Monday, September 9, 2019

The Global Liveability Index 2019

From the Economist Intelligence Unit:

“The EIU’s Global Liveability Index 2019 has crowned Vienna as the world’s most liveable city. Vienna has retained pole position this year, overcoming stiff competition from Melbourne, Sydney, and Osaka.

Canadian cities have fared better than their US counterparts, with three in the top 10 and a fourth, Montreal (20th), ranked above any city south of the border. Meanwhile, the Venezuelan capital, Caracas, ranks in the bottom 10 as the government’s fight for legitimacy has impeded its ability to provide basic services for its citizens.”

From the Economist Intelligence Unit:

“The EIU’s Global Liveability Index 2019 has crowned Vienna as the world’s most liveable city. Vienna has retained pole position this year, overcoming stiff competition from Melbourne, Sydney, and Osaka.

Canadian cities have fared better than their US counterparts, with three in the top 10 and a fourth, Montreal (20th), ranked above any city south of the border. Meanwhile, the Venezuelan capital, Caracas, ranks in the bottom 10 as the government’s fight for legitimacy has impeded its ability to provide basic services for its citizens.”

Posted by at 2:15 PM

Labels: Global Housing Watch

Housing Market in Saudi Arabia

From the IMF’s latest report on Saudi Arabia:

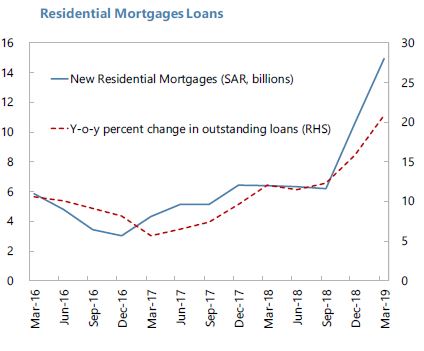

“Mortgage lending is growing strongly, and real estate prices have declined in recent years. Risks at this stage are limited, but policymakers need to keep a close eye on financial and fiscal risks from the housing market.

Real estate prices have fallen by around 20 percent since 2014. Housing rents have also been falling since early 2017. New supply is being driven by government initiatives to build affordable homes while the departure of expatriates may have slowed housing demand.

The government has initiated programs to build affordable housing and raise home ownership. It is providing access to land and financing to developers and encouraging new building technologies to increase the supply of houses. The white land tax announced in 2016 aims to incentivize land development. The approval of real estate investment traded funds (REITs) in 2016 and other reforms are expected to ease financial constraints faced by developers. In February 2018, a SAR 120 billion mortgage market plan was introduced to provide subsidized loans and support for developers. In addition, the developmental housing program partners with NGOs to build affordable houses for low-income households.

Housing demand is being spurred by credit policies and demographic trends. Increasing urbanization and declining household size are increasing housing demand by Saudis, while the departure of expatriates is slowing demand in the rental segment of the market. A new mortgage law was introduced in 2012 that enabled banks and non-bank institutions to lend for residential real estate. A facilitated mortgage program was introduced in 2016 to help Saudi families obtain mortgage loans. The maximum loan-to-value (LTV) ratio for first-time buyers was increased from 85 to 90 percent in January 2018 and risk weights on mortgage loans have been reduced. The PIF has set-up a mortgage refinance company.

Policymakers should remain vigilant about potential fiscal and financial risks as the real estate market develops. Large house price movements may trigger financial and macro instability as highlighted in the April 2019 Global Financial Stability Report (GFSR). Banks’ exposure to the real estate sector is limited—mortgage loans were 17 percent of total bank credit to private sector at end-2018. In addition, mortgage payments are often directly debited from salary, limiting the likelihood of default. Further, many new mortgage loans are guaranteed by the government. Going forward, however, prudential policies should continue to pay close attention to the real estate market and the fiscal impact of housing programs including through PPPs will need to be carefully assessed.”

From the IMF’s latest report on Saudi Arabia:

“Mortgage lending is growing strongly, and real estate prices have declined in recent years. Risks at this stage are limited, but policymakers need to keep a close eye on financial and fiscal risks from the housing market.

Real estate prices have fallen by around 20 percent since 2014. Housing rents have also been falling since early 2017. New supply is being driven by government initiatives to build affordable homes while the departure of expatriates may have slowed housing demand.

Posted by at 2:10 PM

Labels: Global Housing Watch

Wednesday, August 21, 2019

Attempting to Avoid a Recession: Fortune or Folly?

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession, as determined by the National Bureau of Economic Research (or NBER, a private, non-profit, non-partisan organisation). The timing of our hypothetical decisions to sell out of the market and buy back into the market varied by up to eight quarters before and after each actual recession start and end date. This gave us a grand total of 2,577 scenarios to consider, as highlighted in Exhibit 1.”

