Thursday, January 16, 2020

House prices in Finland

From the IMF’s latest report on Finland:

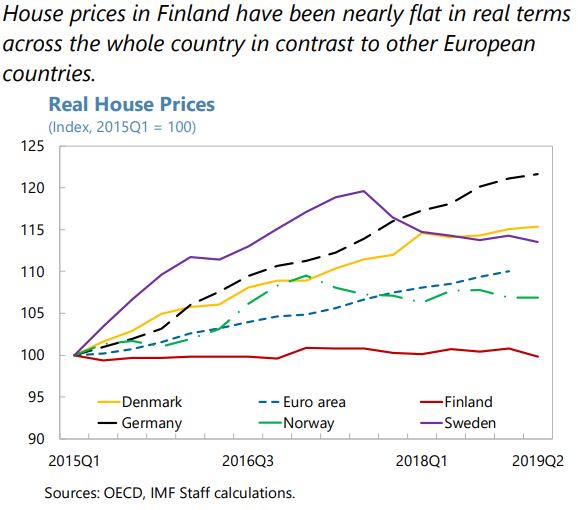

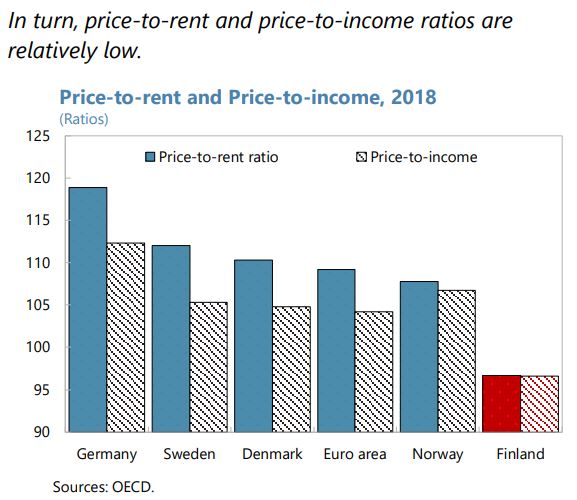

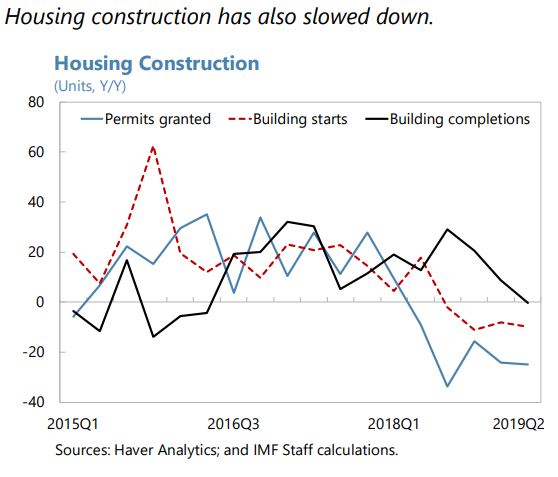

“Finnish banks are highly exposed to real estate, but residential and commercial real estate markets are not obviously overvalued. The exposure of domestic banks to real estate market has grown significantly over the last 20 years. The total volume of credit issued by domestic banks to the real-estate and construction sectors stood at 48.5 billion euros in 2018 (above 20 percent of GDP and 50 percent of banks’ receivables from firms and housing corporations), but rates of non-performing real estate loans remain low. In addition, real estate markets do not seem overheated overall, although there are differences across regions and market segments:

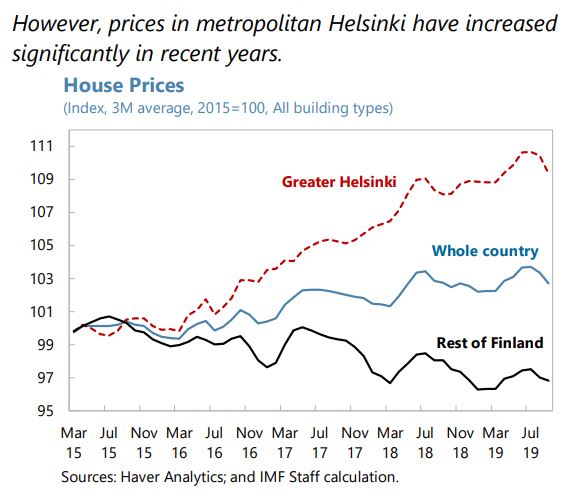

- Residential real estate prices have been nearly flat in real terms across the whole country, priceto-income and price-to-rent ratios are relatively low, and construction of new housing units seems to be slowing. However, housing prices in the Helsinki region have increased steadily while in most other parts of the country prices are falling (…).

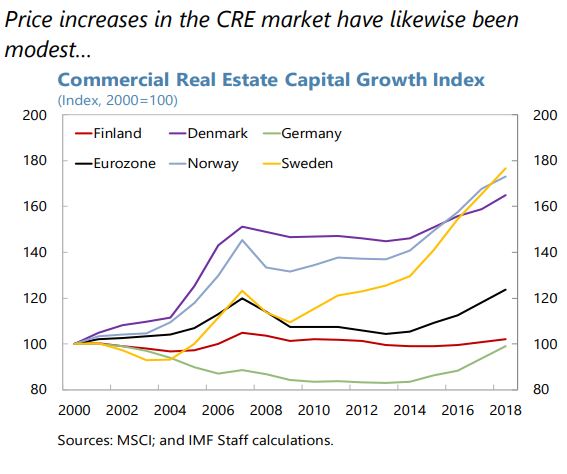

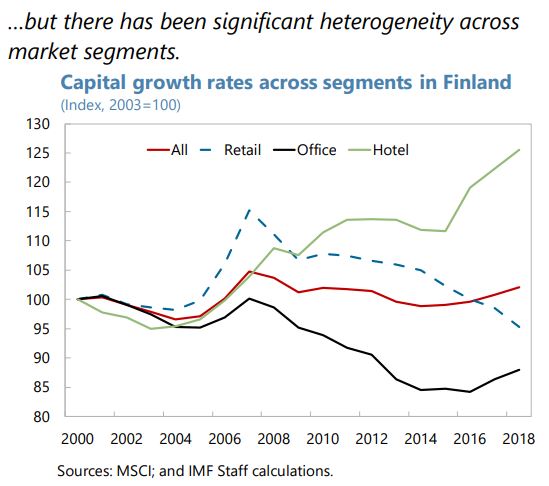

- Commercial real estate (CRE) valuations also do not appear stretched overall, but aggregate price dynamics mask significant differences across regions and submarkets. In the prime Helsinki office segment, limited supply means that rents are increasing, but they remain below the levels observed in other European capitals. By contrast, prices of retail properties have declined, given the brisk pace of growth in e-commerce and new supply in the Helsinki area. There are ongoing efforts to collect more data for a more precise assessment of CRE-related vulnerabilities in the financial sector, but data to monitor developments in CRE markets remain insufficient.

However, the increase and the composition of household debt create borrower-side vulnerabilities. While the debt-to-income ratio remains far below that of Denmark, Norway and Sweden, it has increased in recent years, driven by large annual increases in consumer credit and housing company loans. The share of highly indebted households is also elevated relative to levels observed in the past (although it has been stable in recent years). One concern is that financing the purchase of real estate through shares in a housing company masks risks to home owners and can make higher prices appear more affordable than they truly are.10 In addition, the majority of housing loans carry variable rates.

The authorities are taking steps to address these weaknesses. In particular, a government appointed working group has recommended a comprehensive cap on the debt-toincome (DTI) ratio, limits on the indebtedness of housing companies, and shortening the maximum maturity of mortgages and housing company loans. Crucially, the DTI limit would cover all borrower’s debts, including housing company loans. The working group proposes that the DTI limit be 450 percent; anticipating cases in which higher leverage could be affordable for some borrowers, it also proposes an exemption to allow banks a share of borrowers with higher debt ratios. These would be significant improvements and also in line with recent recommendations by the European Systemic Risk Board. The parliamentary discussions on these proposals are set to begin in 2020. In addition to the working group recommendations, an electronic registry of housing company shares is scheduled to be operational by the end of 2022. The registry will include full ownership information and will therefore make it easier to assess risks of investing in housing companies.”

From the IMF’s latest report on Finland:

“Finnish banks are highly exposed to real estate, but residential and commercial real estate markets are not obviously overvalued. The exposure of domestic banks to real estate market has grown significantly over the last 20 years. The total volume of credit issued by domestic banks to the real-estate and construction sectors stood at 48.5 billion euros in 2018 (above 20 percent of GDP and 50 percent of banks’ receivables from firms and housing corporations),

Posted by at 9:44 AM

Labels: Global Housing Watch

Wednesday, January 15, 2020

Central Banks and Climate Change

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies. However, the central bank should retain absolute discretion to interrupt any action if its first-priority objective – price stability – were to be compromised.”

“The big question, however, is whether central banks can use their monetary instruments to actively promote the fight against climate change (Honohan 2019). Over the last decade, central banks have significantly expanded their balance sheets, often by a factor of five or ten. In many countries, those balance sheets are now commensurate to the size of the national economy. With such an imprint on the economy and financial markets, central banks could take a more proactive approach to financing the climate transition.

Two possibilities come to mind, both without significant changes to the current operational framework:

- Reorient their asset purchases towards ‘green’ securities

- Modulate haircuts applied to different kinds of collateral used in refinancing operations, thus creating an incentive to detain some and offload others. “

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies.

Posted by at 1:25 PM

Labels: Energy & Climate Change

Tuesday, January 14, 2020

House Prices in Peru

From the IMF’s latest report on Peru:

Posted by at 1:48 PM

Labels: Global Housing Watch

Monday, January 13, 2020

Experts Confer on the State of the U.S. Rental Housing Market

Global Housing Watch Newsletter: January 2020

*Below is a conference summary prepared by Pedro Gete (IE Business School).

- The real estate market is poised for a favorable year even with an expected slowdown in the economy in 2020.

- Experts also pointed out the importance of population flows to understand recent housing dynamics, the need to rethink housing policy, and the strong effects that technology—such as Airbnb—is having on housing markets.

- Conference is part of the Federal Reserve Bank of St. Louis’ work in tracking developments in the U.S. housing market.

The Federal Reserve Bank of St. Louis hosted its first annual conference on December 5-6, 2019 on the U.S. rental housing markets. The conference was organized by Carlos Garriga and Don Schlagenhauf of the Federal Reserve Bank of St. Louis, and Pedro Gete from IE Business School. This conference brought together top experts to discuss current trends in the rental housing market alongside in-depth research to help understand the dynamics driving these markets and potential implications of policy decisions.

The view from the private sector and government agencies

The conference included Paul Liegey from the Bureau of Labor Statistics and participants from the private sector: Jeffrey Adler (Yardi Systems); Cris DeRitis (Moody’s); Mike Fratantoni (Mortgage Bankers Association); and Svenja Gudell (Zillow Group); Taylor Marr (Redfin); and Frank Nothaft (CoreLogic). What follows are the key takeaways from these participants:

- The overall outlook for the U.S. economy remains favorable. Most panelists projected slower economic growth in 2020, with real GDP growth between 2 percent and 2.5 percent. Only one forecast had real GDP growth slightly under 1 percent. Comments suggested the recent interest rate cuts by the Fed would cushion a slowdown from turning to a recession.

- Panelists generally agreed that the real estate market was poised for a favorable year even with a slowdown in the economy, as demographics should produce growth in household formation which would generate steady demand for home purchases. Panelists also agreed that the supply of homes to be added in 2020 is unlikely to meet new demand, effectively pushing up prices and reducing affordability for first-time buyers.

- While the demographics are favorable to increasing home sales in 2020, the continued lack of supply and higher prices are likely to keep many potential first-time buyers in the rental market, keeping the demand for rental units stable to increasing. Panelists noted, however, drivers of demand for multifamily units varied across the county: in large (high-cost) coastal cities, demand has been driven by international migration; in mid-size cities in the West, Texas, and South, demand has been driven by domestic migration.

- Panelists offered various hypotheses for the lack of supply for new housing units (both owner-occupied and rental). Panelists noted that anecdotally labor shortages are often cited for containing building. However, economic data suggest the labor reason may be over-emphasized: while total employment growth has been slow, average wage growth for construction workers has slowed, which suggests lower demand for these positions. Among others, alternative hypotheses offered by panelists included: longer time to completion on new construction; a lack of available lots; desire to age in place by older generations; and a large future supply of homes over next 20 years due to the passing of baby boomers.

The view from policymakers and academics

The conference also included participants from the central banks and academia. What follows are the key takeaways from this group.

- Housing Supply and Affordability, presented by Raven Molloy (Federal Reserve Board). Coauthors: Charles G. Nathanson (Northwestern University) and Andrew Paciorek (Federal Reserve Board). The authors develop a model to understand how housing supply constraints affect housing affordability. The model predicts that supply constraints will increase the price of housing services (or rents) by only about half as much as the house purchase price. This is because purchase prices reflect current rents as well as future increases in rents. Using metro-area data, the authors find sizeable effects of supply constraints on house prices, but little effect on rent, house/lot size, location, or housing expenditures. The authors conclude that housing supply constraints distort housing consumption and affordability much less than their estimated effects on house prices would suggest.

- Landlord rights, Evictions, and Rent Affordability, presented by Thao Le (Georgia State University). Coauthors: N. Edward Coulson (University of California) Irvine and Lily Shen (Clemson University). The authors develop a search model to understand the effect of eviction cost on rent affordability. The model predicts that a lower eviction cost will lead to lower rent, higher supply, a higher vacancy rate, a lower homeless rate, and a potentially higher eviction rate. Using data, the authors confirm the model predictions. In areas where landlords have stronger rights, rental houses are more affordable, and the vacancy rate is higher. The results highlight a delicate balance between strict regulations, eviction and rent affordability.

- Affordable Housings and City Welfare, presented by Pierre Mabille (New York University). Coauthors: Jack Favilukis (University of British Columbia) and Stijn Van Nieuwerburgh (Columbia University). The authors evaluate the effect of affordable housing policies (zoning changes, rent control, housing vouchers, and tax credits) on the well-being of citizens. Using a model calibrated to the New York, MSA, they find that housing affordability policies carry substantial insurance value but cause misallocation in labor and housing markets. For example, increasing the housing stock in the urban core by relaxing zoning regulations is welfare improving. Contrary to conventional wisdom, increasing the generosity of the affordable housing or housing voucher systems is also welfare improving. Increasing the housing safety net for the poorest households creates welfare gains for society. How the affordability policies are financed has first-order effects on welfare gains.

- The Price-Rent Ratio during the Boom and Bust, presented by Paul Willen (Federal Reserve Bank of Boston). Coauthors: Jaclene Begley (Fannie Mae) and Lara Loewenstein (Federal Reserve Bank of Cleveland). They decompose the change in the price of occupant-owned property into three components: (1) changes in rent; (2) changes in the relative price of investor-and occupant-owned property; and (3) changes in the price-rent ratio. They show that changes in the price-rent ratio accounts for most of the variation and argue that this has significant implications for theories of the 2000s housing boom and bust.

- The Effect of Home-Sharing on House Prices and Rents: Evidence from Airbnb, presented by Davide Proserpio (University of Southern California). Coauthors: Kyle Barron (NBER) and Edward Kung (UCLA). The authors find that 1 percent increase in Airbnb listings is causally associated with a 0.018 percent increase in rental rates and 0.026 percent increase in house prices. Considering the rapid growth in Airbnb, this accounts for about one-fifth of the average annual increase in national rents, and one-seventh of the average annual increase in housing prices. While this is an important factor, demographic changes across cities zip codes can explain three-fourths of the differences in rent and housing price growth.

- Why is the rent so darn high? Presented by Greg Howard (University of Illinois). Coauthor: Jack Liebersohn (Ohio State University). Rents are high because of migration. The authors show that three-quarters of the CPI-rent increase in the United States from 2000 to 2018 is due to increased demand to live in ex-ante housing-supply-inelastic cities (that is, cities where is it difficult to build new housing). The authors also show that despite low short-run migration rates, people have high long-run mobility. Moreover, the pattern of migration across cities matches the patterns in labor-market and amenity changes.

From left to right: Carlos Garriga (Federal Reserve Bank of St. Louis), Frank Nothaft (CoreLogic), Taylor Marr (Redfin), Svenja Gudell (Zillow Group), and Mike Fratantoni (Mortgage Bankers Association).

From left to right: Randal Verbrugge (Federal Reserve Bank of Cleveland), Paul Liegey (Bureau of Labor Statistics), Jeffrey Adler (Yardi Systems) and Cris DeRitis (Moody’s).

Global Housing Watch Newsletter: January 2020

*Below is a conference summary prepared by Pedro Gete (IE Business School).

- The real estate market is poised for a favorable year even with an expected slowdown in the economy in 2020.

- Experts also pointed out the importance of population flows to understand recent housing dynamics, the need to rethink housing policy,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, January 10, 2020

Housing View – January 10, 2020

On cross-country:

- Asset Bubbles and Global Imbalances – Federal Reserve Bank of Richmond

On the US:

- Dominating Firms Can Depress House Prices as Well as Wages – Wall Street Journal

- Experts predict what the 2020 housing market will bring – Washington Post

- Trump Administration Plans Roll Back of Low-Income Housing Rules – Wall Street Journal

- Our cities don’t have enough affordable housing. Changing this policy will help – CNN

- New Trump Administration Regulations Say That Affordable Housing Is Fair Housing – Reason

- AEI Housing Market Indicators release on September 2019 data – American Enterprise Institute

- Pricey California Targeted in New Effort for Housing Density – Bloomberg

- Home Purchase Sentiment Index Caps Off Strong 2019 Near Its Survey High – Fannie Mae

- How Wealthy Towns Keep People With Housing Vouchers Out – ProPublica

- Opinion: Unintended consequences: How ‘green’ regulations exacerbate the housing crisis – Market Watch

- As Trump Ditches a Fair Housing Rule, New York City Doubles Down – Citylab

- California Governor Pushes $1.4 Billion Plan To Tackle Homelessness – NPR

- Why The Most Favorable Markets for Tech Expansion Aren’t Where You Might Think – Zillow

On other countries:

- [Brazil] Brazil’s house prices keep falling – Global Property Guide

- [Canada] Canada’s house price boom takes off – Global Property Guide

- [United Kingdom] London house prices link to earnings is ‘almost entirely dislocated’ – Financial Times

- [United Kingdom] UK house price affordability worsens over past decade – Financial Times

On cross-country:

- Asset Bubbles and Global Imbalances – Federal Reserve Bank of Richmond

On the US:

- Dominating Firms Can Depress House Prices as Well as Wages – Wall Street Journal

- Experts predict what the 2020 housing market will bring – Washington Post

- Trump Administration Plans Roll Back of Low-Income Housing Rules – Wall Street Journal

- Our cities don’t have enough affordable housing.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts