Wednesday, June 12, 2019

House Prices in Norway

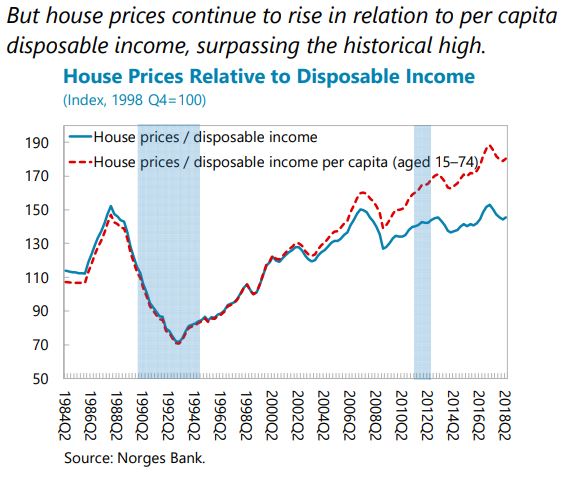

From the IMF’s latest report on Norway:

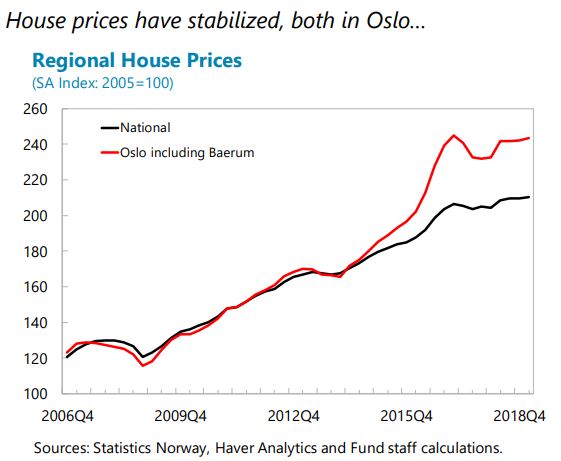

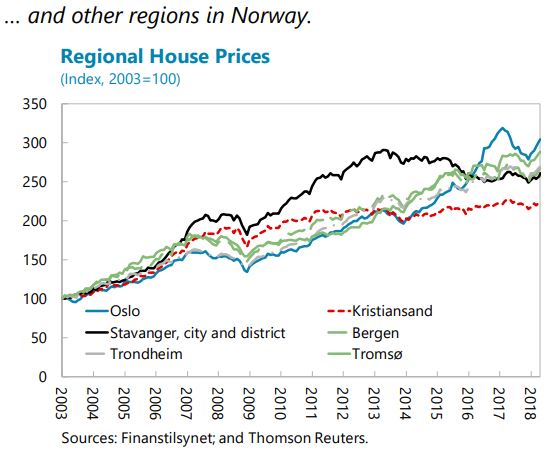

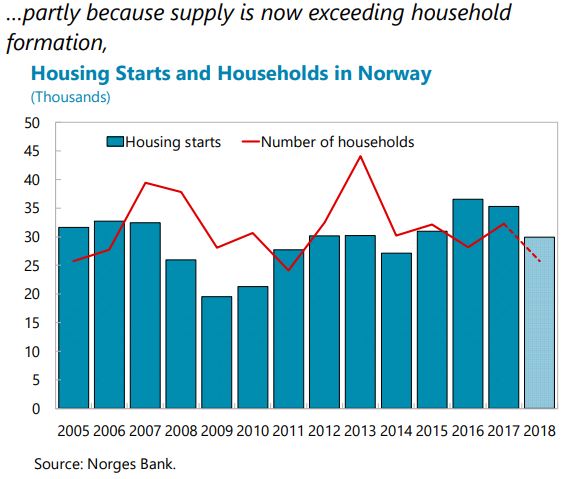

- “House prices remain overvalued, albeit less so than last year, and household debt continues to rise from an already elevated level (…). The house price moderation discussed earlier has improved housing affordability and correspondingly lowered the risks of a price crash. Nevertheless, house prices remain above fundamentals per staff estimates (0–10 percent at the national level and 5–20 percent in Oslo). Moreover, household indebtedness continues to increase from already high levels, leaving households vulnerable to sharp interest rate rises. Besides mortgages, the rapid growth of consumer credit also warrants close watch, even if it starts from a small base.

