Tuesday, January 21, 2020

International Effects of Stock Market Dispersion

From a new paper on the effects of stock market dispersion:

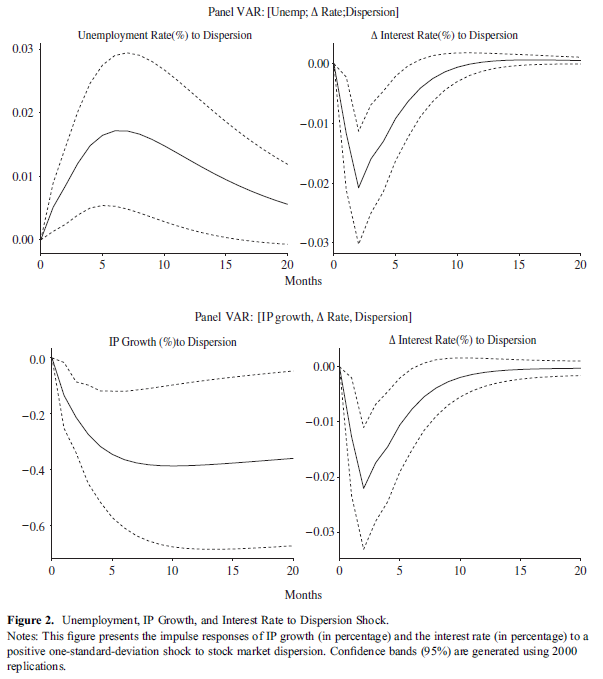

“We study the extent to which stock market dispersion is related to unemployment and output growth for 16 countries over 20 years. Using panel vector-auto-regressions and panel dynamic regressions, we find increases in stock market dispersion across industries to induce future increases in unemployment and

future decreases in industrial production (IP) growth. Moreover, the responses of unemployment and IP growth following a positive shock to stock market dispersion are persistent and are robust to various controls, sample periods, and estimation methods. Our article provides cross-country evidence in support of the hypothesis that shifts in demand across industries negatively affect employment.”

“We present the impulse responses of the unemployment rate and the change in the interest rate to a positive one-standard-deviation shock to stock market dispersion in the upper subfigure of Figure 2. […] Overall, we find an increase in stock market dispersion to have a negative impact on the labor market in the short term, as evidenced by the positive response of the unemployment rate. Specifically, the unemployment rate increases by 0.02% following a positive one-standard-deviation shock to stock market dispersion. This increase peaks after the seventh month and gradually fades away after 15–20 months. Despite its modest magnitude at peak (0.02%), the impact of stock market dispersion on the unemployment rate is relatively long-lived, with the responses lasting beyond the 20-month horizon. Our result is consistent with previous studies that use U.S. data (e.g., Loungani, Rush, and Tave 1990, and more recently Angelidis, Sakkas, and Tessaromatis 2015) in the sense that unemployment significantly depends on the lags of stock market dispersion.”

From a new paper on the effects of stock market dispersion:

“We study the extent to which stock market dispersion is related to unemployment and output growth for 16 countries over 20 years. Using panel vector-auto-regressions and panel dynamic regressions, we find increases in stock market dispersion across industries to induce future increases in unemployment and

future decreases in industrial production (IP) growth. Moreover, the responses of unemployment and IP growth following a positive shock to stock market dispersion are persistent and are robust to various controls,

Posted by at 10:00 AM

Labels: Inclusive Growth

The (Subjective) Well-Being Cost of Fiscal Policy Shocks

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition, we show that accompanying monetary and exchange rate policies (disinflation, depreciations and the liberalization of capital flows) mitigate the well-being cost of fiscal consolidations. Finally, we investigate the well-being consequences of the two well-knowns expansionary fiscal consolidations episodes taking place in the 80s (in Denmark and Ireland). We find that even expansionary fiscal consolidations can have well-being costs. Our results may therefore shed some light on why some governments may choose to consolidate through taxes even at the cost of economic growth. Indeed, if spending cuts are to generate a large well-being loss, they can trigger an opposition and protest against a fiscal consolidation plan and hence making it politically costly.”

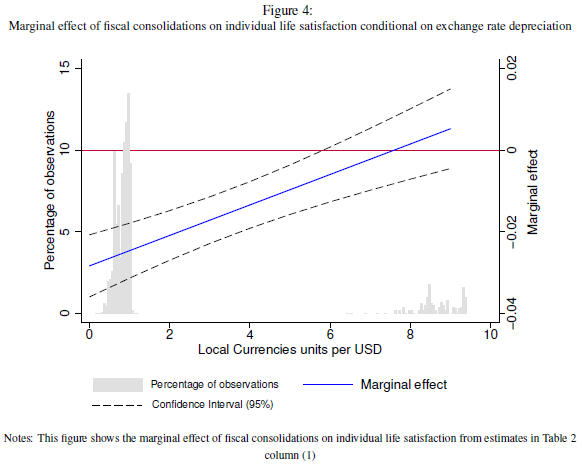

“Figure 4 depicts the effect of a 1 percentage point of GDP increase in the size of a fiscal consolidation conditional on being accompanied by different level of depreciation in the sample. Figure 4 shows that for higher levels of depreciation, that is for ratios of at least 6 units of local currencies per USD, fiscal consolidations do not have any statistically significant effect on well-being.”

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition,

Posted by at 9:55 AM

Labels: Inclusive Growth

Friday, January 17, 2020

Predicting Downside Risks to House Prices and Macro-Financial Stability

From an IMF working paper by Andrea Deghi, Mitsuru Katagiri, Sohaib Shahid, and Nico Valckx:

“This paper predicts downside risks to future real house price growth (house-prices-at-risk or HaR) in 32 advanced and emerging market economies. Through a macro-model and predictive quantile regressions, we show that current house price overvaluation, excessive credit growth, and tighter financial conditions jointly forecast higher house-prices-at-risk up to three years ahead. House-prices-at-risk help predict future growth at-risk and financial crises. We also investigate and propose policy solutions for preventing the identified risks. We find that overall, a tightening of macroprudential policy is the most effective at curbing downside risks to house prices, whereas a loosening of conventional monetary policy reduces downside risks only in advanced economies and only in the short-term.”

From an IMF working paper by Andrea Deghi, Mitsuru Katagiri, Sohaib Shahid, and Nico Valckx:

“This paper predicts downside risks to future real house price growth (house-prices-at-risk or HaR) in 32 advanced and emerging market economies. Through a macro-model and predictive quantile regressions, we show that current house price overvaluation, excessive credit growth, and tighter financial conditions jointly forecast higher house-prices-at-risk up to three years ahead. House-prices-at-risk help predict future growth at-risk and financial crises.

Posted by at 5:37 PM

Labels: Global Housing Watch

Finance and Inequality

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

At the same time, we observe rising or high disparities in income and wealth within many countries. New data also show that economic mobility—the ability of the less well-off to improve their economic status—has stalled in recent decades. No wonder then that inequality of income, wealth, and opportunities is giving rise to populism and anti-globalization sentiments in some countries.

Can the financial sector play a role in reducing inequality? This study makes the case that it can, complementing redistributive fiscal policy in mitigating inequality. By expanding the provision of financial services to low-income households and small businesses, it can serve as a powerful lever in helping create a more inclusive society but—if not well managed—it can also amplify inequalities.

Our study examines empirical relationships between income inequality and three features of finance: depth (financial sector size relative to the economy), inclusion (access to and use of financial services by individuals and firms), and stability (absence of financial distress). We ask three questions.

First, does greater financial depth mean lower or higher inequality within countries? Building on new data sets, our analysis suggests that initially financial depth is associated with lower inequality, but only up to a point, after which inequality rises.

Second, does greater financial inclusion mean lower inequality within countries? We find that greater financial inclusion is associated with reductions in inequality. For payment services, we find evidence that benefits from inclusion are greater for those at the low end of the income distribution, reducing inequality. Both men and women benefit from financial inclusion, but inequality falls more when women have greater access. As regards access to and use of credit, the results are mixed.

Third, is there a relationship between stability and inequality within countries? Our study finds that higher inequality is associated with greater financial risks. Increases in inequality tend to be accompanied by higher growth in credit. For example, in the United States, too much credit, including to lower-income households, contributed to the 2008 crisis. Crises, in turn, lead to higher default rates, making lower-income households worse off and increasing inequality after a crisis.

Our key takeaway is that finance can help reduce inequality but is also associated with greater inequality if the financial system is not well managed. Our findings have five policy implications. First, financial inclusion policies help reduce inequality. Second, there is a case for promoting women’s financial inclusion, as inequality falls even more when policies are inclusive of women. Third, regulatory policies have a role to play in reining in excessive growth of the financial sector. Fourth, provided quality of regulation and supervision is high, financial inclusion and stability can be pursued simultaneously. Fifth, financial sector policies are a complement, not a substitute, for other policy tools—fiscal and macro-structural policies are still needed to help address inequality.”

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

Posted by at 10:58 AM

Labels: Inclusive Growth

Housing View – January 17, 2020

On cross-country:

- Home ownership is the West’s biggest economic-policy mistake – Its obsession with home ownership undermines growth, fairness and public faith in capitalism – The Economist

- Housing is at the root of many of the rich world’s problems – Since the second world war, governments across the rich world have made three big mistakes, says Callum Williams – The Economist

- How housing became the world’s biggest asset class – It is only a recent phenomenon – The Economist

- Politicians are finally doing something about housing shortages. But will it reduce housing costs? – The Economist

- A decade on from the housing crash, new risks are emerging. Shadow banks originate around half America’s mortgages – The Economist

- Owner-occupation is not always a better deal than renting. Each year American owner-occupiers pay around $200bn in maintenance costs on their homes – The Economist

- Home ownership is in decline. That is not a big cause for concern – The Economist

- Governments are rethinking the provision of public housing. Is it better to give people money or build them houses? – The Economist

- What is the future of the rich world’s housing markets? It is plausible that house prices could persistently rise faster than incomes – The Economist

- Global Residential Cities Index – Q3 2019 – Knight Frank

- Around the world, luxury housing is poised to (mostly) strengthen – Los Angeles Times

On the US:

- Capital Income Taxation with Housing – Federal Reserve Bank of Philadelphia

- Affordable housing is in crisis. Is public housing the solution? – Curbed

- What Would It Take to End Homelessness? – Los Angeles Times

- Would Capping Office Space Ease San Francisco’s Housing Crunch? – Citylab

- A Perverse Way To “Solve” California’s Housing Crisis: People Are Leaving The Golden State – Hoover Institution

On other countries:

- [Hong Kong] Hong Kong’s house prices falling – Global Property Guide

- [Indonesia] The housing market in Indonesia rarely makes big moves – Global Property Guide

- [Ireland] Cash offers may lead mortgage customers to make poor decisions – ESRI – The Irish Times

- [Macau] Macau’s housing market slowing sharply – Global Property Guide

- [Netherlands] Amsterdam’s Attempt to Rein In Property Prices Just Got Harder – Bloomberg

- [South Korea] South Korea’s Moon Vows ‘Endless’ Measures to Cap Property Prices – Bloomberg

- [Switzerland] House prices in Switzerland continue to drop – Global Property Guide

- [United Kingdom] Cambridge tech boom blamed for rising property prices – Financial Times

On cross-country:

- Home ownership is the West’s biggest economic-policy mistake – Its obsession with home ownership undermines growth, fairness and public faith in capitalism – The Economist

- Housing is at the root of many of the rich world’s problems – Since the second world war, governments across the rich world have made three big mistakes, says Callum Williams – The Economist

- How housing became the world’s biggest asset class –

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts