Wednesday, April 10, 2019

Rethinking the Phillips Curve: Inflation May Rise Modestly Next Year

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high. In a new paper, however, we show that the relationship between inflation and unemployment has shifted twice—in the late 1960s and in the mid-1990s. The paper replicates the findings of some other researchers, who find a very flat Phillips curve since the 1990s, implying that unemployment has little effect on inflation. But we also propose an alternative hypothesis: The Phillips curve is bent when inflation is low so that high unemployment has little downward effect on inflation, but low unemployment still pushes inflation up. If we are right, inflation is likely to rise modestly over the next couple of years. We will explore what this means for monetary policy in a subsequent post.

THE EVOLVING US PHILLIPS CURVE

Alban Phillips (1958) developed the original curve bearing his name. It related the rate of wage inflation to the unemployment rate in the United Kingdom over the period 1861–1913. Olivier Blanchard (2017, chapter 8) showed that a similar downward-sloping curve in terms of price inflation and unemployment was apparent in the United States in 1900–1960. Our paper confirms Blanchard’s finding that the rising inflation of the late 1960s led to the unmooring of expectations of inflation from the stable low levels that had prevailed before then and a shift in the Phillips curve to a relationship between the change in the rate of inflation and the unemployment rate. The return of inflation to a very low and stable level led to a second shift in the Phillips curve in the mid-1990s, back to a relationship between the level of inflation and the unemployment rate.

In addition to this shift in the persistence of inflation, many researchers have found that the Phillips curve has been very flat since the 1990s, so that changes in unemployment have little effect on inflation. This was most dramatically demonstrated in the aftermath of the Great Recession of 2008–09, when unemployment remained very high for years and yet inflation barely dipped. We show, however, that another hypothesis fits the data equally well: The Phillips curve may become bent when inflation is low, with a flat portion for high unemployment and a steeper portion for low unemployment.”

Continue reading here.

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high.

Posted by at 8:55 AM

Labels: Macro Demystified

Tuesday, April 9, 2019

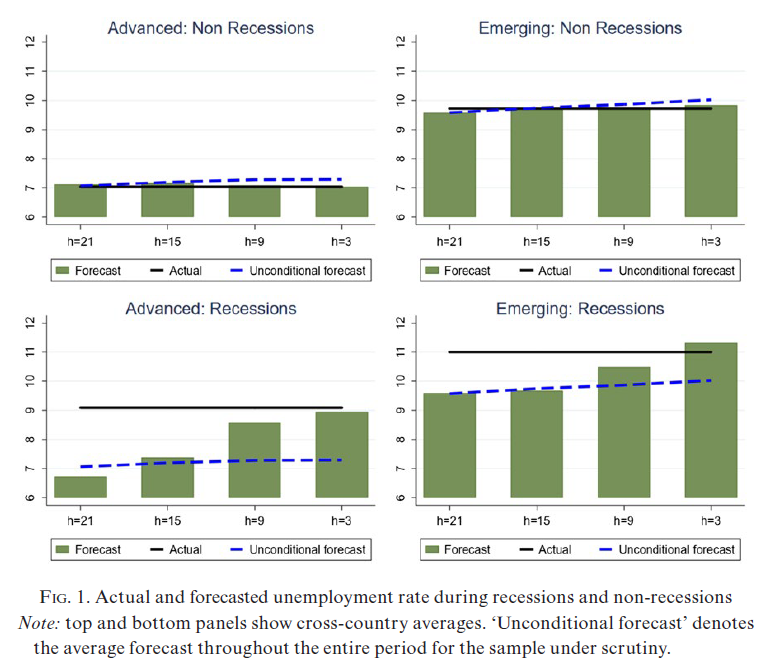

An Assessment of the IMF’s Unemployment Forecasts

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns. Forecasts are characterized by inefficiency (errors of the past are repeated in the present) and rigidity (forecast revisions are serially correlated). There is little to choose between IMF and Consensus Forecasts, a source of private sector forecasts, for the small subset of 12 countries for which both sets of forecasts are available.”

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns.

Posted by at 10:45 PM

Labels: Forecasting Forum

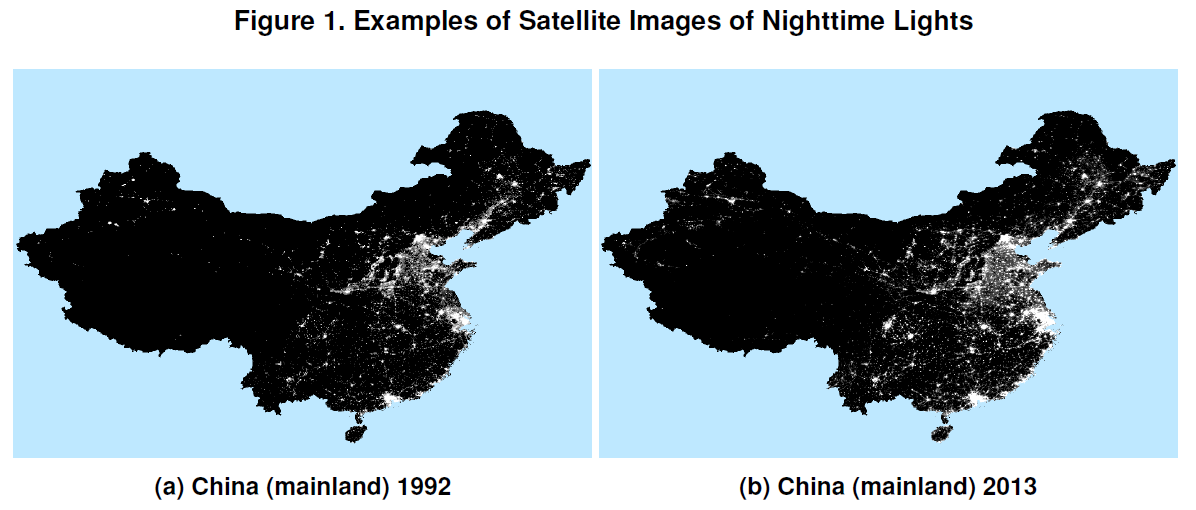

Illuminating Economic Growth

From a new IMF working paper:

“In this paper, we show that nighttime lights can be a useful source of information to improve official real GDP data. To begin with, they can be used to detect the uncertainty in official data and potential mismeasurement of real GDP. Systematic differences between the new and official measures may warrant further investigation as to what contributes to such differences. While nighttime lights can be computationally intensive to process, the method developed in this paper is not limited to nighttime lights. In fact, measures of real GDP that are conditionally independent of official data can be used in a similar fashion.”

“Figure 1 compares satellite images of nighttime lights for mainland China, […] Variation in nighttime lights may thus contain useful information on China’s real economic growth.”

Continue reading here.

From a new IMF working paper:

“In this paper, we show that nighttime lights can be a useful source of information to improve official real GDP data. To begin with, they can be used to detect the uncertainty in official data and potential mismeasurement of real GDP. Systematic differences between the new and official measures may warrant further investigation as to what contributes to such differences. While nighttime lights can be computationally intensive to process,

Posted by at 10:41 PM

Labels: Inclusive Growth

Subjective Models of the Macroeconomy: Evidence From Experts and a Representative Sample

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence, there is strong heterogeneity in the predictions in the representative panel. While households predict changes in unemployment that are qualitatively in line with the experts for all four shocks, their predictions of changes in inflation are at odds with those of experts both for the tax shock and the interest rate shock. People’s beliefs about the micro mechanisms through which the different macroeconomic shocks are propagated in the economy strongly affect how aligned their predictions are with those of the experts. More educated and older respondents form their expectations more in line with experts, consistent with roles for cognitive limitations and learning over the life-cycle. Our findings inform the validity of central assumptions about the expectation formation process and have important implications for the optimal design of fiscal and monetary policy.”

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence,

Posted by at 10:33 PM

Labels: Forecasting Forum

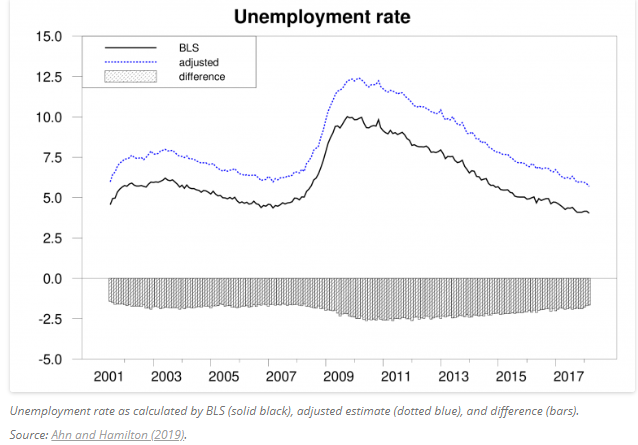

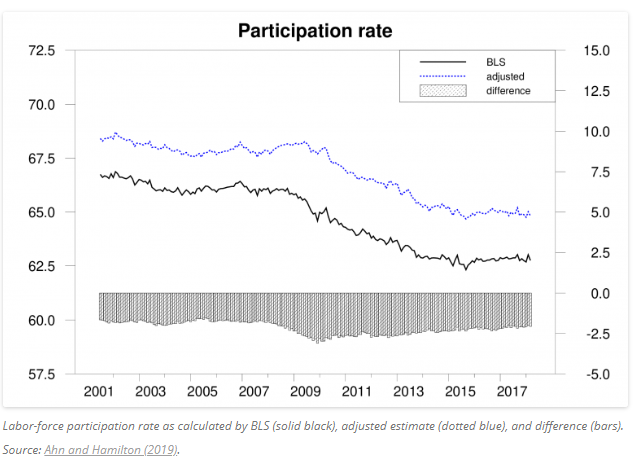

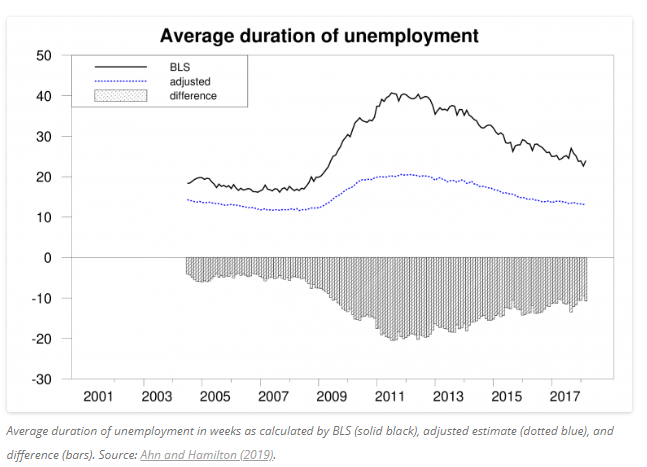

Measuring unemployment and labor-force participation

From a new Econbrowser by Hie Joo Ahn and James D. Hamilton:

“We conclude that the true unemployment rate in the U.S. is 1.9% higher on average than the published estimates.”

“We also conclude that the Bureau of Labor Statistics has underestimated the labor-force participation rate by 2.2% on average and that the fall in participation has been slower than suggested by the BLS estimates.”

“On the other hand, we find that reported average unemployment durations significantly overstate the average length of an uninterrupted spell of unemployment. A big factor in this appears to be the fact noticed by Kudlyak and Lange (2018) that some individuals include periods when they were briefly employed but nonetheless looking for a better job when they give an answer to how many weeks they have been actively looking for a job.”

“Here is our paper’s conclusion:

The data underlying the CPS contain multiple internal inconsistencies. These include the facts that people’s answers change the more times they are asked the same question, stock estimates are inconsistent with flow estimates, missing observations are not random, reported unemployment durations are inconsistent with reported labor-force histories, and people prefer to report some numbers over others. Ours is the first paper to attempt a unified reconciliation of these issues. We conclude that the U.S. unemployment rate and labor-force continuation rates are higher than conventionally reported while the average duration of unemployment is considerably lower.”

From a new Econbrowser by Hie Joo Ahn and James D. Hamilton:

“We conclude that the true unemployment rate in the U.S. is 1.9% higher on average than the published estimates.”

“We also conclude that the Bureau of Labor Statistics has underestimated the labor-force participation rate by 2.2% on average and that the fall in participation has been slower than suggested by the BLS estimates.”

Posted by at 10:28 PM

Labels: Inclusive Growth

Subscribe to: Posts