Wednesday, May 30, 2018

Forecasting Forum – May 2018

Europe’s future: The value of an institutional economics perspective – VOXEU

Spring 2018 Economic Forecast: Expansion to continue, amid new risks – European Commission

A Brief Analysis of the Central America and the Caribbean Economy – Focus Economics

The yield curve and the stock market: Mind the long run – VOXEU

Expansion to continue amid new risks – VOXEU

Economic Snapshot for the G7 Countries – Focus Economics

Retail Apocalypse Postponed Not Cancelled – Conference Board

Biggest fear for world growth is fear itself as markets fret – Bloomberg Quint

Exchange rate forecasting on a napkin – Unassuming Economist

Europe’s future: The value of an institutional economics perspective – VOXEU

Spring 2018 Economic Forecast: Expansion to continue, amid new risks – European Commission

A Brief Analysis of the Central America and the Caribbean Economy – Focus Economics

The yield curve and the stock market: Mind the long run – VOXEU

Expansion to continue amid new risks – VOXEU

Economic Snapshot for the G7 Countries – Focus Economics

Retail Apocalypse Postponed Not Cancelled – Conference Board

Biggest fear for world growth is fear itself as markets fret – Bloomberg Quint

Exchange rate forecasting on a napkin – Unassuming Economist

Posted by at 10:42 AM

Labels: Forecasting Forum

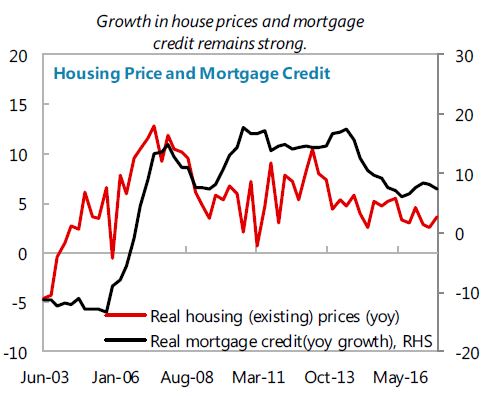

House Prices in Colombia

From the IMF’s latest report on Colombia:

Posted by at 9:40 AM

Labels: Global Housing Watch

Exchange rate forecasting on a napkin

From a new ECB working paper:

“The international finance literature has documented two important regularities in foreign exchange markets. First, there is ample evidence that, for developed countries, real exchange rates are reverting to the level implied by the Purchasing Power Parity (PPP) theory. Second, for flexible currency regimes the adjustment process is mainly driven by the nominal exchange rate. At the same time most of the recent articles remain skeptical that one can outperform the random walk (RW) in nominal exchange rate forecasting.

In this paper we claim that the two above in-sample regularities of foreign exchange markets can be exploited to infer out-of-sample movements of major currency pairs. To prove this thesis we proceed as follows:

- We begin by presenting robust (in-sample) evidence that, for major currency pairs, long-run PPP holds and that the nominal exchange rate is the main driver of this adjustment process.

- We then evaluate a battery of models that aim to exploit these in-sample regularities for forecasting purposes. The winner of the forecasting race is a calibrated PPP model, which just assumes that the real exchange rate gradually returns to its sample mean, completing half of the adjustment in 3 years, and that the adjustment is only driven by the nominal exchange rate. This approach is so simple that it can be implemented even on the back of a napkin in two steps. Step 1 consists in calculating the initial real exchange rate misalignment with an eyeball estimate of what is the distance from the sample mean. Step 2 consists in recalling that, according to this model, one tenth of the required adjustment is achieved by the nominal exchange rate in the first 6 months, one fifth in one year, just over a third in two years and exactly half after 3 years.

- We highlight that severe problems arise when attempting to carry out more sophisticated approaches, such as estimating the pace of mean reversion of the real exchange rate or forecasting relative inflation. Among the estimated approaches, we find that it is strongly preferable to rely on direct rather than multi-step iterative forecasting methods. We also find that models estimated with panel data techniques perform only marginally better than those based on individual currency pairs. This finding has bittersweet implications. On the negative side, estimated models encounter a second formidable competitor that, like the RW, bypasses the estimation error problem. On the positive side, the HL model is more acceptable than the RW from the perspective of economic theory.

- This analysis highlights also that equilibrium exchange rate analysis matters. Simple measures of exchange rate disequilibria, not only signal economic imbalances, but also provide hints in which direction the exchange rate will go.

Our paper has an important message for policymakers. For advanced countries, it is better to rely on the concept of long-run PPP rather than on the RW.”

From a new ECB working paper:

“The international finance literature has documented two important regularities in foreign exchange markets. First, there is ample evidence that, for developed countries, real exchange rates are reverting to the level implied by the Purchasing Power Parity (PPP) theory. Second, for flexible currency regimes the adjustment process is mainly driven by the nominal exchange rate. At the same time most of the recent articles remain skeptical that one can outperform the random walk (RW) in nominal exchange rate forecasting.