Exhibit 1: Endless Possibilities

Source: Bloomberg, SEI

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession,

Posted by at 12:29 PM

Labels: Forecasting Forum

Tuesday, August 20, 2019

Housing markets and inequality

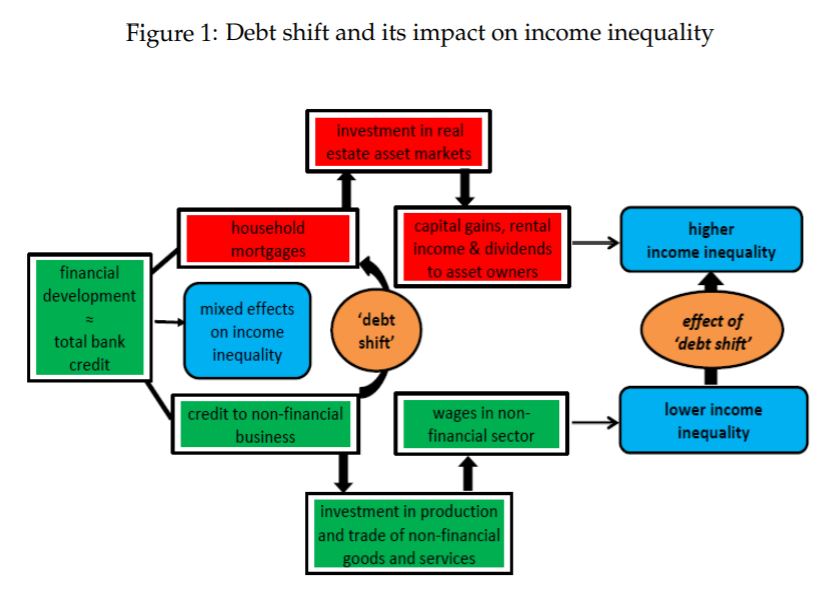

From a working paper by Dirk Bezemer and Anna Samarina:

“These results suggest that ‘debt shift’ may be one of the factors explaining recent

trends in income inequality. Credit to real estate asset markets results in rising capital

gains and growth of incomes connected to the real estate sector. Since these incomes

are concentrated among rich households, this widens income disparities. In support,

we find that mortgage credit increases the income share of households in the top 10%

of the income distribution.”Continue reading here.

From a working paper by Dirk Bezemer and Anna Samarina:

“These results suggest that ‘debt shift’ may be one of the factors explaining recent

trends in income inequality. Credit to real estate asset markets results in rising capital

gains and growth of incomes connected to the real estate sector. Since these incomes

are concentrated among rich households, this widens income disparities. In support,

we find that mortgage credit increases the income share of households in the top 10%

of the income distribution.”

Posted by at 8:13 AM

Labels: Global Housing Watch

Lessons in economics from Algeria’s victory in the Africa Cup of Nations

From a VoxEU post by Rabah Arezki:

“Algeria’s recent victory in the Africa Cup of Nations has united a country whose development model has frustrated its young and educated workforce. This column offers four lessons for economic development from the national football team’s success: on the role of competition and market forces, mobilising talent, the role of managers, and the importance of referees (i.e. regulation).

On 19 July, Algeria won the 2019 edition of the Africa Cup of Nations. The victory was the culmination of a strongly contested international football tournament with 24 teams where we saw the best of competition, talent, and refereeing on the continent. Algeria’s consecration comes amid sweeping political transformation triggered by massive demonstrations in the past few months, in turn driven by youths asking for radical change. This has united Algerians and emboldened the national team. This can-do spirit and renewed momentum are likely to be key ingredients for delivering big reforms.

On the economic front, Algeria’s development model has frustrated an educated young and increasingly female labour force aspiring to economic empowerment beyond subsidies and public jobs. The model is essentially stuck in the transition from an administrated economy to a market economy. Moreover, decades of state domination with episodes of liberalisation have yielded crony capitalism, further distancing the population from appreciating the power of harnessing markets for development.

In Algeria, as in many countries, football has triggered passions capturing dreams of greatness and unifying nations. Football can offer four lessons for economic development in Algeria, which is looking to revamp its economic model (see also Kuper and Szymanski 2009 and Palacios-Huerta 2014).

The first lesson is on the role of competition and the power of market forces. In too many sectors in Algeria, prices are controlled and state or private monopolies are the rule, stifling the space for talented Algerians to transform their economy and deterring foreign investment. This is unsustainable considering the shrinking rents coming from oil and gas ever since oil prices collapsed in 2014. Football illustrates how market mechanisms are an important filter for detecting and rewarding talent based on performance and for moving away from favouritism. Without free entry and failure, as in football, economic dynamism and momentum rapidly come to a halt.”

Continue reading here.

From a VoxEU post by Rabah Arezki:

“Algeria’s recent victory in the Africa Cup of Nations has united a country whose development model has frustrated its young and educated workforce. This column offers four lessons for economic development from the national football team’s success: on the role of competition and market forces, mobilising talent, the role of managers, and the importance of referees (i.e. regulation).

On 19 July,

Posted by at 8:09 AM

Labels: Inclusive Growth

Subscribe to: Posts