Thursday, October 24, 2019

The Phillips curve: Dead or alive

From VOX post by Peter Hooper, Frederic S. Mishkin, Amir Sufi:

“The apparent flattening of the Phillips curve has led some to claim that it is dead. The column uses data from US states and metropolitan areas to suggest a steeper slope, with non-linearities in tight labour markets. We have been here before – in the 1960s, similar low and stable inflation expectations led to the great inflation of the 1970s.

At a ‘Fed Listens’ event on 26 September 2019, Richard Clarida, vice chair of the Federal Reserve Board, observed that the flattening of the Phillips curve in recent decades is central to the Fed’s review of policy strategy (Clarida 2019). Price inflation has become much less responsive to resource slack, permitting the Fed to support employment during economic downturns more aggressively than it has in the past.

A flat Phillips curve reduces the chances of a breakout of inflation. This is especially important because the Fed considers the benefits of running a high-pressure economy, and of adopting a policy strategy that makes up for inflation misses to the downside by aiming for subsequent overshoots. Many participants in financial markets go even further than the Fed, believing that the Phillips curve is dead – in other words, excessive inflation is no longer a risk.

Recent experience in the US, Europe, and Japan appears to support this view. Major central banks struggle to get inflation to return to (or even move towards their objectives), even after labour markets have tightened. The US labour market has been running at or beyond estimates of full employment for the past two years, and inflation is still significantly below the Fed’s 2% target.

Indeed, measures of inflation expectations have been drifting lower, not higher as the Phillips curve model would predict. So is this model really dead, or just dormant? If not dead, how can we explain the flattening of the Phillips curve? What might reverse this trend, leading to a resurgence of inflation?

A lot of empirical research has been devoted to these questions over the past decade, for example Yellen (2015), Kiley (2015) Blanchard (2016), Nalewaik (2016), Powell (2018), and Hooper et al. (2019). We know that the Phillips curve was alive and well during the 1950s through the 1970s, and into the 1980s at the national level. Prices and wages showed significant sensitivity to movements in unemployment during this period. These sensitivities increased when the labour market tightened beyond full employment, indicating a nonlinear relationship. Policymakers allowed the labour market to tighten well beyond full employment levels for a sustained period during the 1960s and, at first, inflation remained low and stable. But several years of tight labour markets resulted in the great inflation of the 1970s.

Since the late 1980s, however, there has been only weak evidence of the sensitivity and nonlinearity of the response of inflation to labour market tightening. Efforts to estimate statistically significant price Phillips curve models using national data have generally failed.

Is the Phillips curve dead?

In a recent paper (Hooper et al. 2019), we argue that there are three reasons why the evidence for a dead Phillips curve is weak.”

Continue reading here.

From VOX post by Peter Hooper, Frederic S. Mishkin, Amir Sufi:

“The apparent flattening of the Phillips curve has led some to claim that it is dead. The column uses data from US states and metropolitan areas to suggest a steeper slope, with non-linearities in tight labour markets. We have been here before – in the 1960s, similar low and stable inflation expectations led to the great inflation of the 1970s.

Posted by at 10:00 AM

Labels: Macro Demystified

Monday, October 21, 2019

Understanding the rise in second-home buying

Global Housing Watch Newsletter: October 2019

In this interview, Daniel Garcia talks about his new paper: Second-Home Buying and the Housing Boom and Bust. Daniel Garcia is an economist at the Federal Reserve.

Disclaimer: The views expressed in this Q&A are those of the author, and do not reflect the views of the Federal Reserve Board or the Federal Reserve System.

Hites Ahir: What prompted you to work on this project?

Daniel Garcia: I read a paper by Neil Bhutta (2015), where he documents that existing homeowners contributed more to the rise in aggregate mortgage debt during the housing boom than all first-time borrowers, subprime and otherwise.[1] Neil’s paper showed the housing boom on the borrower side was to a large extent driven by individuals who were already homeowners – and were typically above-average in income and credit scores – rather than by borrowers becoming first time homeowners. I felt that understanding the effects of the rise in second-home buying (existing homeowners acquiring additional properties) was important macro-prudentially and a bit understudied.

Hites Ahir: How do experts measure second-home buying?

Daniel Garcia: The most reliable measure comes from anonymized credit bureau data, such as the Federal Reserve Bank of New York/Equifax Consumer Credit Panel dataset, which allows researchers to impute second-home buying based on the number of first-lien mortgages in individual’s credit files. One issue with credit bureau records is they do not contain the address of nonprimary residences. I therefore supplement my analysis with the Credit Risk Insight Servicing McDash (CRISM) dataset, a merge done by Equifax of their credit bureau records with a loan-level dataset containing property address (McDash).

Hites Ahir: How much was the increase in second-home buying during the 2000-06 period?

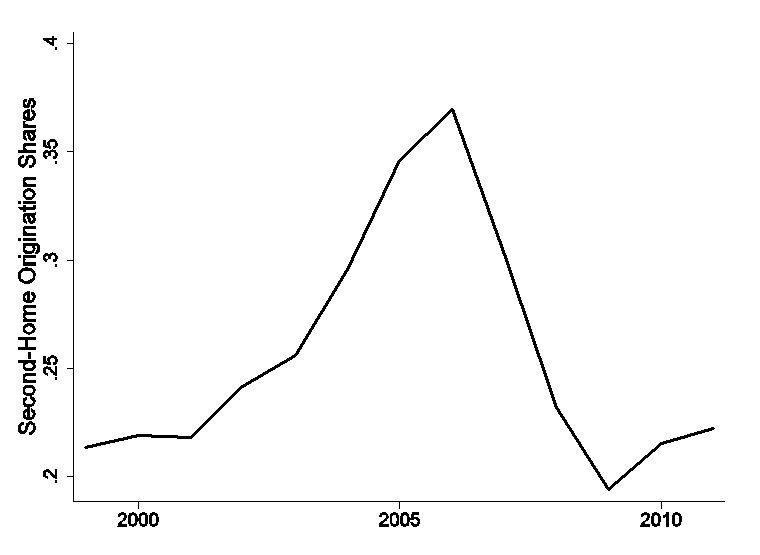

Daniel Garcia: In the Federal Reserve Bank of New York/Equifax Consumer Credit Panel dataset, the share of new home purchase loans going to existing homeowners rose from about 20 to almost 40 percent from 2000 to 2006. In other words, close to 4 in 10 purchase mortgages went to existing homeowners at the peak of the housing boom in 2006. Since the housing crash, the share of purchase mortgages going to existing homeowners is back around 20 percent (Figure 1).

Figure 1: The share of new loans for non-primary residences

Note: The figure plots the aggregate second-home origination (new loans for nonprimary residences) share by year. Source: Federal Reserve Bank of New York/Equifax Consumer Credit Panel dataset and author’s calculations.

Hites Ahir: What was driving the increase?

Daniel Garcia: Rising fundamentals in the late 1990s expansion seem an important part of the story. Locals of areas where house prices and wages grew more in the late 1990s were on average more likely to buy additional properties in the mid-2000s than elsewhere. That said, improving fundamentals are likely not the full story, because other expansions did not produce such a strong increase in second-home buying. It is likely that improving fundamentals in the late 1990s interacted with other changes in the economy, such as optimistic beliefs about house prices and easier credit conditions, to generate the increase in second-home buying.

Hites Ahir: How did the rise in second-home buying affect the economy?

Daniel Garcia: The strong rise in second-home buying could have had important macroeconomic implications, contributing to housing mispricing and over-construction during the boom and the rise in foreclosures during the recession, as argued by others such as Haughwout et al (2011); Chinco and Mayer (2019); Albanesi et al (2019). However, disentangling causality is challenging, as the rise in second-home buying could have been a symptom rather than a cause of other economic forces, such as overly optimistic beliefs about house prices.

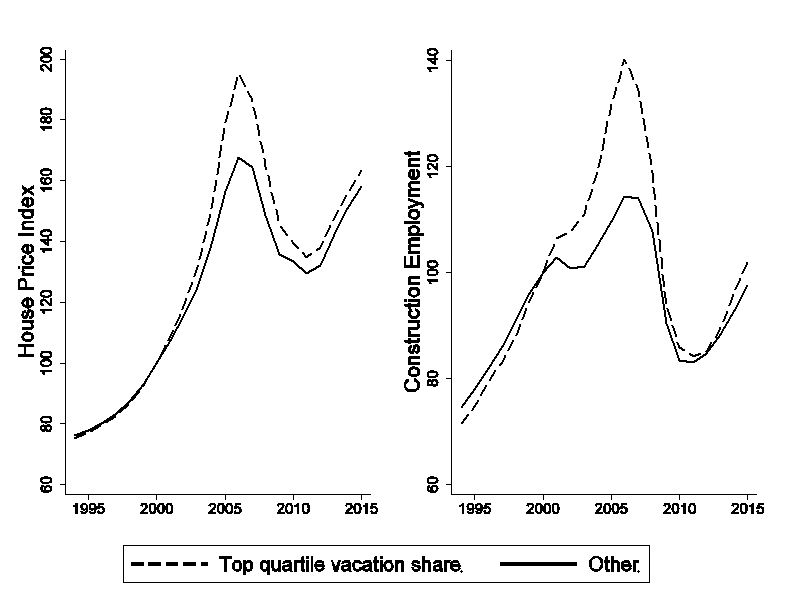

To estimate the causal effects, I focus on vacation areas, which I measure based on the vacation share of housing from the 2000 decennial census. I argue they offer an ideal laboratory – vacation areas experienced a stronger rise in second-home buying during the boom than elsewhere, reflecting factors originating elsewhere such as rising income, house prices, and demand for second homes in other parts of the country. Because of the relatively stronger rise in second-home buying there, vacation areas experienced more pronounced boom-bust episodes: house prices and construction employment grew more quickly than elsewhere during the mid -2000s and crashed more sharply during the recession (Figure 2).

In the paper, I verify that the sharp boom-bust in vacation areas was caused by changes in demand for second homes originating elsewhere, rather than by local developments, by ruling out alternative explanations. For example, vacation areas were otherwise ordinary across various other boom indicators, such as the use of alternative mortgages, private-label securitization, changes in mortgage debt by locals, pre-trends in income and house prices, supply constraints, and credit scores. Moreover, all of the stronger increase in second-home buying there was explained by purchases from out-of-town buyers.

Figure 2: House Prices and Construction Employment in Vacation vs Other Areas

Note: The figure plots house prices against time for two groups: the top quartile of vacation shares in the 2000 census, and the other counties. House prices and construction employment are indexed to equal 100 in the year 2000. Source: 2000 Census, CoreLogic HPI and Quarterly Census of Employment and Wages.

Hites Ahir: Why focus on vacation areas, and are estimates based on those areas likely to be representative?

Daniel Garcia: Housing in vacation areas allows us to estimate the causal effects of changes in second-home buying. Other parts of the country, such as cities in the sand states such as Los Angeles, Phoenix, and Las Vegas, also had high second-home buying, but also high private-label securitization, use of alternative mortgages, and increases in household debt, making it challenging to isolate the effects of second-home buying there. The appeal of vacation areas is we can confidently isolate the effects of second-home buying there.

That said, the effects of second-home buying in vacation areas are likely informative of the overall effects, because second-home buying in vacation areas was broadly representative: most of the second-home purchases there were for individuals acquiring their second or third property (about 85 percent of all second-home purchases during the boom), but also included second-home buying by borrowers with 4 or more houses, a segment of the market more likely to consist of property investors. Therefore, I interpret the main findings of the paper as informative of second-home buying overall.

Hites Ahir: What are the implications of your findings?

Daniel Garcia: The findings suggest changes in credit demand amplified the housing boom and bust. Vacation areas had a stronger housing boom and bust caused by the rise in demand for second homes in other parts of the country. It is unlikely that credit supply developments explained the boom-bust in those areas, as mortgages for vacation area properties were average in the use of alternative (such as interest-only) mortgages and private-label securitization.

Though the findings highlight the role of changes in credit demand, they are consistent with credit supply mattering elsewhere in the aggregate, as found by others (e.g. Mian and Sufi 2009; Demyanyk and Hemert 2011) including some of my own previous work (Garcia 2018). My view is that outward shifts in both credit supply and demand helped cause the housing boom and bust, likely anchored by common factors such as overly optimistic beliefs on house prices, as argued by others such as Burnside et al (2016), Piazzesi and Schneider (2016), and Kaplan et al. (2017).

Hites Ahir: What is the current state of second-home buying in the United States?

Daniel Garcia: For individuals, the share of second-home purchase shares has remained around 20 percent since the recession. The corporate share of home purchases was around 11 percent at the end of 2019, up a few percentage points from 2016 according to data from CoreLogic. Therefore, the scene appears somewhat quieter than in other countries such as the United Kingdom, Canada, and Australia, where recent rises in out-of-town buying have been more pronounced.

[1] Sometimes second-home buyers are referred to as property investors. I use the term “second-home buyers” instead, to distinguish between individual buyers from corporate investors. Moreover, many second-home purchases by individuals likely had a consumption motive – about 85 percent of all second-home purchases by individuals during the housing boom were for a second or third property.

Global Housing Watch Newsletter: October 2019

In this interview, Daniel Garcia talks about his new paper: Second-Home Buying and the Housing Boom and Bust. Daniel Garcia is an economist at the Federal Reserve.

Disclaimer: The views expressed in this Q&A are those of the author, and do not reflect the views of the Federal Reserve Board or the Federal Reserve System.

Posted by at 5:00 AM

Labels: Global Housing Watch

Sunday, October 20, 2019

Housing policies to combat the affordability crisis

From VOX post by Jack Favilukis, Pierre Mabille, Stijn Van Nieuwerburgh:

“Housing affordability is a leading challenge for local policymakers around the world, yet a coherent framework for analysing the various policy options is lacking. This column builds such a framework and uses it to show that policies that make affordable housing more efficient, that expand rent control, and that increase vouchers have a redistributive effect. Upzoning policies creates smaller, but more uniformly distributed benefits.

The ‘housing affordability crisis’ has been in the headlines in many parts of the world, and for a good reason. Among the 50 largest metropolitan statistical areas (MSAs) in the US, half of all renter households spend more than 30% of their income on rent (Joint Center for Housing Studies of Harvard University 2018). They are rent burdened. Other common metrics to quantify the lack of affordability are average rent-to-income and house price-to-income ratios. All of these metrics have been rising in most major cities in the world. Housing affordability has been the leading challenge for local policymakers. Yet a coherent framework for analysing the various policy options is lacking.

A new framework

In a recent paper (Favilukis et al. 2019), we build a framework to evaluate four major housing policy tools – zoning changes, rent control, housing vouchers, and tax credits – that policymakers employ to tackle housing affordability issues. The framework is adapted from modern macroeconomics and finance. Each period, households that differ in age and labour productivity make choices about how much to consume, save, and work; whether to own or rent a house; the size of the house; and how large a mortgage to get if they own. Savings are invested in a government bond or in rental housing.

We introduce a spatial dimension in this macro model. The metropolitan area has two locations: the city centre where people work but only some households live (zone 1), and the suburbs/outer boroughs of the MSA (zone 2) from which households commute to work. Commuting has a time cost and a financial cost. Households can choose their location in each period. Households are risk averse and face labour income and mortality risk, which they cannot perfectly insure against. This market incompleteness is the key friction in the model. The government provides some insurance through the tax code, including for example unemployment insurance. However, local policymakers can affect the provision of social insurance by using affordable housing policies.”

Continue reading here.

From VOX post by Jack Favilukis, Pierre Mabille, Stijn Van Nieuwerburgh:

“Housing affordability is a leading challenge for local policymakers around the world, yet a coherent framework for analysing the various policy options is lacking. This column builds such a framework and uses it to show that policies that make affordable housing more efficient, that expand rent control, and that increase vouchers have a redistributive effect. Upzoning policies creates smaller,

Posted by at 9:45 AM

Labels: Uncategorized

Friday, October 18, 2019

Housing View – October 18, 2019

On cross-country:

- Making Sense of Increased Synchronization in Global House Prices – Federal Reserve Bank of Dallas

On the US:

- Housing Market Points to Recession By Election Day – Council on Foreign Relations

- 2019 Cost Burden Report: Half of Renter Households Struggle With Affordability – Apartment List

- Rent control is making a comeback. Does it work? – Curbed

- This Is How to Make Democratic Candidates’ Housing Plans a Reality – Citylab

- So You Make $100,000? It Still Might Not Be Enough to Buy a Home. – Wall Street Journal

- Explaining the Black-White Homeownership Gap – Urban Institute

- How Cities Address the Housing Crisis, and Why It’s Not Enough – Citylab

- Empty Garages: The Answer to California’s Housing Shortage? – New York Times

- Policy Uncertainty and Bank Mortgage Credit – Bank for International Settlements

On other countries:

- [Argentina] Argentina defaults again; currency controls to hurt the housing market further – Global Property Guide

- [Australia] Housing and the Economy – Reserve Bank of Australia

- [Canada] How Ottawa can tackle the housing shortage – Fraser Institute

- [Chile] Chile’s housing market strengthens – Global Property Guide

- [Dominican Republic ] The Dominican Republic has empty beaches, low costs, and great yields – Global Property Guide

- [Hong Kong] Hong Kong leader Carrie Lam unveils property measures – Reuters

- [Indonesia] Jakarta’s rental yields are moderate to attractive – Global Property Guide

- [Qatar] Qatar’s housing market is gradually improving – Global Property Guide

- [Romania] Moderate to good rental yields in Bucharest, Romania – Global Property Guide

- [Russia] Russia’s house prices are picking up again – Global Property Guide

- [United Kingdom] How far do people move house? – Bank of England

On cross-country:

- Making Sense of Increased Synchronization in Global House Prices – Federal Reserve Bank of Dallas

On the US:

- Housing Market Points to Recession By Election Day – Council on Foreign Relations

- 2019 Cost Burden Report: Half of Renter Households Struggle With Affordability – Apartment List

- Rent control is making a comeback. Does it work?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, October 17, 2019

The link between declining middle-wage jobs, rising wage inequality, and worker welfare

From VOX post by Jennifer Hunt and Ryan Nunn:

“Over the last five decades, middle-wage jobs diminished in the US as wage inequality increased. This column investigates the relationship between these two phenomena, and finds no evidence that either computerisation or automation (often cited as a source of both trends) produced employment polarisation or increased wage inequality. By examining wages at the individual level (rather than occupation-average wages), the column suggests that the evolution of wages can be better explained by distinct causes—ranging from changing labour market institutions to globalisation—than by observable demographic factors.

Middle-wage jobs in the US are gradually diminishing while wage inequality has been rising. But are the two related? Does the decline in middle-wage jobs represent polarisation of employment, and is the decline a good or a bad thing for workers?

