Monday, December 3, 2018

Per capita income, consumption patterns, and carbon dioxide emissions

From VoxEU:

With global emissions of CO2 still growing, understanding the determinants behind energy use and emissions is as relevant as ever. This column looks at the role of per capita income and consumption choices. It finds that the share of expenditures spent on energy and energy-intensive goods tends to decrease with income across a large set of countries. Simulations indicate that income growth shifts consumption patterns in a way which generally reduces emissions. However, increasing emissions in low- and middle-income countries as well as a shift from direct to indirect consumption of energy mean that the effect on total world emissions is modest.

The consumption of energy is associated with numerous negative externalities. Fossil fuels, specifically, cause emissions of CO2, the most prevalent greenhouse gas. With the issue of climate change far from resolved, understanding the determinants behind emission levels is necessary to improve forecasting and guide policy making.

There is ample empirical evidence that energy demand depends on per capita income. In high-income countries, a number of single-country survey-based studies find that rich households spend a smaller share of their income on energy (e.g. Dubin and McFadden 1984). Less is known about this relationship in the developing world, where most of the growth in energy demand is currently taking place. A number of studies find that energy demand also increases slower than total expenditures in middle-income countries, including in China (e.g. Cao et al. 2016). On the other hand, as large populations are just beginning to purchase energy-intensive appliances (fridges, air conditioners, cars), it is feared that energy demand in the developing world may keep growing rapidly (Auffhammer and Wolfram 2014, Gertler et al. 2016).

More generally, the structural change literature has clearly documented that consumers of different income levels prefer different sets of goods (e.g. Comin et al. 2018), generally shifting from agriculture to manufacturing to services as income grows. Yet we still do not have a clear picture of the aggregate consequences for energy consumption, and what the relationship between income, consumption patterns and CO2 emissions looks like in the aggregate. This relationship directly affects the CO2 intensity of GDP, a critical ingredient when trying to project emissions and understand the potential magnitude of climate change. A quick survey of prominent emission projection models (from academics, governments, or international agencies) also shows that these models tend to incorporate income effects in consumption in a rather crude manner, as they are typically more focused on technology assumptions.

Our recent article (Caron and Fally 2018) systematically summarises the implications of shifting consumption patterns on energy demand and emissions. We take an aggregate view across countries spanning most of the per capita income spectrum and all sectors of the economy. Our framework, an extension of the general equilibrium model described in Caron et al. (2014), links non-homothetic household preferences (i.e. with non-trivial income effects) to emissions through production and trade linkages. The model allows us to uncover patters of comparative advantage in the production of CO2-intensive goods. We can thus identify the role of income in determining energy demand, making sure that we are not confounding it for differences in the availability of energy or energy-intensive goods and services across countries.

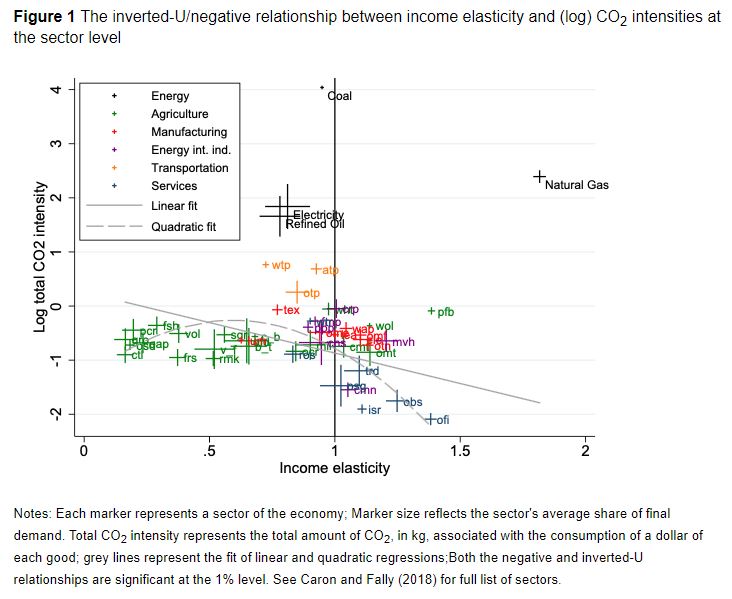

The relationship between income elasticity and emissions intensity across sectors

Do high income consumers prefer goods which are, coincidentally, less CO2 intensive in their production?

Using different types non-homothetic preferences, we estimate the income elasticity of goods in 50 sectors of the economy. As many before us, we find a clear role for per capita income in determining consumption patterns – the income elasticity of most sectors is significantly different from one.

The directconsumption of energy generally increases slower than income. Figure 1 shows that the two main energy goods consumed directly by households, electricity (ely) and refined oil (p_c, mostly gasoline for transportation), have an income elasticity below one. While these estimates reflect an average across all countries, they depend on income – energy consumption is more income-elastic in low-income countries. This is consistent with scattered country-level evidence from the literature.

