Wednesday, June 12, 2019

House Prices in Norway

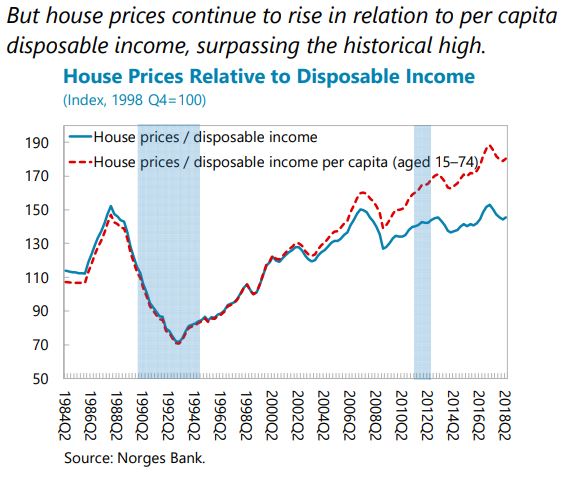

From the IMF’s latest report on Norway:

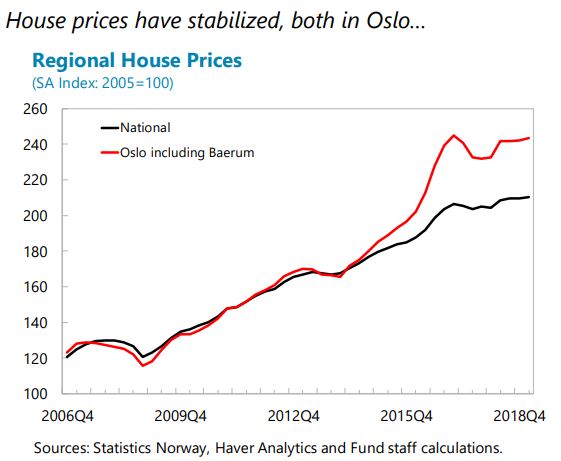

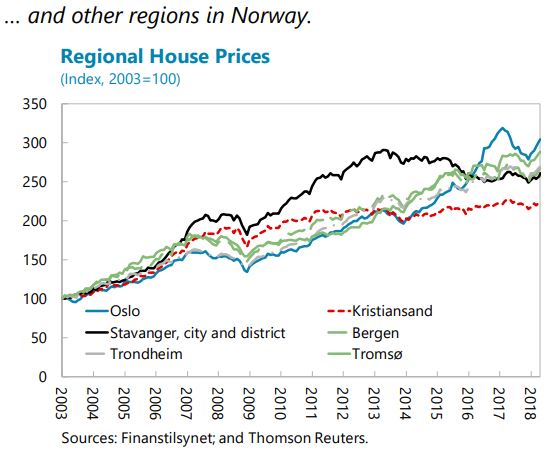

- “House prices remain overvalued, albeit less so than last year, and household debt continues to rise from an already elevated level (…). The house price moderation discussed earlier has improved housing affordability and correspondingly lowered the risks of a price crash. Nevertheless, house prices remain above fundamentals per staff estimates (0–10 percent at the national level and 5–20 percent in Oslo). Moreover, household indebtedness continues to increase from already high levels, leaving households vulnerable to sharp interest rate rises. Besides mortgages, the rapid growth of consumer credit also warrants close watch, even if it starts from a small base.

- Risks from commercial real estate are rising (…). Commercial real estate prices have increased by about 60 percent since 2000 in real terms, and more than twice that in prime Oslo. Although yields in Norway are not especially low, Oslo’s prime market has the lowest yield compression among major European cities. Banks have substantial exposure to CRE loans25 which account for 15 percent of banks’ loan portfolio (23 percent of GDP), higher than peer countries.”

- The current prudential toolkit to mitigate financial stability risks is quite comprehensive and should not be loosened at this stage.

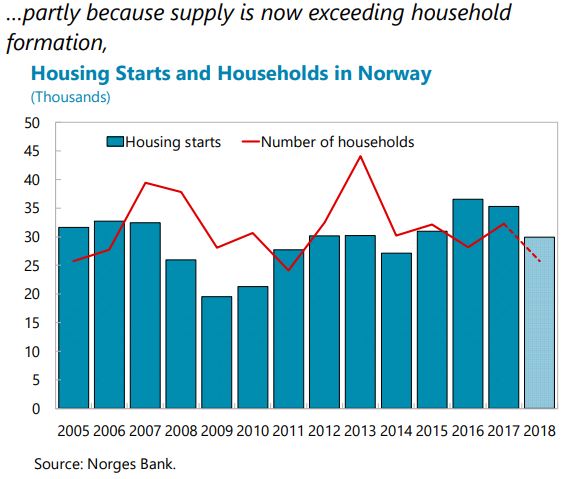

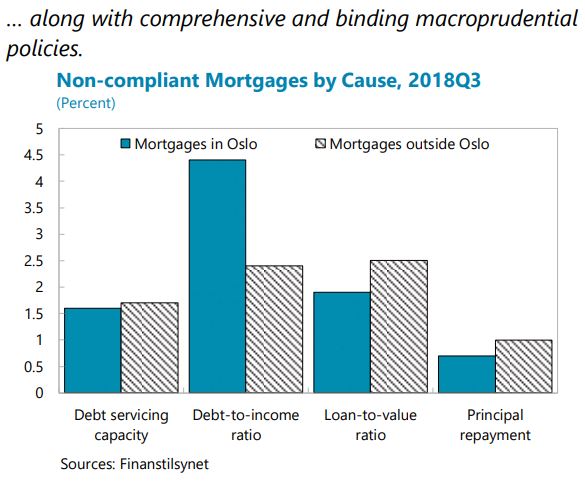

Residential housing: The current mortgage regulations, renewed last year, consist of both capital and borrower-based measures such as maximum LTV and DTI ratios, and are welltargeted to areas with higher risks such as Oslo. Together, they have contributed to containing the incidence of risky mortgages, not least in the capital. Given that prices are still overvalued, and that household debt continues to rise, the regulations should be extended as is when reviewed at year-end, barring large unexpected developments in the coming months. The tighter limits for Oslo should be preserved. As recommended in previous years, the mortgage regulations could also be made permanent; the parameters could then be adjusted as needed over the financial cycle.”

Posted by at 2:22 PM

Labels: Global Housing Watch

Subscribe to: Posts