Posted by at 9:32 AM

Labels: Forecasting Forum, Macro Demystified

Tuesday, May 29, 2018

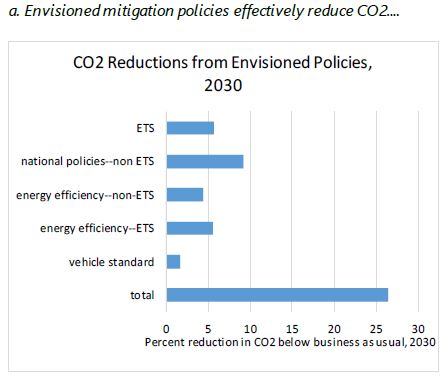

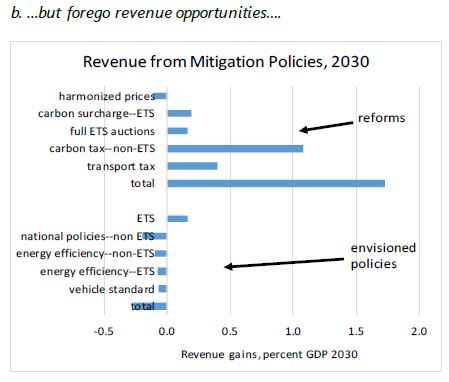

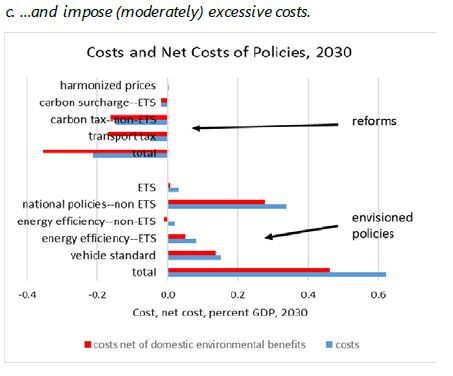

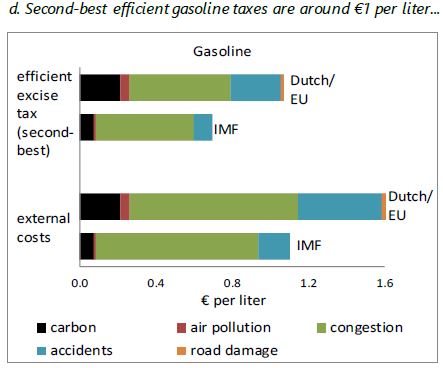

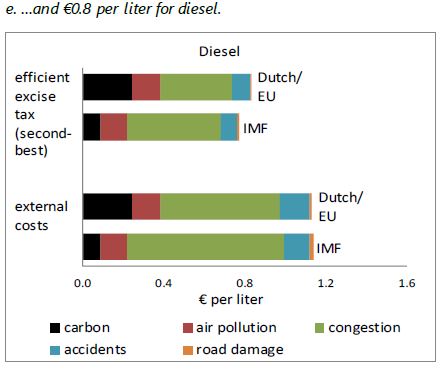

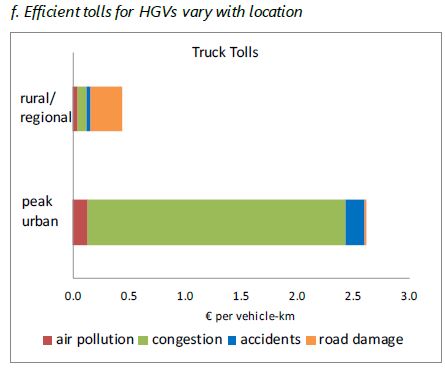

Options for Carbon Mitigation and Transportation Policy in the Netherlands

From the IMF’s latest report on the Netherlands:

“The new Dutch government fully embraced the Paris Climate Agreement and committed to an ambitious climate change policy. The European Union (EU) has pledged to reduce CO2 and other greenhouse gases (GHGs) by 40 percent relative to 1990 levels by 2030. The Netherlands is planning to go further, increasing its own GHG reduction target for 2030 to 49 percent below 1990 levels. Existing policies designed to meet the EU pledge include: (i) the EU Emissions Trading System (ETS) reducing power generation and large industrial emissions 43 percent below 2005 levels by 2030; (ii) national-level targets for non-ETS emissions—for the Netherlands a 36 percent reduction below 2005 levels by 2030;2 (iii) EU goals for energy efficiency (a 30 percent improvement by 2030) and renewables;3 and (iv) EU standards for vehicle CO2 emission rates. The new government agreement contains substantial policy measures to cost-effectively reduce emissions including: introducing a minimum price for CO2 emissions from power generation on top of the ETS; shifting taxes off electricity and onto gas generation; phasing out coal plants and natural gas for new buildings by 2030; subsidizing carbon capture and storage (CCS); and expanding offshore wind power.

