Friday, July 12, 2019

Housing View – July 12, 2019

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St. Louis

- A New Approach on Housing Affordability – New York Times

- Kamala Harris’ Plan To End the Racial Homeownership Gap Doubles Down on the Worst Aspects of U.S. Housing Policy – Reason

- Rebounds in Homeownership Have Not Reduced the Gap for Black Homeowners – The Harvard Joint Center for Housing Studies

- Democrats May Inflate Another Housing Bubble – Wall Street Journal

- Can This Factory Produce a Cheaper Apartment? – Citylab

- Don’t look now, but home equity delinquencies are rising – American Banker

On other countries:

- [Chile] Chile’s house prices are rising strongly – Global Property Guide

- [Portugal] Portugal Passes ‘Right to Housing’ Law As Prices Surge – Citylab

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 11, 2019

Housing Market in the Euro Area

From the IMF’s latest report on the Euro Area:

“Macroprudential policies should be used more actively to manage financial vulnerabilities in both housing and corporate sectors. France, for example, has tightened large exposure limits for big French banks lending to highly indebted corporates, and some countries have increased their countercyclical capital buffers. However, bank-based tools cannot address risks arising from nonbank loans. As recommended in the 2018 FSAP, borrower-based tools could be legislated where they are currently unavailable, and used more proactively against risky firms and households. In particular a range of borrower-based tools for corporates (such as limits on loan-to-value ratios for commercial real estate, debt/equity caps and minimum ICRs) should be explored, and national macroprudential supervisors should have the authority to use these tools for all financial institutions. The authorities should also monitor liquidity risks in investment funds that are increasingly exposed to lower-grade corporate debt and real estate in search for yield. In order to be effective, comprehensive and comparable credit information systems need to be available in all countries. Urgently addressing data gaps in the area of commercial real estate and nonbank financial institutions is also needed to allow a fuller assessment of financial stability risks.”

From the IMF’s latest report on the Euro Area:

“Macroprudential policies should be used more actively to manage financial vulnerabilities in both housing and corporate sectors. France, for example, has tightened large exposure limits for big French banks lending to highly indebted corporates, and some countries have increased their countercyclical capital buffers. However, bank-based tools cannot address risks arising from nonbank loans. As recommended in the 2018 FSAP, borrower-based tools could be legislated where they are currently unavailable,

