Monday, June 18, 2018

House Prices in Switzerland

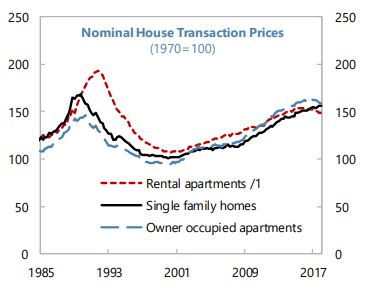

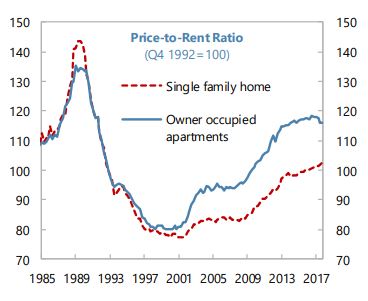

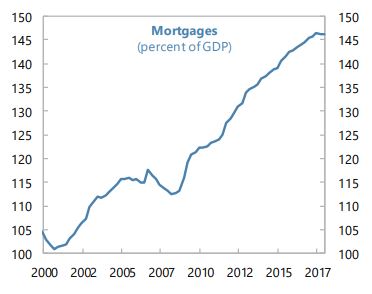

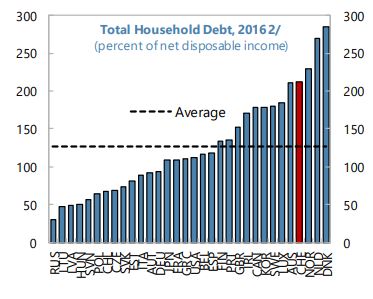

The IMF’s latest report on Switzerland says that:

“Private sector leverage and real estate exposure is high. The growth rate of mortgage claims has slowed from a high base, but these claims increase by about 5 percentage points of GDP per year. Liquidity and capital of domestically-focused banks exceed regulatory minima, and profits have held up despite narrowing interest spreads. Following a series of macroprudential tightening measures during 2012–14, property prices subsequently stabilized, but have risen again recently alongside moderating mortgage interest rates. Reflecting their status as attractive global cities and internationally-traded assets, property prices in Geneva and Zurich have been among the fastest growing in the world. However, standard housing-price metrics do not indicate significant misalignment. Newer-vintage mortgages appear riskier, with nearly half exceeding indicative affordability thresholds and also carrying higher loan-to-value ratios, especially those for purchasing

investment properties.”

The IMF’s latest report on Switzerland says that:

“Private sector leverage and real estate exposure is high. The growth rate of mortgage claims has slowed from a high base, but these claims increase by about 5 percentage points of GDP per year. Liquidity and capital of domestically-focused banks exceed regulatory minima, and profits have held up despite narrowing interest spreads. Following a series of macroprudential tightening measures during 2012–14, property prices subsequently stabilized,

Posted by at 10:08 AM

Labels: Global Housing Watch

Friday, June 15, 2018

What makes a country good at football?

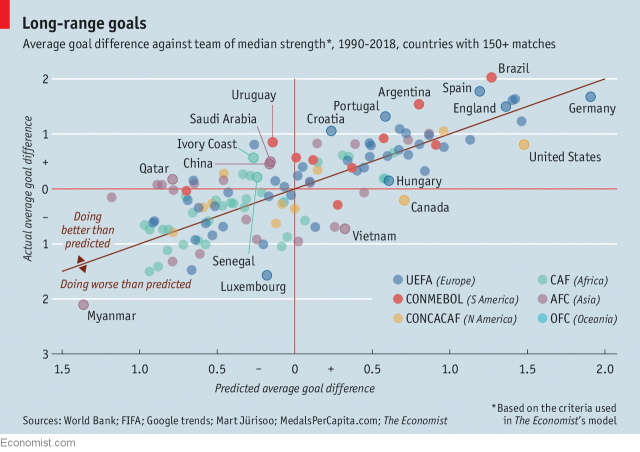

From a new article from the The Economist:

“The Economist has built a statistical model to identify what makes a country good at football. Our aim is not to predict the winner in Russia, which can be done best by looking at a team’s recent results or the calibre of its squad. Instead we want to discover the underlying sporting and economic factors that determine a country’s footballing potential—and to work out why some countries exceed expectations or improve rapidly. We take the results of all international games since 1990 and see which variables are correlated with the goal difference between teams.” “Our model explains 40% of the variance in average goal difference for these teams.”

