Wednesday, July 10, 2019

Housing Market in Germany

From the IMF’s latest report on Germany:

“Real estate prices continue to rise rapidly while aggregate credit growth remains in check.

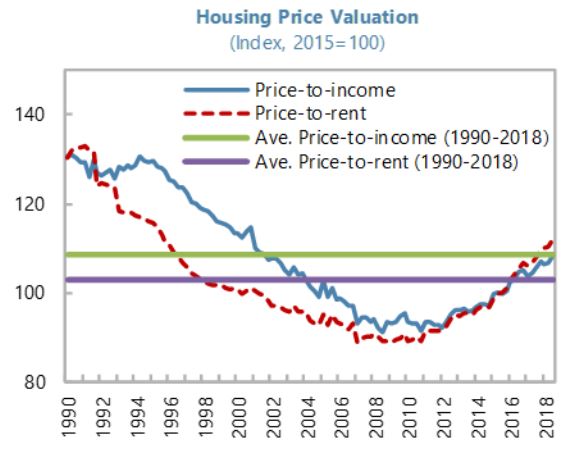

- House prices in major cities have continued to rise rapidly, moving further into overvaluation territory. Staff analysis suggests that house prices were overvalued in Germany’s main cities, from 10–15 percent in Stuttgart and Dusseldorf to 25–30 percent in Hannover, Frankfurt and Hamburg and more than 40 percent in Munich in 2017.11 The government has stepped up efforts to increase housing supply, including by allocating €2 billion to build 100,000 new social housing units during 2020–21, selling federally-owned properties to local authorities at reduced prices to build affordable housing, and providing a special depreciation allowance for new rental housing construction. The impact on house prices, however, is expected to be limited.

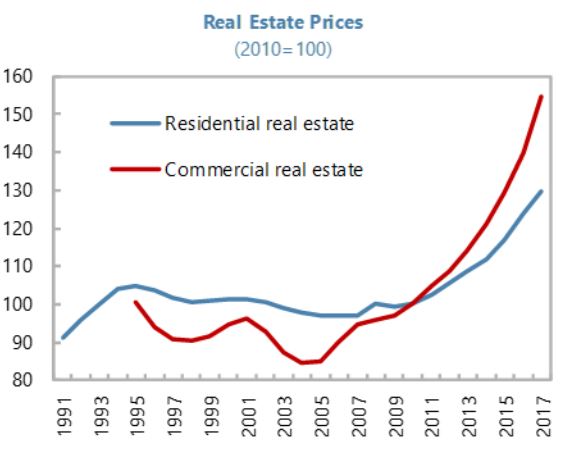

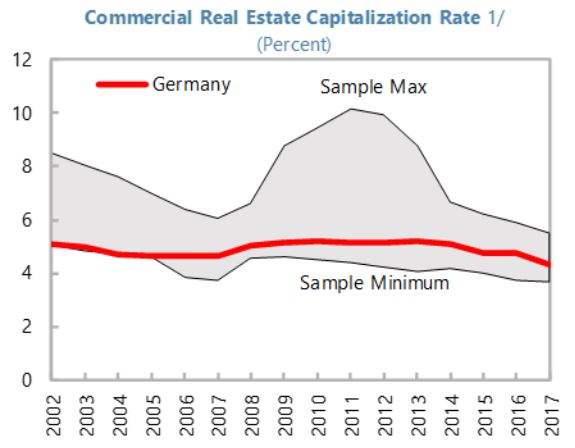

- Commercial real estate (CRE) prices have risen even faster than house prices (…) with a moderate decline in the yield on CRE investment (…). Price increases have been particularly large in the office sub-segment and banks’ exposure to the sector has risen over the last three years, despite the sizable share of equity-based and foreign-financed investment.

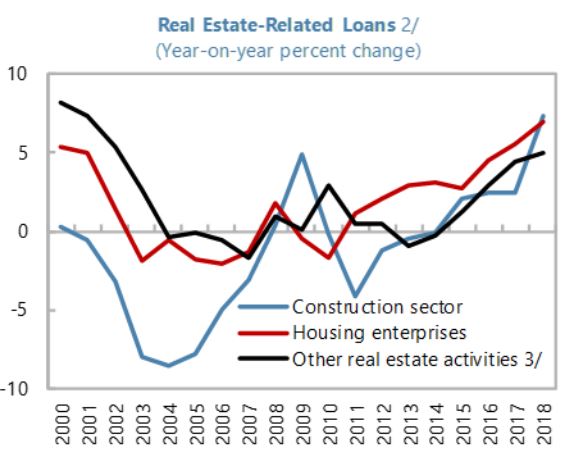

- These rapid price increases have not yet been accompanied by strong increases in credit growth at the aggregate level. Credit growth accelerated to a pace slightly exceeding nominal GDP growth, but the credit-to-GDP ratio remains low from a historical perspective and compared with other advanced economies. Bank lending to CRE-related activities also appears relatively small compared to the EU average, yet the impact of a sharp decline in CRE prices on bank balance sheets could still be important as defaults on CRE tend to be higher than those on residential real estate.

Additional macroprudential action is needed to guard against imbalances in the real estate sector.

- Urgently address data gaps. The Bank Lending Survey suggests that LTV ratios for new mortgage loans have been relatively stable on an aggregate basis (…), yet lack of granular loan information hinders a full assessment of potential financial stability risks in specific market segments. It is essential that these data gaps be addressed.

- Consider prompt activation of the existing borrower-based measures. Absent granular data alongside the prolonged rise in house prices, the authorities should consider implementing an LTV cap and amortization requirements on mortgages.

- Expand the macroprudential toolkit. Germany currently lacks income-based instruments for residential and CRE lending or other borrowerbased instruments for CRE lending. The authorities should consider introducing income-based instruments, such as a debt-toincome or debt-service-to-income cap. In addition, appropriate instruments for CRE should also be considered, taking into account diverse financing structures. As the government is currently reviewing the effectiveness of existing instruments, this is a right time to consider expanding the toolkit.”

Posted by at 12:11 PM

Labels: Global Housing Watch

Subscribe to: Posts