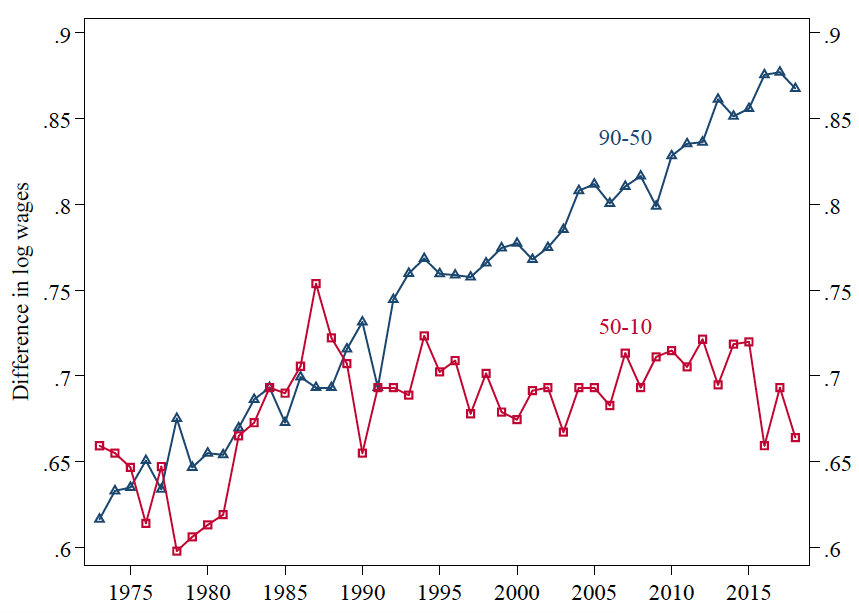

Inequality between top and middle hourly wages has increased steadily for the last 50 years in the US. By contrast, inequality between middle and bottom wages rose sharply in the 1980s; then, after a slight decline, it remained stable for the next 30 years. These gaps are commonly measured as the ratio of the 90th and 50th percentile wages (the wage of the worker earning more than 90% of workers relative to the wage of the worker earning more than 50% of workers) and the ratio of the 50th and 10th percentile wages, as shown in Figure 1.

Note: Difference between 90th and median log hourly wages (90-50) and median and 10th percentile wages (50-10), weighted by weekly hours work. Non-self employed workers 18-64 without missing values for covariates used elsewhere in the paper, but including imputed values.

Source: CPS MORGs 1979-2018 and CPS Mays 1973-1979.Economists have investigated many potential explanations for these changes, including the decline of unions (Fortin et al. 2019); the inflation-adjusted minimum wage (Lee 1999); the spread of outsourcing and temporary-agency labour (Feenstra and Hanson 1999); reduced competition and dynamism (Furman and Orszag 2018, Shambaugh et al. 2018); and increased international trade, off-shoring, and technological progress (Blum 2008, Feenstra and Hanson 2003). The first two factors played an important role in the 1980s, and many researchers believe that technology has played an important role throughout.

A complementary analysis focuses on employment shares of low-, middle-, and high-wage workers rather than wage inequality. One of the most striking findings from this work is that the share of middle-wage jobs has declined. This decline can be measured in different ways, one of which is to examine shifts in the occupational composition of employment. Some research foregrounds the role of technology in its examination of these shifts, because in addition to a decline in the employment share of middle-wage occupations and a rise in employment share of high-wage occupations, the share of low-wage occupation employment share has been rising (e.g. Autor 2015a,b and Autor and Dorn 2013 for the US; Goos et al. 2009 and Goos et al. 2014 for other countries).”

Continue reading here.

From VOX post by Jennifer Hunt and Ryan Nunn:

“Over the last five decades, middle-wage jobs diminished in the US as wage inequality increased. This column investigates the relationship between these two phenomena, and finds no evidence that either computerisation or automation (often cited as a source of both trends) produced employment polarisation or increased wage inequality. By examining wages at the individual level (rather than occupation-average wages), the column suggests that the evolution of wages can be better explained by distinct causes—ranging from changing labour market institutions to globalisation—than by observable demographic factors.

Posted by at 9:18 AM

Labels: Inclusive Growth

Subscribe to: Posts