The Dutch authorities are also considering major reforms to transportation policy to complement emission reduction efforts and to address other environmental costs. These reforms include full penetration of electric vehicles into the new car fleet by 2030; adoption of km-based (i.e., distance-based) taxation for HGVs; stiffer penalties to deter dangerous driving; and infrastructure upgrades to alleviate traffic congestion. The first policy will progressively erode traditional revenue sources from LDVs—fuel taxes and CO2-related vehicle taxes—posing the question of what revenue-raising instruments could replace them.”

From the IMF’s latest report on the Netherlands:

“The new Dutch government fully embraced the Paris Climate Agreement and committed to an ambitious climate change policy. The European Union (EU) has pledged to reduce CO2 and other greenhouse gases (GHGs) by 40 percent relative to 1990 levels by 2030. The Netherlands is planning to go further, increasing its own GHG reduction target for 2030 to 49 percent below 1990 levels. Existing policies designed to meet the EU pledge include: (i) the EU Emissions Trading System (ETS) reducing power generation and large industrial emissions 43 percent below 2005 levels by 2030;

Posted by at 5:48 PM

Labels: Energy & Climate Change

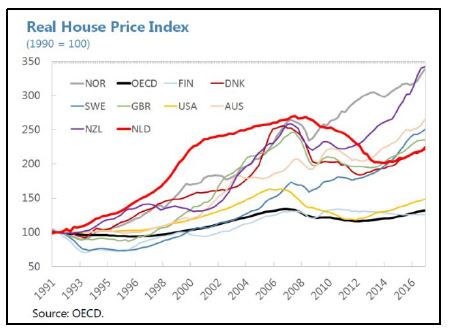

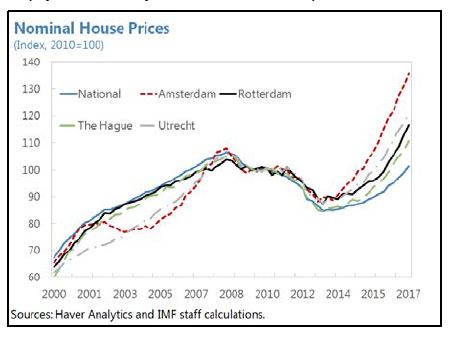

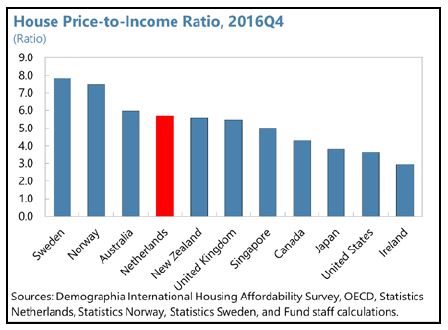

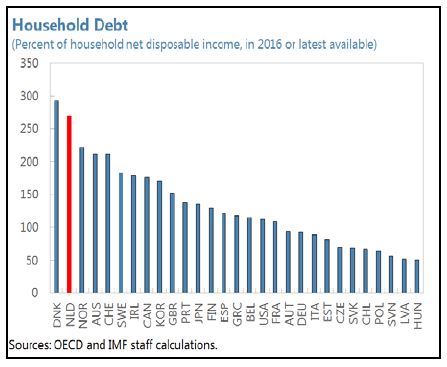

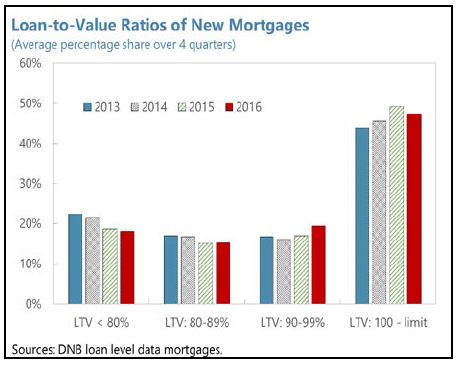

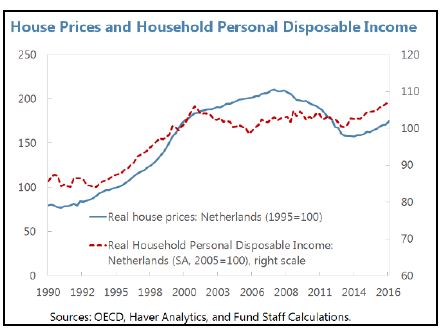

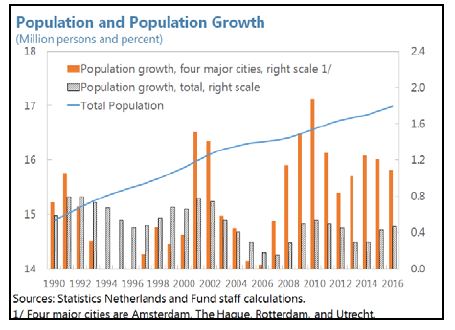

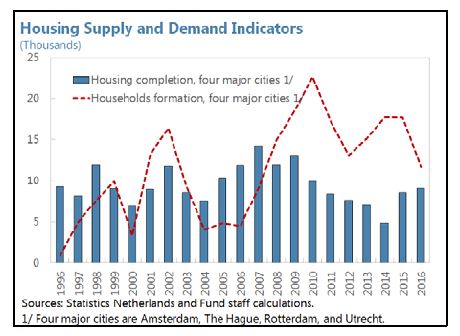

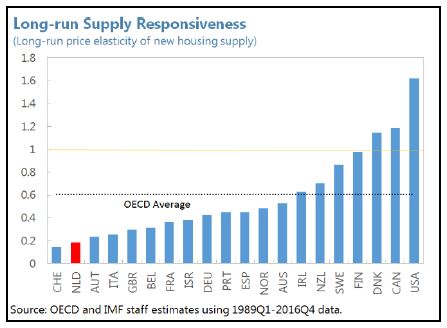

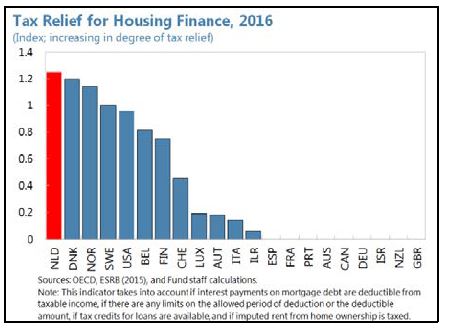

Fundamental Drivers of House Prices in the Netherlands? A Cross-Country Analysis

The latest IMF report on the Netherlands says that:

- “In sum, apart from the conventional fundamental demand and supply factors, the interaction of various institutional and structural factors seems to have contributed significantly to high and rapidly rising house prices in the Netherlands. The large direct and indirect subsidies for social housing and the highly regulated rental market is likely skewing housing needs and use in the Netherlands. The coexistence of a well-developed mortgage market and large tax preferences for owner-occupied housing and mortgage debt seems to have further fueled the surge in demand for homeownership and household debt. In addition, the sluggish response of housing supply exacerbated the situation by failing to cushion the impact of demand pressures.”

- “Overvalued house prices and elevated household debt are a source of vulnerability in the Netherlands in view of the importance of the housing market to both financial and macroeconomic stability. The recent house-price cycle left the Netherlands with elevated level of household debt and a significant share of underwater mortgages. While households have started to deleverage gradually from the record debt levels over the past years, a large correction of house prices, driven by slower real income growth, a reverse in sentiment, or interest rate hikes could weaken household balance sheets further and depress private demand, and in turn adversely affect corporate and bank earnings.”

- “The authorities have been vigilant about the risks and have introduced a series of measures to target the owner-occupied housing sector and strengthen the resilience of banks and households, including additional bank capital buffer requirements in line with Basel III/CRD IV, an introduction of LTV and debt service-to-income (DSTI) caps since 2013, a gradual reduction of LTV limit for mortgages to 100 percent by 2018, a tax exemption for gifts used for housing down payments or mortgage repayments, allowing MID only for new fully amortizing loans, and a gradual reduction of the maximum tax rate allowed for MID from 52 percent in 2013 to 38 percent in 2042 in steps of ½ percent per year.”

- “Nevertheless, further and comprehensive reforms are needed to address the risks from the housing market and enhance the macro-financial resilience of the economy. A stable housing market (without pronounced boom-bust cycles) would contribute to smoother economic development. It is critical that policies work together to fundamentally address housing market imbalances that pose risks to stability and growth and hinder labor mobility:”

The latest IMF report on the Netherlands says that:

- “In sum, apart from the conventional fundamental demand and supply factors, the interaction of various institutional and structural factors seems to have contributed significantly to high and rapidly rising house prices in the Netherlands. The large direct and indirect subsidies for social housing and the highly regulated rental market is likely skewing housing needs and use in the Netherlands. The coexistence of a well-developed mortgage market and large tax preferences for owner-occupied housing and mortgage debt seems to have further fueled the surge in demand for homeownership and household debt.

Posted by at 5:32 PM

Labels: Global Housing Watch

Subscribe to: Posts