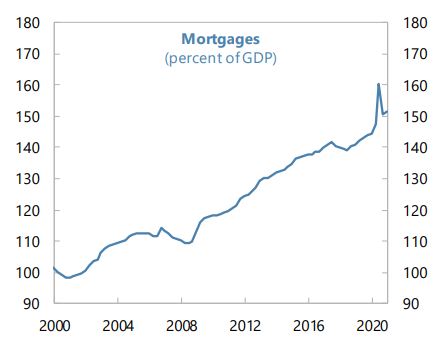

“Residential property prices have risen during the crisis, increasing affordability and imbalance concerns; commercial real estate faces risks from negative COVID-19 effects. Rising house prices have increased imbalances, especially among rentals, where vacancies are higher. A deterioration of affordability may take place when income support is withdrawn and should be monitored. Commercial real estate, especially outside core central business districts, also faces risks from negative pandemic effects and changes in occupancy, rents, and valuations. Voluntary self-regulation by financial institutions may face limits in terms of timeliness and stringency, and proactive measures (e.g., LTV or DTI restrictions) may be needed. The sectoral CCyB deactivation was appropriate, but should remain temporary, with buffers reset for potential real estate developments when conditions allow. Review of restrictions on housing supply in core urban areas and possible tax distortions may help identify measures to address imbalances.”

(…)

The authorities also see risks from real estate and search-for-yield behavior and are monitoring these carefully. They shared staff’s overall assessment and agreed that lagged effects of the COVID-19 crisis, real estate developments, and “lower-for-longer” pressures may have potentially important implications for financial stability. They will continue to monitor developments closely, as well as fintech and crypto activities. They highlighted progress made in implementing FSAP advice, especially on resources for FINMA, strengthening data collection and analysis, increasing risk-based on-site inspections, and improving recovery and resolution planning. They noted that the traditional approach of bank self-regulation in Switzerland has advantages—especially ownership—and stressed that self-regulatory measures may become binding and are augmented when needed. SNB and FINMA pointed to the effectiveness of new, stronger self-regulation on LTV ratios and faster amortization of mortgage loans for investment purposes from January 2020. Recent large market losses and risk controls are being closely examined. Smaller regional and cantonal banks have strong capital buffers and are prepared for further competitive pressures, including digitization. A solution is being sought for PostFinance.”

Posted by at 2:28 PM

Labels: Global Housing Watch

Subscribe to: Posts