However, just looking at direct energy consumption is misleading. It ignores the emissions embodied in the consumption of non-energy goods – think of the emissions caused by the production of the steel and leather constituting the chair you are sitting on, and so on. Tracking ‘indirect’ emissions throughout global supply chains (based on intermediate input and trade linkages), we can compute the ‘total’ emissions associated with the consumption of each good. Plotting income elasticity against total (embodied) CO2 intensity, Figure 1 reveals an ‘inverted-U’ relationship – sectors of intermediate income elasticity have, on average, the highest CO2 intensity. But it is also asymmetric and negative overall, with high-income-elasticity sectors having the lowest CO2 requirements on average.

We insist that this represents an ‘incidental’ correlation – high-income consumers do not necessarily prefer these goods becausethey are less emissions intensive.”

Continue reading here.

From VoxEU:

With global emissions of CO2 still growing, understanding the determinants behind energy use and emissions is as relevant as ever. This column looks at the role of per capita income and consumption choices. It finds that the share of expenditures spent on energy and energy-intensive goods tends to decrease with income across a large set of countries. Simulations indicate that income growth shifts consumption patterns in a way which generally reduces emissions.

Posted by at 2:22 PM

Labels: Energy & Climate Change

Friday, November 30, 2018

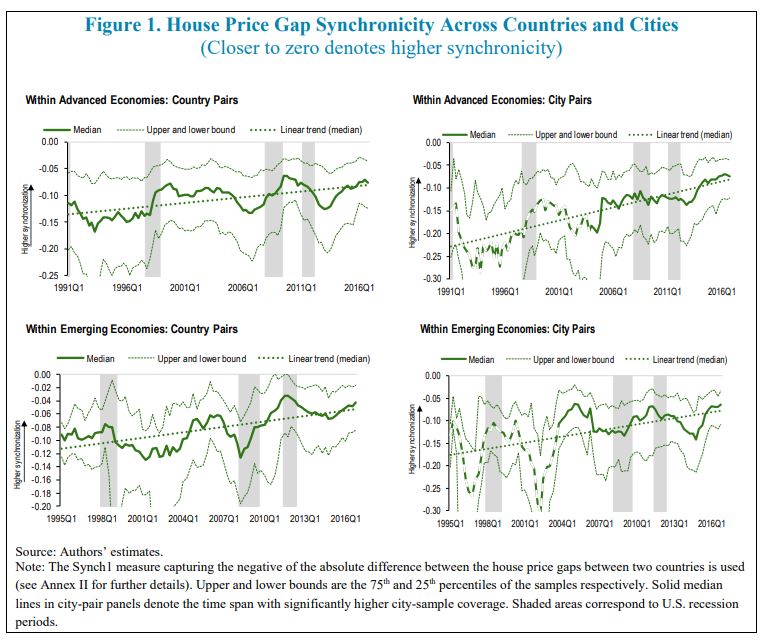

House Price Synchronicity, Banking Integration, and Global Financial Conditions

From a new IMF working paper by Adrian Alter, Jane Dokko, and Dulani Seneviratne:

“We examine the relationship between house price synchronicity and global financial conditions across 40 countries and about 70 cities over the past three decades. The role played by cross-border banking flows in residential property markets is examined as well. Looser global financial conditions are associated with greater house price synchronicity, even after controlling for bilateral financial integration. Moreover, we find that synchronicity across major cities may differ from that of their respective countries’, perhaps due to the influence of global investors on local house price dynamics. Policy choices such as macroprudential tools and exchange rate flexibility appear to be relevant for mitigating the sensitivity of domestic housing markets to the rest of the world.”

From a new IMF working paper by Adrian Alter, Jane Dokko, and Dulani Seneviratne:

“We examine the relationship between house price synchronicity and global financial conditions across 40 countries and about 70 cities over the past three decades. The role played by cross-border banking flows in residential property markets is examined as well. Looser global financial conditions are associated with greater house price synchronicity, even after controlling for bilateral financial integration.

Posted by at 4:13 PM

Labels: Global Housing Watch

Finding Success

From the IMF’s Finance & Development magazine:

“Assaf Razin’s Israel and the World Economy shows that globalization can be a powerful force for economic progress in the case of a country with the institutions and policies to take advantage of the possibilities of an open economy. As depicted in this comprehensive and accessible book, Israel’s strong growth since its stabilization from high inflation in 1985 owes much to an international economy in which capital, labor, and ideas are mobile and in which trade and investment flow readily across far-flung international borders.

Razin explains that where other countries have experienced problems with globalization, Israel has found success. Large capital inflows are understandably viewed as dangerous in emerging markets living with memories of recent currency crises: in Israel foreign capital provided crucial funding for investment in the country’s showcase technology sector. Israel is now solidly established as a high-tech powerhouse—a place where budding venture capitalists from emerging market countries flock to learn how to develop an innovation ecosystem. But the domestic market alone is far too small and homegrown capital formation insufficient to foster that innovation. Globalization has been essential.

