Thursday, May 10, 2018

Remittances and labor market outcomes in LICs, MICs and Fragile States

From a new IMF working paper by Ralph Chami, Ekkehard Ernst, Connel Fullenkamp, and Anne Oeking”

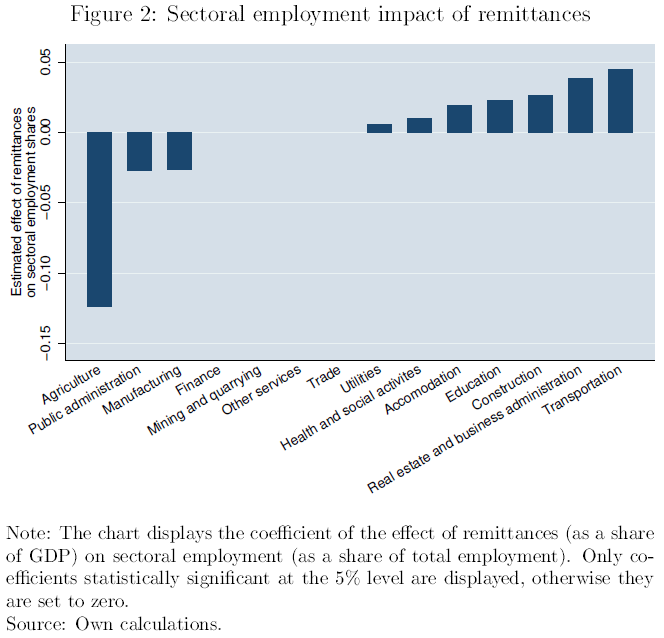

“We present cross-country evidence on the impact of remittances on labor market outcomes. Remittances appear to have a strong impact on both labor supply and labor demand in recipient countries. These effects are highly significant and greater in size than those of foreign direct investment or offcial development aid. On the supply side, remittances reduce labor force participation and increase informality of the labor market. In addition, male and female labor supply show significantly different sensitivities to remittances. On the demand side, remittances reduce overall unemployment but benefit mostly lower-wage, lower-productivity nontradables industries at the expense of high-productivity, high-wage tradables sectors. As a consequence, even though inequality declines as a result of larger remittances, average wage and productivity growth declines, the latter more strongly than the former leading to an increase in the labor income share. In fragile states, in contrast, remittances impose a positive externality, possibly because the tradables sector tends to be underdeveloped. Our findings indicate that reforms to foster inclusive growth need to take into account the role of remittances in order to be successful.”

From a new IMF working paper by Ralph Chami, Ekkehard Ernst, Connel Fullenkamp, and Anne Oeking”

“We present cross-country evidence on the impact of remittances on labor market outcomes. Remittances appear to have a strong impact on both labor supply and labor demand in recipient countries. These effects are highly significant and greater in size than those of foreign direct investment or offcial development aid. On the supply side, remittances reduce labor force participation and increase informality of the labor market.

Posted by at 11:30 AM

Labels: Inclusive Growth

What Drives Labor and Product market Reforms in Advanced Countries?

A new IMF working paper by Romain A Duval Davide Furceri, and Jakob Miethe find “widespread support for the crisis-induces-reform hypothesis. Reforms are also more likely to happen when other countries undertake them or there is formal pressure to implement them. Other robust correlates are more specific to certain areas—for example, political factors are most relevant for job protection reforms.”

“High unemployment, recession and/or an open economic crisis tend to be associated with a greater likelihood of reform. The effect is economically significant. For example, an increase of 10 percentage points in unemployment (as seen in several European economies in the aftermath of the Great Recession) is associated with an increase in the probability to undertake a major EPL reform for regular contract of about 5 percentage points — that is, about twice the average probability in the sample.”

“[…] outside pressure increases the likelihood of reform in certain areas. Reforms are more likely when other countries also undertake them and when there is formal pressure: many product market reforms in EU countries have occurred during their accession process, and competition-relevant EU directives have also been an important factor behind deregulation.”

A new IMF working paper by Romain A Duval Davide Furceri, and Jakob Miethe find “widespread support for the crisis-induces-reform hypothesis. Reforms are also more likely to happen when other countries undertake them or there is formal pressure to implement them. Other robust correlates are more specific to certain areas—for example, political factors are most relevant for job protection reforms.”

“High unemployment, recession and/or an open economic crisis tend to be associated with a greater likelihood of reform.

Posted by at 11:22 AM

Labels: Inclusive Growth

Lawrence R. Klein and the making of large-scale macro-econometric modeling, 1938-1955

From new Documentos CEDE by Erich Pinzón-Fuchs:

“Lawrence R. Klein was the father of macro-econometric modeling, the scientific practice that dominated macroeconomics throughout the second half of the twentieth century. Therefore, understanding how Klein developed his identity as a macro-econometrician and how he conceived and forged macro-econometric modeling at the same time, is essential to draw a clear picture of the origins and subsequent development of this scientific practice in the United States. To this aim, I focus on Klein’s early trajectory as a student of economics and as an economist (from 1938-1955), and I particularly examine the extent to which the people and institutions Klein encountered helped him shape his professional identity. Klein’s experience at places like Berkeley, MIT, Cowles, and the University of Michigan, as well as his early acquaintance with people such as Griffith Evans, Paul Samuelson, and Trygve Haavelmo were decisive in the formation of his idea on how econometrics, expert knowledge, mathematical rigor, and a specific institutional configuration should enter macro-econometric modeling. Although Klein’s identity defined some of the most important characteristics of this practice, by the end of the 1950s, macro-econometric modeling became a scientific practice independent of Klein’s enthusiasm and with a “life of its own,” ready to be further developed and adapted to specific contexts by the community of macroeconomists.” Picture from Nobelprize.org.

Picture from Nobelprize.org.

From new Documentos CEDE by Erich Pinzón-Fuchs:

“Lawrence R. Klein was the father of macro-econometric modeling, the scientific practice that dominated macroeconomics throughout the second half of the twentieth century. Therefore, understanding how Klein developed his identity as a macro-econometrician and how he conceived and forged macro-econometric modeling at the same time, is essential to draw a clear picture of the origins and subsequent development of this scientific practice in the United States.

Posted by at 10:50 AM

Labels: Forecasting Forum, Profiles of Economists

Macroeconomic Forecasting in Germany has changed after the Great Recession?

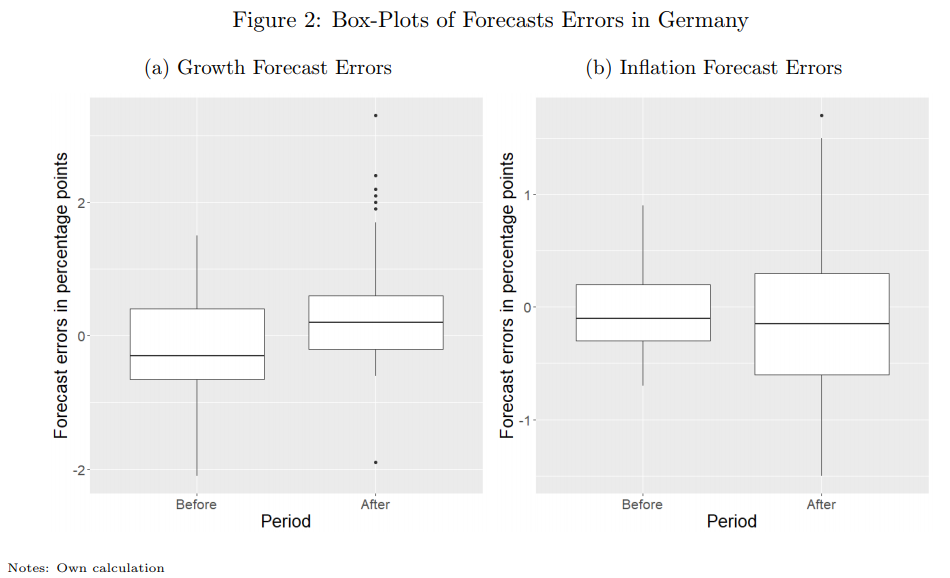

From a new paper by Jörg Döpke, Ulrich Fritsche, and Karsten Müller:

“Based on a panel of annual data for 17 growth and inflation forecasts from 14 institutions for Germany, we analyse forecast accuracy for the periods before and after the Great Recession, including measures of directional change accuracy based on Receiver Operating Curves (ROC). We find only small differences on forecast accuracy between both time periods. We test whether the conditions for forecast rationality hold in both time periods. We document an increased crosssection variance of forecasts and a changed correlation between inflation and growth forecast errors after the crisis, which might hint to a changed forecaster behaviour. This is also supported by estimated loss functions before and after the crisis, which suggest a stronger incentive to avoid overestimations (growth) and underestimations (inflation) after the crisis. Estimating loss functions for a 10—year rolling window also reveal shifts in the level and direction of loss asymmetry and strengthens the impression of a changed forecaster behaviour after the Great Recession.”

From a new paper by Jörg Döpke, Ulrich Fritsche, and Karsten Müller:

“Based on a panel of annual data for 17 growth and inflation forecasts from 14 institutions for Germany, we analyse forecast accuracy for the periods before and after the Great Recession, including measures of directional change accuracy based on Receiver Operating Curves (ROC). We find only small differences on forecast accuracy between both time periods. We test whether the conditions for forecast rationality hold in both time periods.

Posted by at 10:43 AM

Labels: Forecasting Forum

Wednesday, May 9, 2018

GDP Growth Rate Projection in Asia Pacific

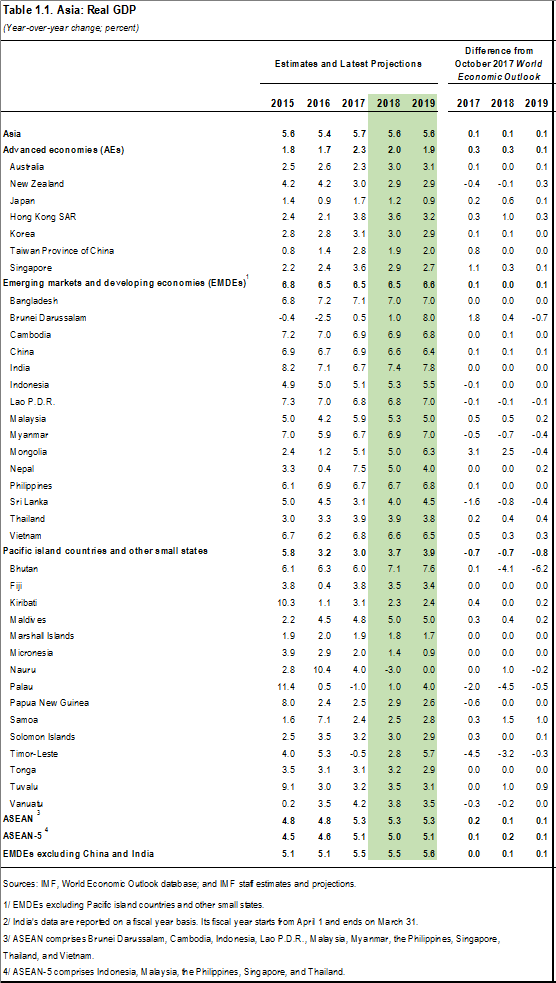

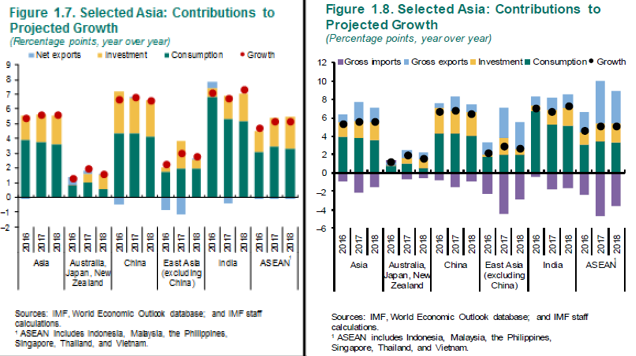

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6). Consumption and investment continue to be major contributors. The contribution of net exports remained small, but the strong growth of gross exports and imports suggests that the recovery in external demand (both inside and outside the region) was an important driver of GDP growth in Asia (Figures 1.7 and 1.8).”

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6).

Posted by at 3:46 PM

Labels: Forecasting Forum

Subscribe to: Posts