Friday, June 8, 2018

Housing View – June 8, 2018

On cross-country:

- Western Cities Want to Slow Flood of Chinese Home Buying. Nothing Works. – Wall Street Journal

- International comparisons of mortgage markets, part II – Rutgers Center for Real Estate

- A Guide to Some of My Blog Posts, Hither and Yon – Steve Malpezzi

- Residential investment and economic activity: evidence from the past five decades – Bank for International Settlements

- Q1 2018: Strong house price rises continue in Europe, US and parts of Asia – Global Property Guide

- Book Review: Municipal Dreams: The Rise and Fall of Social Housing, by John Boughton – Financial Times

- Affordable housing solutions in pipes, containers and 3D printers – Reuters

- The financing of renovation in the social housing sector: A comparative study in 6 European countries – Housing Europe

- Why loan-to-value matters when you shop for a mortgage – Financial Times

- Blackstone remains global king of property funds – Financial Times

On the US:

- Can a new mayor fix San Francisco’s housing and homelessness problems? – Economist

- The Political and Policy Conundrum of Rent Control – Zillow

- A First Look at the Tax Cut and Jobs Act, the Economy, and Real Estate – Steve Malpezzi

- The Death of the Small Apartment Building – Bloomberg

- Why reducing urban traffic congestion can help the American middle class – London School of Economics

- California’s emigrants aren’t all moving to cheaper housing markets – MarketWatch

- After Years of Disinvestment, City Public Housing Is Poised to Get U.S. Oversight – New York Times

- In Vancouver, a Housing Frenzy That Even Owners Want to End – New York Times

- Los Angeles tenants increasingly engaging in rent strikes amid housing crisis – Washington Post

- Strategies for Responding to Gentrification – Harvard Joint Center for Housing Studies

- The Sharing Economy and Housing Affordability: Evidence from Airbnb – SSRN

- The Latest HUD Proposal Would Exacerbate the Housing Insecurity Crisis – Center for American Progress

- Shifting the risk of mortgage defaults from taxpayers to investors – Brookings

- Home Value Forecast: Does Quality of School System Impact Home Prices? – Pro Teck

- Housing Was Undersupplied during the Great Housing Bubble – George Mason University

- Response to the Federal Housing Finance Agency Request for Comment on How Its Regulations May Be Made More Effective and Less Burdensome – George Mason University

- Underwriting Loosening for Conventional Conforming Loans – CoreLogic

- Booming cities, unintended consequences – McKinsey

- S. house prices to rise at twice the speed of inflation and pay: Reuters poll – Reuters

- ‘YIMBY’ call to build more housing divides booming San Francisco – Reuters

- Red Tape Is What Keeps Housing Unaffordable – Foundation For Economic Education

- Boston’s housing market, in three charts – Urban Institute

- The Tight Housing Supply Is Raising Prices – Wall Street Journal

- Seattle Declares War on Workers With Wage and Housing Regulations – Mises Institute

- S. Home Flipping Rate Matches Six-Year High in Q1 2018 – ATTOM

On other countries:

- [Australia] Australia’s House Prices Retreat Appears Entrenched – Wall Street Journal

- [Canada] OPINION: All three major parties ignore real solutions to Ontario’s housing crunch – Toronto Sun

- [Canada] Steel and Aluminum Tariffs Could Leave Canada’s Housing Sector on Shakier Foundation – Wall Street Journal

- [China] Luxury Real Estate Comes to Urban Chinatowns – Wall Street Journal

- [China] China pushes state banks into home rental market at their own risk – Reuters

- [Denmark] Danish non-profit social housing and mortgage institutes – a common stand on future financial regulation – European Covered Bond Council

- [France] Airbnb: The home-sharing site’s number one destination is Paris, where it stands accused of driving up rents and house prices – Financial Times

- [Germany] Germany to toughen laws to stem steep rent hikes – Reuters

- [Ireland] Home mortgage debt outstanding legacy of Ireland’s financial crisis – Reuters

- [Ireland] Ireland’s housing crisis – The case for a European cost rental model – Nevin Economic Research Institute

- [Netherlands] Exploding house prices and imploding affordability in urban housing markets – Rabobank

- [Norway] Strong Norway house prices fuel August or September rate hike view – Reuters

- [United Kingdom] ‘Reform land valuation’ call to unlock housing plots in the UK – Financial Times

- [United Kingdom] Brexit puts a ceiling on London housing demand, prices – Reuters poll – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Western Cities Want to Slow Flood of Chinese Home Buying. Nothing Works. – Wall Street Journal

- International comparisons of mortgage markets, part II – Rutgers Center for Real Estate

- A Guide to Some of My Blog Posts, Hither and Yon – Steve Malpezzi

- Residential investment and economic activity: evidence from the past five decades – Bank for International Settlements

- Q1 2018: Strong house price rises continue in Europe,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 7, 2018

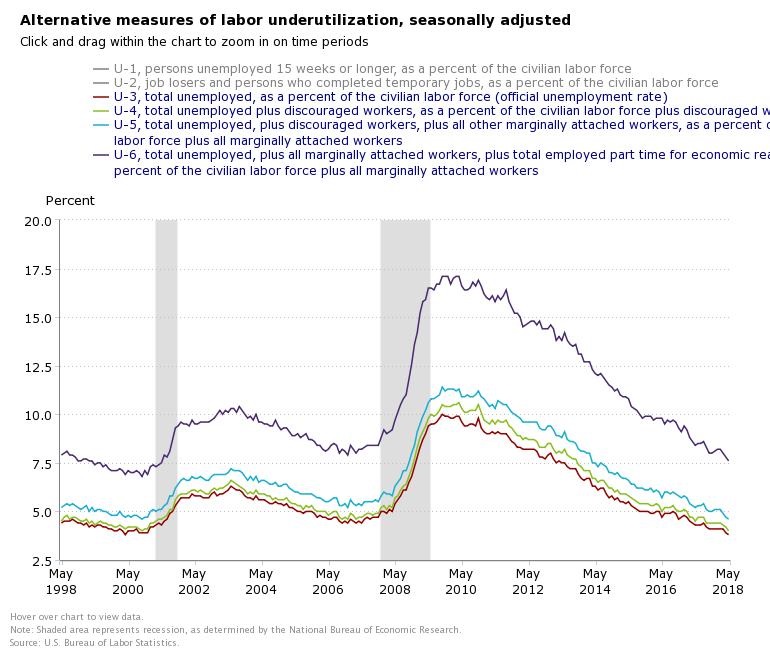

Snapshots of the Salubrious US Labor Market

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

Posted by at 10:18 AM

Labels: Inclusive Growth

Wednesday, June 6, 2018

Housing Market in Romania

The IMF’s latest report on Romania says that:

- “Notwithstanding these improvements, vulnerabilities arise from the high exposure of banks to the real estate sector and sovereign debt. Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program, which allows loan-to-value ratios up to 95 percent. The Romanian banking system has also a large exposure to their own sovereign debt (one of the highest in the EU at around 20 percent of assets in 2017), that could lead to valuation losses in the event of interest rate increases. Finally, despite declining considerably since 2011, about 35 percent of banks’ liabilities and assets remain denominated in foreign exchange (FX), and FX liquidity risks can exist within an environment of ample overall liquidity.”

- “A Debt-Service-to-Income (DSTI) limit on mortgage lending would mitigate risks from the exposure of banks to the real estate sector. An appropriately set DSTI limit can boost borrowers’ resilience and should be imposed on all mortgages, including those made under

the Prima Casa program. In this context, staff welcomed the government’s strategy to gradually scale back the program.”

The IMF’s latest report on Romania says that:

- “Notwithstanding these improvements, vulnerabilities arise from the high exposure of banks to the real estate sector and sovereign debt. Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program,

Posted by at 10:12 PM

Labels: Global Housing Watch

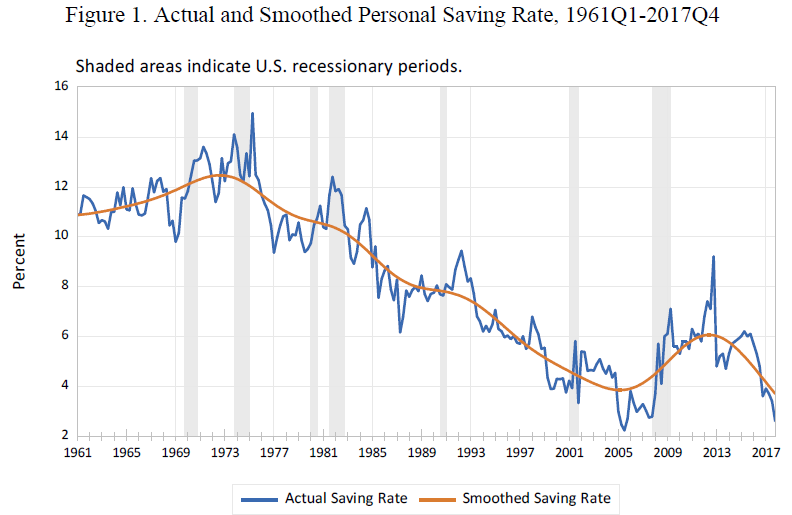

The U.S. Personal Saving Rate

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income, employment

and net worth recovered. Assuming that the real growth in these determinants remains strong, the estimated model predicts continued negative pressures on the current account deficit and further external imbalances attributable to the U.S. household sector.”

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income,

Posted by at 1:35 PM

Labels: Inclusive Growth, Macro Demystified

Financial Stability and Inequality: A Challenge for Macroprudential Regulation

From a new post by Pierre Monnin:

“Theoretical analyses and recent empirical evidence support the hypothesis that increasing inequality can pave the way to financial instability. Considering these results, central banks and financial regulators should keep a close watch on income and wealth distributions in their countries. They should be particularly attentive to a simultaneous rise in inequality and aggregate debt. They might also consider including inequality in their sets of early warning indicators for financial crises.”

“Central banks and financial regulators should also carefully consider the potential feedback loops between their macroprudential policy, inequality and financial stability. Some measures aimed at strengthening financial stability might increase inequality, and thus impede their initial goals. In such a case, central banks and financial regulators, perhaps in collaboration with fiscal authorities, could consider accompanying measures to mitigate the impact of macroprudential measures on inequality. When facing the choice between two policies with the same impact on financial stability, they should prefer the option that does not lead to higher inequality (or increases it the least) to avoid or reduce the side effects of higher inequality on financial stability. Finally, in accordance with their mandate regarding financial stability, central banks and financial regulators may have some reasons to support policies, e.g. fiscal policies, that mitigate the impact of inequality on financial stability.”

From a new post by Pierre Monnin:

“Theoretical analyses and recent empirical evidence support the hypothesis that increasing inequality can pave the way to financial instability. Considering these results, central banks and financial regulators should keep a close watch on income and wealth distributions in their countries. They should be particularly attentive to a simultaneous rise in inequality and aggregate debt. They might also consider including inequality in their sets of early warning indicators for financial crises.”

Posted by at 1:32 PM

Labels: Inclusive Growth

Subscribe to: Posts