Similarly, immigration is a hot-button issue in the United States and in some countries in Europe but a source of growth in Israel. This is because a massive influx of skilled immigrants from the former Soviet Union starting in 1989 led to a surge in productivity, propelling Israel to medium- to high-income status, capped by membership in the Organisation for Economic Co-operation and Development in 2010. And Razin shows that this productivity boom translated into higher wages even for domestic workers who might otherwise have been harmed by the increased labor supply.

There is a sense in which this is three books in one. First, Razin explains the intuition and policy implications of a more globalized world across a range of topics, including migration, inequality, capital flows, currency crises, international trade, and more. The book then connects each topic to developments in the Israeli economy, portraying both successes and challenges in light of the underlying theory. Last, each chapter includes self-contained technical expositions of key models with which to analyze these economic phenomena, making this a text to be considered for a rigorous course on international economic policy.

It is not that Razin thinks Israel has done everything right—far from it. He covers rising inequality within Israeli society, the low participation rates and levels of skills among the fastest-growing segments of the population, the problem of brain drain as highly educated Israelis move abroad, and the costs associated with Israel’s security challenges, including a chapter on the “Rising Cost of Occupation.”

Still, even with Razin’s frankness about the potential pitfalls, his book is an ode to the potential benefits of good economic policy, to economic models through which to examine policy, and to Israel’s astonishing economic success.”

From the IMF’s Finance & Development magazine:

“Assaf Razin’s Israel and the World Economy shows that globalization can be a powerful force for economic progress in the case of a country with the institutions and policies to take advantage of the possibilities of an open economy. As depicted in this comprehensive and accessible book, Israel’s strong growth since its stabilization from high inflation in 1985 owes much to an international economy in which capital,

Posted by at 3:59 PM

Labels: Macro Demystified

Housing View – November 30, 2018

On cross-country:

- There is more to high house prices than constrained supply – Economist

- Pockets of risk in European housing markets – VoxEU

- The real cost of international real estate – Savills

- Rising residential costs help push Hong Kong to the top of the Savills Live/Work Index – Savills

On the US:

- Drivers of the Great Housing Boom-Bust: Credit Conditions, Beliefs, or Both? – NBER

- What The 1990s Tell Us About The Next Housing Bust – Real Estate Decoded

- Ruling mostly clears plan to upzone Seattle neighborhoods for affordable housing – Seattle Times

- A tax break to hasten gentrification? Housing market’s Opportunity Zones may miss their target – Market Watch

- US: Signs of a slowdown? – ING

- Ahead of Amazon’s move to Queens, could buying an apartment count as insider trading? – Quartz

- 81 Percent of Homes in the San Francisco Metro Area Are Worth More Than $1 Million. That’s Not Normal. – Reason

- The U.S. Housing Boom Is Coming to an End, Starting in Dallas – Wall Street Journal

- What Accounts for Recent Growth in Homeowner Households? – Harvard Joint Center for Housing Studies

- 6 ways Washington could make housing more affordable – Politico

- Why a housing project is building hope for the US working poor – Financial Times

- Rent Control Is Making a Comeback. But Is That a Good Idea? – The Pew Charitable Trusts

- House prices have surged, and so will the government’s mortgage obligations – Market Watch

- Why 2019 won’t lead to a home buyer’s market – Market Watch

- Black Homeowners Saw Greater Home Price Appreciation Than Whites in Some Areas – CityLab

- Secret luxury homes: how the ultra-rich hide their properties – Financial Times

On other countries:

- [Australia] Securitisation and the Housing Market – Reserve Bank of Australia

- [Australia] Why Australia may not be the next “big short” – MacroBusiness

- [China] China’s Real Estate Market – NBER

- [Ireland] Why are job numbers soaring despite the housing crisis? – The Irish Times

- [New Zealand] NZ cenbank to ease mortgage curbs but lift bank capital norms – Reuters

- [Puerto Rico] Generadores de 3700 dólares y lavabos de 666 dólares: los sobreprecios de las reparaciones en Puerto Rico – New York Times

- [Singapore] Financial Stability Review 2018 – Monetary Authority of Singapore

- [Sweden] Financial Stability Report 2018:02 – Sveriges Riksbank

- [Sweden] Swedish housing market starting to crumble – Variant Perception

- [United Kingdom] The case for scrapping stamp duty – Economist

- [United Kingdom] Lending relationships and the collateral channel – Bank of England

- [United Kingdom] Brexit effect ‘limited’ on UK house prices – Financial Times

- [United Kingdom] BOE Warns Disorderly Brexit May Halve Commercial-Property Prices – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- There is more to high house prices than constrained supply – Economist

- Pockets of risk in European housing markets – VoxEU

- The real cost of international real estate – Savills

- Rising residential costs help push Hong Kong to the top of the Savills Live/Work Index – Savills

On the US:

- Drivers of the Great Housing Boom-Bust: Credit Conditions,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts