Thursday, January 4, 2018

GDP growth forecasts and information flows: Is there evidence of overreactions?

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories. In addition to these warnings, further motivation is provided by macroeconomic episodes in which improved economic prospects are followed by crises. For instance, several European economies, among them Greece and Ireland, went through this type of trajectory. Another case is given by recent events in Brazil, where prominent optimism regarding economic prospects was later proven wrong in a stark manner.”

“The empirical analysis shows a significant association between mean forecast errors and earlier information flows. The sign of the documented relationship is consistent with the overreaction hypothesis. More positive information is followed, on average, by higher forecast errors, that is, by increments in the mean difference between forecast growth and realized growth.”

“It is worth noting that the strongest evidence is documented for information flows and forecasts errors that are between 4 and 8 years apart. In other words, the evidence indicates the presence of a process that develops at a frequency that is lower than the usual business cycle frequency.”

“This work documents the presence of systematic errors in growth forecasts. Mean forecast errors are positively associated with the tone of information flows observed in previous periods.”

“The inefficient use of information and the associated errors in decision-making could explain economically significant aggregate fluctuations. In particular, excessive optimism after the arrival of positive information can contribute to the emergence of vulnerabilities that increase the likelihood of economic crises.”

The article is available from the International Finance.

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories.

Posted by at 10:41 AM

Labels: Forecasting Forum

CO2 Emissions in UK

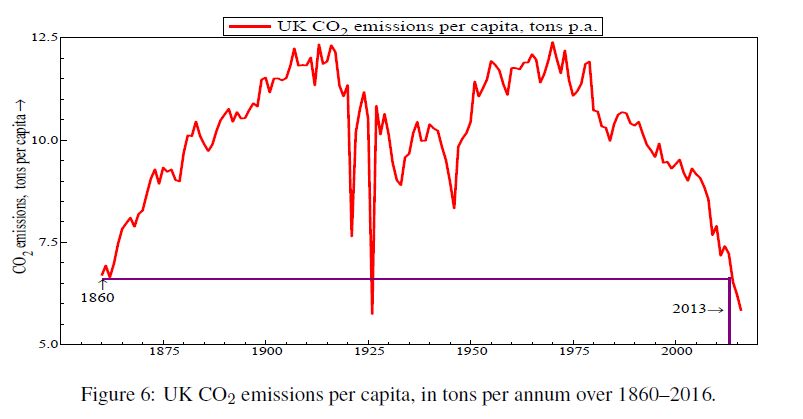

Hendry reports per capita UK CO2 emissions, “which rose considerably till 1916, fluctuated violently till 1950, and have dropped dramatically since 1970” (see Hendry, 2017b).

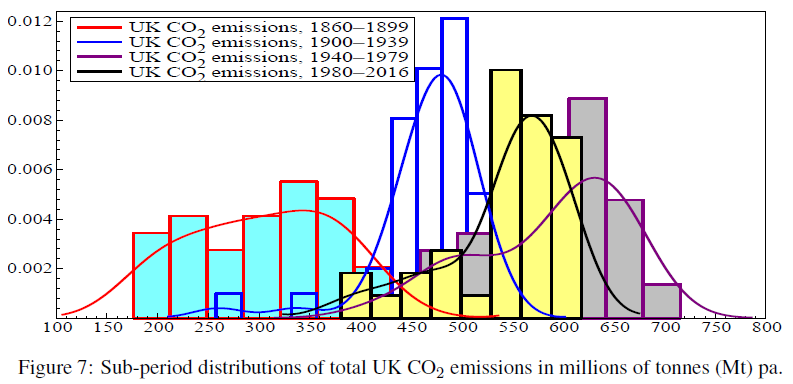

“The sub-period distributions of UK CO2 emissions in [the figure below] illustrate their changes in shape, spread and location.”

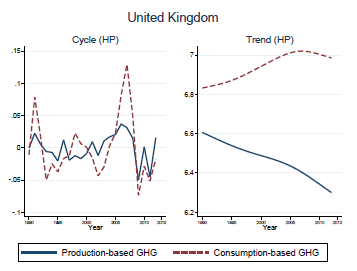

My working paper with Gail Cohen, Joao Jalles and Ricardo Marto shows how production-based emissions and consumption-based emissions differ in the UK. Both the cyclical components and the trend components are shown in the figure below.

Hendry reports per capita UK CO2 emissions, “which rose considerably till 1916, fluctuated violently till 1950, and have dropped dramatically since 1970” (see Hendry, 2017b).

“The sub-period distributions of UK CO2 emissions in [the figure below] illustrate their changes in shape, spread and location.”

My working paper with Gail Cohen, Joao Jalles and Ricardo Marto shows how production-based emissions and consumption-based emissions differ in the UK.

Posted by at 10:37 AM

Labels: Energy & Climate Change

David Hendry on Why Forecasting Fails

The noted econometrician writes: “The intermittent failure of economic forecasts to ‘foresee’ the future reflects both imperfect knowledge and a non-stationary and evolving world that is far from ‘general equilibrium’ and closer to ‘general disequilibrium’.”

“[This has] disastrous consequences for dynamic stochastic general equilibrium (DSGE) systems, which transpire to be the least structural of all possible model forms as their derivation entails they are bound to ‘break down’ when the underlying distributions of economic variables shift. This serious problem is highlighted by Hendry and Muellbauer (2017) in their critique of the Bank of England quarterly econometric model (BEQEM–pronounced Beckem: […] a DSGE which, as in the film ‘Bend it Like Beckham’, bent in the Financial Crisis, but so much that it broke and had to be replaced.”

“Surprisingly, despite that abject failure, it was replaced by yet another DSGE (COMPASS: Central Organising Model for Projection Analysis and Scenario Simulation […]. Unfortunately, […] COMPASS had already failed to characterize data available before it was even developed. Persisting with such an approach introduces a triple whammy as:

a] the derivations sustaining DSGEs use an invalid mathematical basis;

b] imposing a so-called ‘equilibrium’ fails to take account of past shifts;

c] the DSGE approach assumes agents act in the same incorrect way as the modeller, so assumes agents have failed to learn that imperfect knowledge about location shifts forces revisions to their plans.”

“During a visit to LSE in 2009, Queen Elizabeth II asked Luis Garicano “why did no one see the credit crisis coming?” to which a part of his answer should have been that DSGE models dominated economic agencies and essentially ruled out such major financial crises by assuming away imperfect knowledge. Prakash Loungani (2001) argued “The record of failure to predict recessions is virtually unblemished.””

The article is available from the here.

The noted econometrician writes: “The intermittent failure of economic forecasts to ‘foresee’ the future reflects both imperfect knowledge and a non-stationary and evolving world that is far from ‘general equilibrium’ and closer to ‘general disequilibrium’.”

“[This has] disastrous consequences for dynamic stochastic general equilibrium (DSGE) systems, which transpire to be the least structural of all possible model forms as their derivation entails they are bound to ‘break down’ when the underlying distributions of economic variables shift.

Posted by at 10:33 AM

Labels: Forecasting Forum

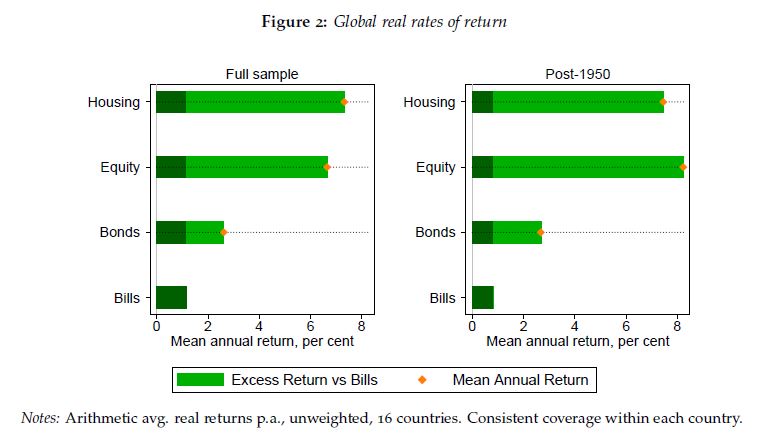

The Rate of Return on Everything: 1870–2015

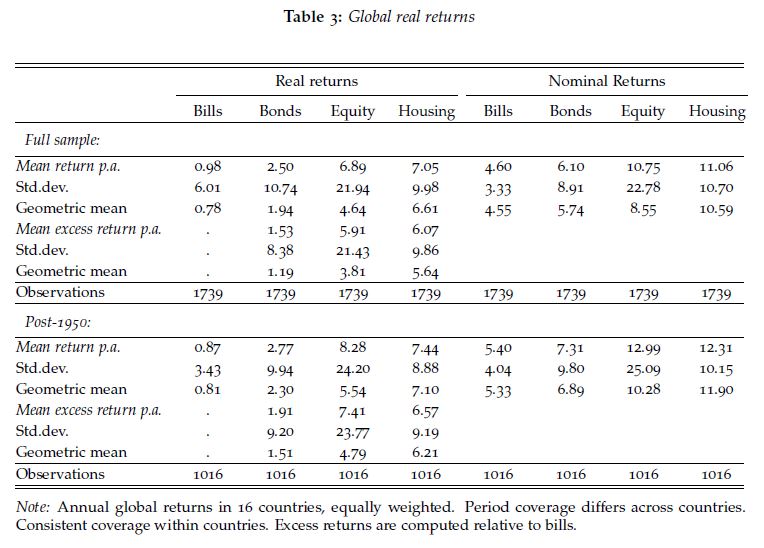

From a new paper by Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor:

“This paper answers fundamental questions that have preoccupied modern economic thought since the 18th century. What is the aggregate real rate of return in the economy? Is it higher than the growth rate of the economy and, if so, by how much? Is there a tendency for returns to fall in the long-run? Which particular assets have the highest long-run returns? We answer these questions on the basis of a new and comprehensive dataset for all major asset classes, including—for the first time—total returns to the largest, but often ignored, component of household wealth, housing. The annual data on total returns for equity, housing, bonds, and bills cover 16 advanced economies from 1870 to 2015, and our new evidence reveals many new insights and puzzles.”

“This paper, perhaps for the first time, investigates the long history of asset returns for all the major categories of an economy’s investable wealth portfolio. Our investigation has confirmed many of the broad patterns that have occupied much research in economics and finance. The returns to risky assets, and risk premiums, have been high and stable over the past 150 years, and substantial diversification opportunities exist between risky asset classes, and across countries. Arguably the most surprising result of our study is that long run returns on housing and equity look remarkably similar. Yet while returns are comparable, residential real estate is less volatile on a national level, opening up new and interesting risk premium puzzles.”

From a new paper by Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor:

“This paper answers fundamental questions that have preoccupied modern economic thought since the 18th century. What is the aggregate real rate of return in the economy? Is it higher than the growth rate of the economy and, if so, by how much? Is there a tendency for returns to fall in the long-run? Which particular assets have the highest long-run returns?

Posted by at 7:34 AM

Labels: Global Housing Watch

Subscribe to: Posts