Posted by at 11:07 AM

Labels: Global Housing Watch

Wednesday, July 10, 2019

Housing Market in Germany

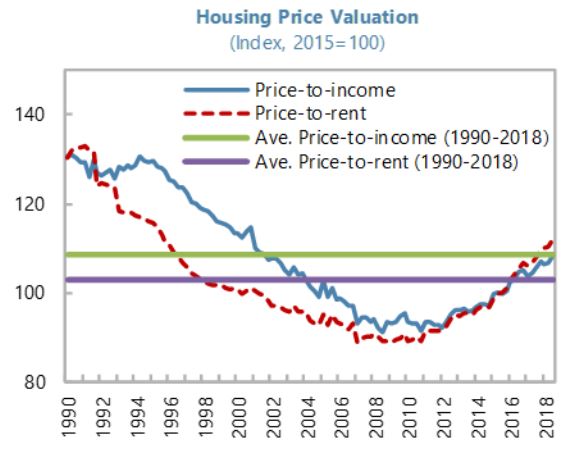

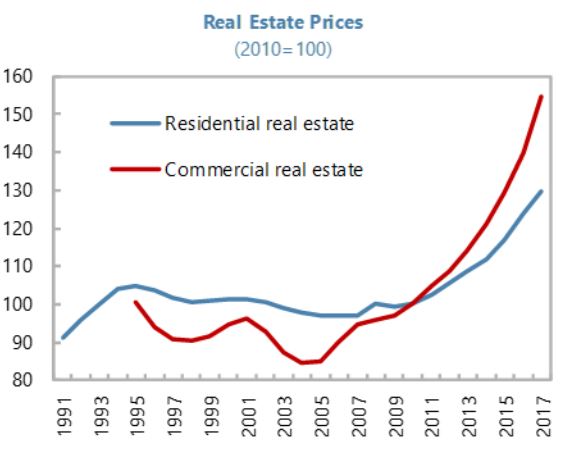

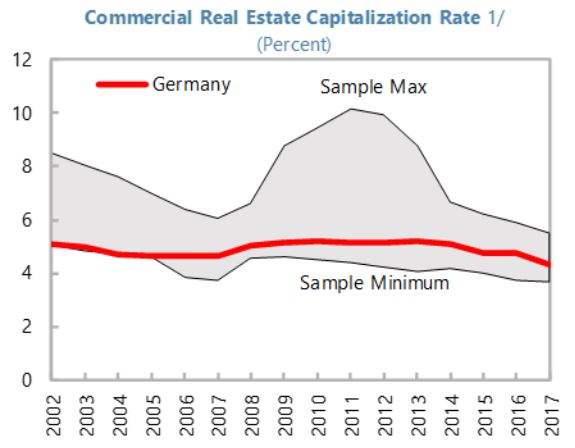

From the IMF’s latest report on Germany:

“Real estate prices continue to rise rapidly while aggregate credit growth remains in check.

- House prices in major cities have continued to rise rapidly, moving further into overvaluation territory. Staff analysis suggests that house prices were overvalued in Germany’s main cities, from 10–15 percent in Stuttgart and Dusseldorf to 25–30 percent in Hannover, Frankfurt and Hamburg and more than 40 percent in Munich in 2017.11 The government has stepped up efforts to increase housing supply, including by allocating €2 billion to build 100,000 new social housing units during 2020–21, selling federally-owned properties to local authorities at reduced prices to build affordable housing, and providing a special depreciation allowance for new rental housing construction. The impact on house prices, however, is expected to be limited.

- Commercial real estate (CRE) prices have risen even faster than house prices (…) with a moderate decline in the yield on CRE investment (…). Price increases have been particularly large in the office sub-segment and banks’ exposure to the sector has risen over the last three years, despite the sizable share of equity-based and foreign-financed investment.

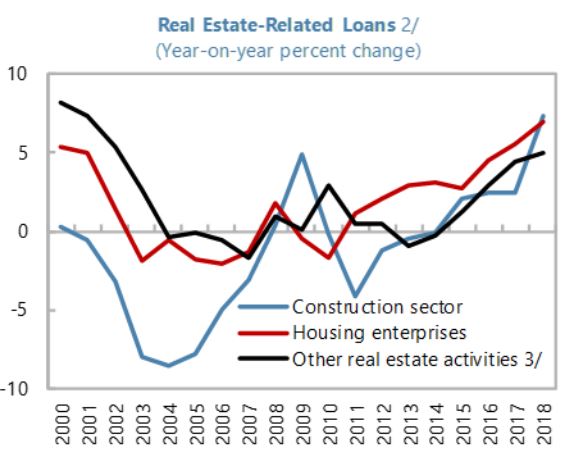

- These rapid price increases have not yet been accompanied by strong increases in credit growth at the aggregate level. Credit growth accelerated to a pace slightly exceeding nominal GDP growth, but the credit-to-GDP ratio remains low from a historical perspective and compared with other advanced economies. Bank lending to CRE-related activities also appears relatively small compared to the EU average, yet the impact of a sharp decline in CRE prices on bank balance sheets could still be important as defaults on CRE tend to be higher than those on residential real estate.

Additional macroprudential action is needed to guard against imbalances in the real estate sector.

- Urgently address data gaps. The Bank Lending Survey suggests that LTV ratios for new mortgage loans have been relatively stable on an aggregate basis (…), yet lack of granular loan information hinders a full assessment of potential financial stability risks in specific market segments. It is essential that these data gaps be addressed.

- Consider prompt activation of the existing borrower-based measures. Absent granular data alongside the prolonged rise in house prices, the authorities should consider implementing an LTV cap and amortization requirements on mortgages.

- Expand the macroprudential toolkit. Germany currently lacks income-based instruments for residential and CRE lending or other borrowerbased instruments for CRE lending. The authorities should consider introducing income-based instruments, such as a debt-toincome or debt-service-to-income cap. In addition, appropriate instruments for CRE should also be considered, taking into account diverse financing structures. As the government is currently reviewing the effectiveness of existing instruments, this is a right time to consider expanding the toolkit.”

From the IMF’s latest report on Germany:

“Real estate prices continue to rise rapidly while aggregate credit growth remains in check.

- House prices in major cities have continued to rise rapidly, moving further into overvaluation territory. Staff analysis suggests that house prices were overvalued in Germany’s main cities, from 10–15 percent in Stuttgart and Dusseldorf to 25–30 percent in Hannover, Frankfurt and Hamburg and more than 40 percent in Munich in 2017.11 The government has stepped up efforts to increase housing supply,

Posted by at 12:11 PM

Labels: Global Housing Watch

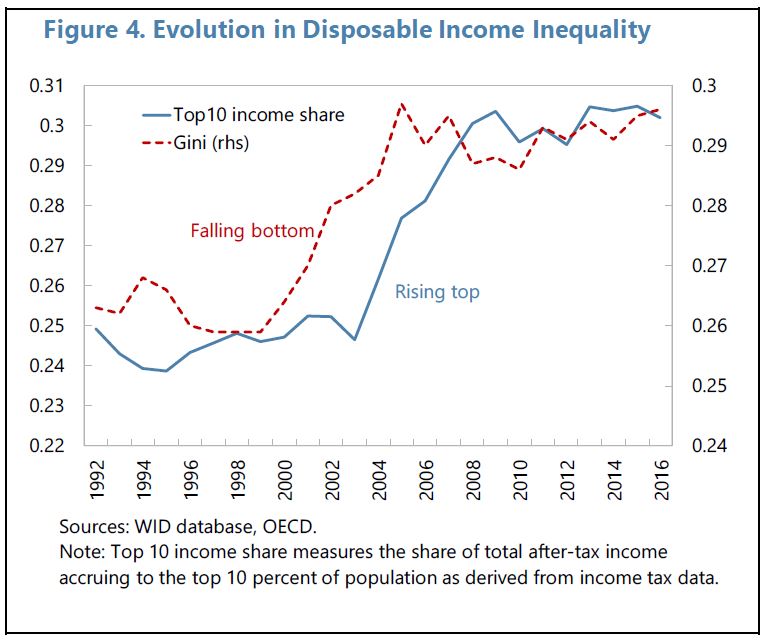

Wealth Inequality and Private Savings in Germany

From latest IMF report on Germany:

“Does the large current account surplus in Germany reflect export-driven income gains that are evenly shared among the population? The evidence strongly suggests this is not the case and underscores the important role of German business wealth concentration in this context. As high corporate savings and underlying profits largely reflect capital income accruing to wealthy households and increasingly retained in closely-held firms, the buildup of external imbalance has been accompanied by widening top income inequality, rising private savings and compressed consumption rates.”

From latest IMF report on Germany:

“Does the large current account surplus in Germany reflect export-driven income gains that are evenly shared among the population? The evidence strongly suggests this is not the case and underscores the important role of German business wealth concentration in this context. As high corporate savings and underlying profits largely reflect capital income accruing to wealthy households and increasingly retained in closely-held firms, the buildup of external imbalance has been accompanied by widening top income inequality,

Posted by at 12:02 PM

Labels: Inclusive Growth

Monday, July 8, 2019

Grenada : Climate Change Policy Assessment

From the IMF’s latest report on Grenada:

“Grenada has made significant strides to counter climate change but meeting the daunting remaining challenges will require domestic policy actions and sustained international support. Climate change is an existential threat to Grenada. Increasing frequency and intensity of coastal storms threatens infrastructure and livelihoods, as do increased risk of coastal flooding and drought. Notably, Hurricane Ivan in 2004 caused damages of over 200 percent of GDP. Grenada has recognized this by placing climate resilience at the center of its policy making and forging strategic alliances with key global climate finance providers. However, the challenges facing the country remain daunting and will require large increases in international support, both financial and technical, to assist the Grenadian authorities turn their impressive resilience plans into action.

This Climate Change Policy Assessment (CCPA) takes stock of Grenada’s plans to manage its climate response, from the perspective of their macroeconomic and fiscal implications. The CCPA is a joint initiative by the IMF and World Bank to assist small states to understand and manage the expected economic impact of climate change, while safeguarding long-run fiscal and external sustainability. It explores the possible impact of climate change and natural disasters on the macroeconomy and the cost of Grenada’s planned response. It suggests macroeconomically relevant reforms that could strengthen the likelihood of success of the national strategy and identifies policy gaps and resource needs.

General preparedness for climate change. Grenada has made significant strides in preparedness. Its Nationally Determined Contribution (NDC) sets out an ambitious agenda for mitigation. The Climate Change Policy and National Adaptation Plan (NAP) provide costed detailed plans for adaptation and resilience building. The establishment of the Ministry of Climate Resilience in 2017 has further promoted mainstreaming of climate adaptation. However, implementation capacity remains a huge impediment to meeting NAP goals, particularly given Grenada’s tight fiscal constraints. Post-disaster activities and responsibilities are well-articulated but require formalization and more progress is required on financing. A Disaster Resilience Strategy (DRS) drawing on the recommendations of the CCPA and summarizing and synthesizing actions from other plans and strategies would help Grenada improve its readiness to cope with future disasters.

