Monday, September 9, 2019

Housing Market in Saudi Arabia

From the IMF’s latest report on Saudi Arabia:

“Mortgage lending is growing strongly, and real estate prices have declined in recent years. Risks at this stage are limited, but policymakers need to keep a close eye on financial and fiscal risks from the housing market.

Real estate prices have fallen by around 20 percent since 2014. Housing rents have also been falling since early 2017. New supply is being driven by government initiatives to build affordable homes while the departure of expatriates may have slowed housing demand.

The government has initiated programs to build affordable housing and raise home ownership. It is providing access to land and financing to developers and encouraging new building technologies to increase the supply of houses. The white land tax announced in 2016 aims to incentivize land development. The approval of real estate investment traded funds (REITs) in 2016 and other reforms are expected to ease financial constraints faced by developers. In February 2018, a SAR 120 billion mortgage market plan was introduced to provide subsidized loans and support for developers. In addition, the developmental housing program partners with NGOs to build affordable houses for low-income households.

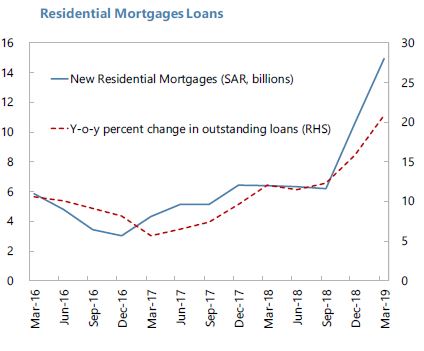

Housing demand is being spurred by credit policies and demographic trends. Increasing urbanization and declining household size are increasing housing demand by Saudis, while the departure of expatriates is slowing demand in the rental segment of the market. A new mortgage law was introduced in 2012 that enabled banks and non-bank institutions to lend for residential real estate. A facilitated mortgage program was introduced in 2016 to help Saudi families obtain mortgage loans. The maximum loan-to-value (LTV) ratio for first-time buyers was increased from 85 to 90 percent in January 2018 and risk weights on mortgage loans have been reduced. The PIF has set-up a mortgage refinance company.

Policymakers should remain vigilant about potential fiscal and financial risks as the real estate market develops. Large house price movements may trigger financial and macro instability as highlighted in the April 2019 Global Financial Stability Report (GFSR). Banks’ exposure to the real estate sector is limited—mortgage loans were 17 percent of total bank credit to private sector at end-2018. In addition, mortgage payments are often directly debited from salary, limiting the likelihood of default. Further, many new mortgage loans are guaranteed by the government. Going forward, however, prudential policies should continue to pay close attention to the real estate market and the fiscal impact of housing programs including through PPPs will need to be carefully assessed.”

Posted by at 2:10 PM

Labels: Global Housing Watch

Subscribe to: Posts