- Risks from commercial real estate are rising (…). Commercial real estate prices have increased by about 60 percent since 2000 in real terms, and more than twice that in prime Oslo. Although yields in Norway are not especially low, Oslo’s prime market has the lowest yield compression among major European cities. Banks have substantial exposure to CRE loans25 which account for 15 percent of banks’ loan portfolio (23 percent of GDP), higher than peer countries.”

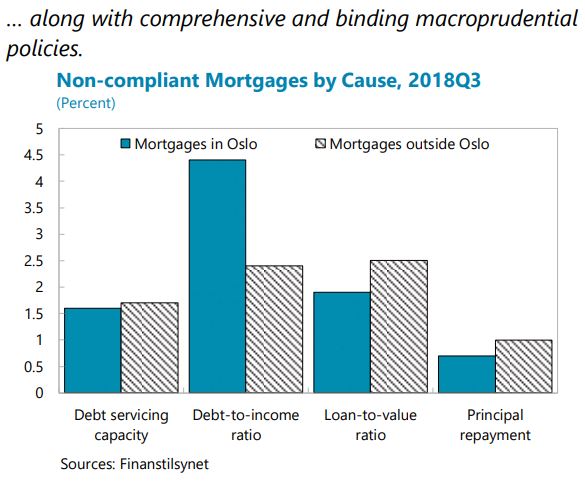

- The current prudential toolkit to mitigate financial stability risks is quite comprehensive and should not be loosened at this stage.

Residential housing: The current mortgage regulations, renewed last year, consist of both capital and borrower-based measures such as maximum LTV and DTI ratios, and are welltargeted to areas with higher risks such as Oslo. Together, they have contributed to containing the incidence of risky mortgages, not least in the capital. Given that prices are still overvalued, and that household debt continues to rise, the regulations should be extended as is when reviewed at year-end, barring large unexpected developments in the coming months. The tighter limits for Oslo should be preserved. As recommended in previous years, the mortgage regulations could also be made permanent; the parameters could then be adjusted as needed over the financial cycle.”

From the IMF’s latest report on Norway:

- “House prices remain overvalued, albeit less so than last year, and household debt continues to rise from an already elevated level (…). The house price moderation discussed earlier has improved housing affordability and correspondingly lowered the risks of a price crash. Nevertheless, house prices remain above fundamentals per staff estimates (0–10 percent at the national level and 5–20 percent in Oslo). Moreover, household indebtedness continues to increase from already high levels,

Posted by at 2:22 PM

Labels: Global Housing Watch

RIP Marty Feldstein

Marty Feldstein passed away at the age of 79. He was the first person I wrote a profile of when I joined the IMF’s public relations department in the 2000s. He was very pleasant and very patient during the interview, but got irritated when the photographer asked him to remove his glasses for the photograph. “The glasses stay on,” he said firmly. See the photograph and read my profile of Marty.

Marty Feldstein passed away at the age of 79. He was the first person I wrote a profile of when I joined the IMF’s public relations department in the 2000s. He was very pleasant and very patient during the interview, but got irritated when the photographer asked him to remove his glasses for the photograph. “The glasses stay on,” he said firmly. See the photograph and read my profile of Marty.

Posted by at 9:50 AM

Labels: Profiles of Economists

Tuesday, June 11, 2019

IMF’s Ian Parry receives the IAEE’s 2019 annual prize for outstanding contributions to the field

The International Association for Energy Economics (IAEE) has awarded Ian Parry (IMF) the 2019 annual prize for outstanding contributions to the field of energy economics and its literature.

Ian Parry is Principal Environmental Fiscal Policy Expert in the IMF’s Fiscal Affairs Department, specializing in fiscal analysis of climate change, environment, and energy issues. Before joining the Fund in 2010, Ian held the Allen V. Kneese Chair in Environmental Economics at Resources for the Future. Below are some of latest posts by Ian Parry.

The International Association for Energy Economics (IAEE) has awarded Ian Parry (IMF) the 2019 annual prize for outstanding contributions to the field of energy economics and its literature.

Ian Parry is Principal Environmental Fiscal Policy Expert in the IMF’s Fiscal Affairs Department, specializing in fiscal analysis of climate change, environment, and energy issues. Before joining the Fund in 2010, Ian held the Allen V. Kneese Chair in Environmental Economics at Resources for the Future.

Posted by at 5:05 PM

Labels: Energy & Climate Change

Monday, June 10, 2019

GDP and beyond: New Zealand’s well-being budget prioritizes gross national well-being

From a Vox piece on NZ’s well-being budget:

“To Prime Minister Jacinda Ardern, the purpose of government spending is to ensure citizens’ health and life satisfaction, and that — not wealth or economic growth — is the metric by which a country’s progress should be measured. GDP alone, she said, “does not guarantee improvement to our living standards” and nor does it “take into account who benefits and who is left out.”The budget requires all new spending to go toward five specific well-being goals: bolstering mental health, reducing child poverty, supporting indigenous peoples, moving to a low-carbon-emission economy, and flourishing in a digital age. To measure progress toward these goals, New Zealand will use 61 indicators tracking everything from loneliness to trust in government institutions, alongside more traditional issues like water quality.”

Other material on similar subjects include an earlier IMF paper on Bhutan’s Gross National Happiness index (GNH) by Sriram Balasubramanian and Paul Cashin and a Vox piece on new growth models.

From a Vox piece on NZ’s well-being budget:

“To Prime Minister Jacinda Ardern, the purpose of government spending is to ensure citizens’ health and life satisfaction, and that — not wealth or economic growth — is the metric by which a country’s progress should be measured. GDP alone, she said, “does not guarantee improvement to our living standards” and nor does it “take into account who benefits and who is left out.”The budget requires all new spending to go toward five specific well-being goals: bolstering mental health,

Posted by at 10:09 AM

Labels: Inclusive Growth, Uncategorized

Thursday, June 6, 2019

Understanding Housing Finance: Views from Susan Wachter

Global Housing Watch Newsletter: May 2019

Susan Wachter is the Albert Sussman Professor of Real Estate and Professor of Finance at The Wharton School of the University of Pennsylvania. In this interview, Wachter talks about her work on housing finance in the U.S., the housing finance revolution, the impact of new borrowing constraints on homeownership, and more.

Before, during, and after the housing bubble…

Hites Ahir: “The American mortgage in historical and international context” is a paper that you co-authored with Richard Green. It is one of your most cited papers. Could you tell us a bit about this paper?

Susan Wachter: Richard and I identified the “American Mortgage,” the 30-year fixed-rate self-amortizing mortgage without prepayment penalty, as unique and explained its historical sources. The Great Depression was in part a housing finance crisis; as the then prevailing short-term “bullet” loans came due with no financing available, they triggered an unprecedented number of foreclosures. The response first from the Home Owners’ Loan Corporation (HOLC) and later enshrined in the new Federal Housing Administration (FHA), was to institute the new mortgage instrument, the forerunner of the American Mortgage, that would not be subject to such shocks, that would be affordable, and that would support rather than undermine systemic stability.

Hites Ahir: “The housing finance revolution” is another paper that you co-authored with Richard Green in 2007, just around the time of the Great Financial Crisis. The paper examines the institutional changes in housing finance in industrialized countries. What did you find in this paper and how do the findings tie in with the housing boom of 2000-06?

Susan Wachter: The housing finance revolution, the integration of mortgages into global financial markets, as defined here, came about in the aftermath of crises in the Savings & Loan industry and similar institutions elsewhere. Many countries across the globe segmented housing finance from capital markets prior to the 1980s. With global inflation, the banking industry’s colloquial “3-6-3 rule”—pay depositors 3 percent, lend at 6 percent, and golf at 3 o’clock—could no longer work, as money market funds offered rates far higher than the 6 percent. The Savings & Loan industry hemorrhaged deposits and ultimately failed due to this asset-liability mismatch: long-term mortgages could not be funded by short-term deposits. Securitization provided an alternative source of funds accessed from global capital markets, through the government-sponsored enterprises Fannie Mae and Freddie Mac. The housing finance revolution, the move from segmented and regulated S&L lending to mortgage-backed securities—integrated with global capital markets but still regulated through the GSEs—was followed by a deregulation of securitization. The deregulation led to the proliferation of unregulated private-label mortgage-backed securitization which funded risky loans that were poorly underwritten and underpriced for risk. These loans funded the housing boom of 2000 to 2006.

Hites Ahir: You have tried to explain the housing bubble with Adam Levitin. In a nutshell, what is the explanation?

Susan Wachter: The bubble was the result of a shift in mortgage finance from regulated securitization by Fannie Mae and Freddie Mac to unregulated securitization by Wall Street banks. Housing is uniquely vulnerable to credit-fueled bubbles because it cannot be directly shorted and because of the correlated nature of home prices. Accordingly, the market’s stability has always depended on regulation of underwriting standards. Those underwriting standards helped establish the dominance of the 30-year fixed rate mortgage, a uniquely American product that has been the bedrock of middle-class homeownership and contributed to financial stability. The shift from regulated Fannie/Freddie securitization to unregulated Wall Street securitization led to a race to the bottom in underwriting standards as banks competed for market share. The result was an oversupply of underpriced credit, marked by a shift from the traditional 30-year fixed to exotic products resembling pre-Depression “bullet loans.” With credit constraints loosened, borrowers were able to bid up housing prices, which pushed up the price of neighboring properties because of price correlation. Higher home prices made mortgages on those properties look safer, thus encouraging more lending. Yet the credit-fueled rise in home prices was unsustainable for more than a few years because of the limit on demand for homeownership. Once the newly unconstrained demand was tapped, home prices peaked, and the price correlations that make housing so susceptible to credit bubbles now operated in reverse to produce a devasting downward spiral in home prices and mortgage defaults that sparked the 2008 financial crisis.

Hites Ahir: 12 years later—it is 2019, what is the current state of housing finance in the U.S.?

Susan Wachter: The overall economy has more than recovered, and inflation-adjusted housing prices are near their 2006 highs, but, supported by low interest rates and high rents, they are not in bubble territory. Nonetheless, echoes of the crisis remain. More than 10 years after the U.S. government placed the GSEs—government-sponsored enterprises—into conservatorship, they remain in limbo. The major unfinished business of the Great Recession is the reform of the housing finance system and particularly Fannie Mae and Freddie Mac which together with Ginnie Mae today provide 70 percent of the financing for the housing market, with taxpayers at risk.

Housing finance and homeownership

Hites Ahir: Are there limits to housing finance in promoting homeownership?

Susan Wachter: Yes, there are limits: housing finance systems can lower the cost of funds, through efficient market pricing of interest rate risk and default risk, and by limiting systemic risk, preventing underwriting standards from deterioration and leverage from excessive growth in the good times, as I discuss here. But beyond this, if mortgage interest rates pro-cyclically underprice risk, perhaps in an attempt to lower the cost of lending, the result will be a higher cost of lending as the resulting instability gets priced into future housing finance lending.

Hites Ahir: With Roberto G. Quercia and George W. McCarthy, you assessed the impact of affordable lending efforts on homeownership rates. What is the verdict?

Susan Wachter: Yes, it is possible to cross-subsidize lending rates. The profit rate on loans does not have to be similarly high for all lending segments of the market, adjusting for risk. Pooling for risk is efficient due to diversification gains, and high-end borrowers may willingly join in, resulting in a stable pool even with cross-subsidies.

Hites Ahir: After the Great Recession, mortgage lending became stricter. How have the new borrowing constraints changed U.S. homeownership rates?

Susan Wachter: The evidence is that homeownership rates, particularly among millennials, are lower, in part due to FICO score and other requirements that go beyond levels that prevailed before the crisis. While renting is a choice and a good choice for many, some households are constrained, that is they may prefer to be homeowners, and may pay more as renters, but they cannot qualify to be homeowners. This is a concern particularly in gentrifying markets, since homeownership can provide a hedge against rent increases and enable households to stay in markets that optimize their lifetime opportunities.

Looking back and ahead

Hites Ahir: I looked at the list of refereed papers that you have published over the years. “The Impact of Agricultural Prices on Inflation” is your first refereed paper, published in 1975. However, your first paper on housing markets appears about 10 years later—“Residential Real Estate Brokerage: Rate Uniformity and Moral Hazard” in 1987. What triggered your interest in housing markets?

Susan Wachter: I have always been interested in land markets and in policy. That paper, which was the subject of my PhD thesis, was recently updated in a 2016 jointly co-authored paper with Davide Furceri, Prakash Loungani, and John Simon—“Global Food Prices and Domestic Inflation: Some Cross-Country Evidence.” I was and still am fascinated by what we can learn by global comparisons. But having a family meant a period of domestic interest in both senses of the word.

Hites Ahir: You have written a lot about housing markets, especially housing finance. What would be the top five papers on housing finance that I should read?

Susan Wachter: My early work with Richard Herring, “Real Estate Booms and Banking Busts,” shows how banks respond to booms by their lending practices, accelerating booms into bubbles. Several papers with Andrey Pavlov take this further and point to banks’ incentivizing borrowing when they underprice the option to default which is imbedded in mortgages. “Subprime Lending and Real Estate Prices” shows how this lower cost of lending led to higher house prices in the US bubble. “Mortgage Put Options and Real Estate Markets” derives a bubble indicator, the correlation of a decline in the credit risk premium with price rises, adjusted for fundamentals, and shows how this indicator is associated with the severity of price declines after prices peak across many countries. Finally, an article I wrote for the National Institute of Economic and Social Research (NIER), “The Market Structure of Securitisation and the US Housing Bubble,” shows how all financial institutions that lend to real estate are impacted by unsustainably risky lending that leads to correlated real estate price declines and, through financial contagion effects, systemic risk. This sets up the need for macro prudential policy. For a comprehensive account of the rise and collapse in home prices that sparked the 2008 financial crisis, see The Great American Housing Bubble, co-authored with Adam Levitin, forthcoming, Harvard University Press.

Hites Ahir: What kind of questions would you like future research on housing finance to address?

Susan Wachter: Global finance and housing finance are now integrated and will continue be so going forward. How do nations address the inevitable housing finance and housing affordability challenges, in an era of an increasing attraction of urban centrality, and consequently higher housing prices, in developed and emerging economies? Housing finance, macro instability, and the new affordability concerns together raise important questions—ones that we in the housing finance community can address to help inform social and financial stability policies across nations.

Photo by Breno Assis

Global Housing Watch Newsletter: May 2019

Susan Wachter is the Albert Sussman Professor of Real Estate and Professor of Finance at The Wharton School of the University of Pennsylvania. In this interview, Wachter talks about her work on housing finance in the U.S., the housing finance revolution, the impact of new borrowing constraints on homeownership, and more.

Posted by at 2:30 PM

Labels: Global Housing Watch

Subscribe to: Posts