Mitigation. Grenada plans to progress on its mitigation pledge for the Paris Agreement in the near term by expanding the share of renewable energy in the power generation mix and by adopting energy efficiency measures including in the transport sector. However, progress has been slow and a finalized legal and regulatory framework is needed to provide incentives for this to occur. In addition, Grenada could consider using upstream fuel excise-based carbon taxation to reinforce price incentives towards energy efficiency paying due attention to distributional impacts, administrative efficiency and competitiveness. Feebates (tax-subsidy schemes integrated into existing excises) could further reinforce mitigation incentives.

Adaptation. Grenada’s adaptation strategy—the NAP—covers all infrastructure sectors, land, agroforestry, agriculture, fishing, food security, water, mangrove, marine, coral, health, and zone management. An estimated one-third of capital expenditures in 2019 budget already goes to resilience-building projects. However, progress is hindered by capacity constraints, in particular in investment project execution. Progress is being made on supporting policies and regulations but implementation and enforcement need to be strengthened, notably with regard to building codes and draining maintenance.

Financing. Grenada faces huge financing challenges to meet its ambitious climate change policy. The authorities have estimated financing needs at about US$500 million, equivalent to over 40 percent of 2018 GDP. Even if most mitigation investment can be financed by the private sector, the required adaptation investment of at least US$340 million out of the $500 million estimated by the authorities is difficult to reconcile with fiscal constraints and other priority needs, including general infrastructure maintenance and development. Proposed reforms to the Fiscal Responsibility Law (FRL) may open some space for increased revenue and loan-financed investment in resilient infrastructure but maintaining a safe debt level means that this will be limited. Maximizing use of available grant financing is therefore crucial for Grenada to ensure long term fiscal sustainability while meeting climate adaptation goals. Grenada has made some progress in beginning to access global climate financing and needs to build on this to maintain progress. However, as the availability of these funds for Grenada may be limited they will need to be supplemented by domestic revenue mobilization, available concessional loans and increased private sector participation remain key to any resource mobilization strategy.

Risk management. Grenada has well identified disaster and climate risks but does not yet have a comprehensive risk and contingent liability assessment. The authorities have put in place a number of elements of a comprehensive natural disaster risk layering strategy, including establishing contingency funds, participating in regional parametric insurance schemes and including a hurricane clause in debt restructuring agreements. However, indemnity and catastrophe insurance is underused in both the public and private sectors and Grenada has not established contingent lines of finance. Fiscal buffers also fall short of desirable levels. Grenada could enhance its risk management by putting place a National Natural Disaster Risk Financing Strategy as a key element of the broader DRS. This would guide future policy making on risk transfer and retention, including trade-offs between options and provide a framework for seeking increased international support.

National processes. The establishment of Ministry of Climate Resilience has helped to further strengthen the mainstreaming of climate-related projects. Climate resilience has been built into the public sector investment program framework as a key screening element, but in practice the weight given to climate resilience project prioritization and selection process is not yet clear. Weak project management capacity is a considerable drag on Grenada’s public investment management system. Grenada should establish an asset registry which would be the foundation for well managed asset insurance and disaster loss assessment.

Priority needs. To meet its mitigation plan, Grenada will need to rely heavily on private investment. Investment needs for adaptation require using as much grant and concessional financing (including contingent financing for natural disasters) as possible to maintain debt sustainability, while also creating space for private sector participation and increasing, where possible, domestic resource mobilization. Expansion of insurance coverage should also play a role but cannot substitute for investments in resilient infrastructure. Capacity building will also be crucial including for public investment management and to help complete the DRS, move toward carbon taxation, and enhance implementation of sectoral adaptation plans.

From the IMF’s latest report on Grenada:

“Grenada has made significant strides to counter climate change but meeting the daunting remaining challenges will require domestic policy actions and sustained international support. Climate change is an existential threat to Grenada. Increasing frequency and intensity of coastal storms threatens infrastructure and livelihoods, as do increased risk of coastal flooding and drought. Notably, Hurricane Ivan in 2004 caused damages of over 200 percent of GDP.

Posted by at 10:36 AM

Labels: Energy & Climate Change

Subscribe to: Posts