From a new article from the The Economist:

“The Economist has built a statistical model to identify what makes a country good at football. Our aim is not to predict the winner in Russia, which can be done best by looking at a team’s recent results or the calibre of its squad. Instead we want to discover the underlying sporting and economic factors that determine a country’s footballing potential—and to work out why some countries exceed expectations or improve rapidly.

Posted by at 10:37 AM

Labels: Forecasting Forum

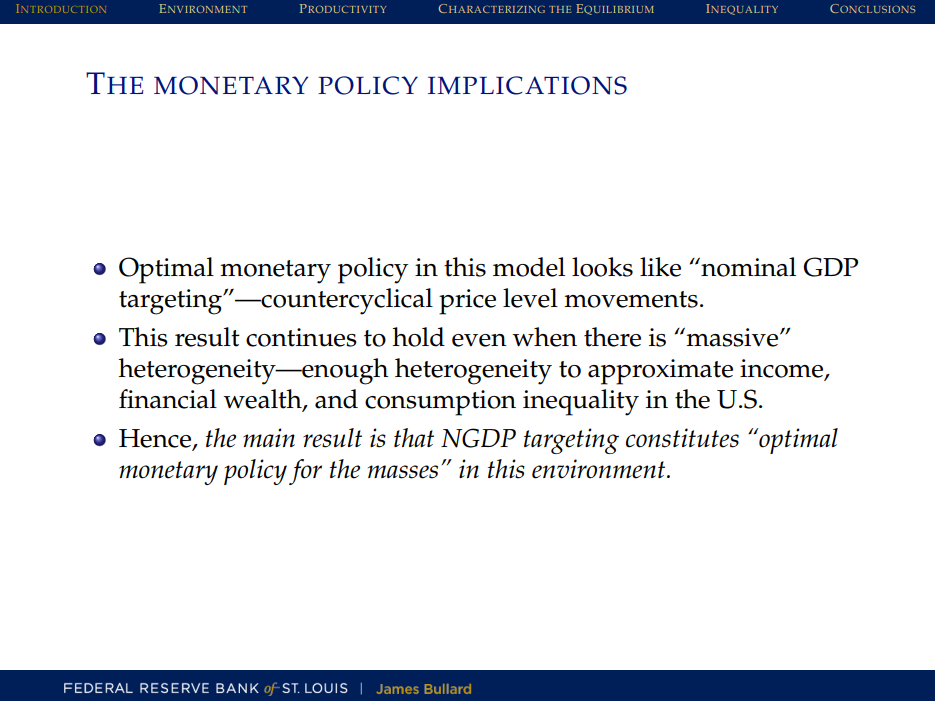

Optimal Monetary Policy For the Masses: the James Bullard and Larry Summers View

A new post by David Beckworth summarizes a new paper by James Bullard and Ricardo DiCecio:

“This paper builds upon the risk-sharing view of NGDP targeting. The basic idea is that in a world of fixed-price nominal debt contracts (i.e. the real world), a NGDP level target provides better risk sharing among creditors and debtors against economic shocks than does a price stability target.

This is because a NGDP level target makes inflation countercyclical. During recessions, inflation rises and causes creditors to bear some of the unexpected pain by lowering the real debt payments they receive from debtors. During booms, inflation falls and allows creditors to share in some of the unexpected gain by increasing the real debt payments they receive from debtors. Debtors, in other words, bear less risk during recessions but also share unexpected gains during expansions.

NGDP level targeting, in other words, causes a fixed-price nominal debt world to look and feel a lot like an equity-world. In a similar spirit, some observers have called for a risk-sharing mortgages as a way to avoid another Great Recession. The point of this paper is that the same benefit that such risk-sharing mortgages would bring can be had by having a central bank target the growth path of NGDP.”

A new post by David Beckworth summarizes a new paper by James Bullard and Ricardo DiCecio:

“This paper builds upon the risk-sharing view of NGDP targeting. The basic idea is that in a world of fixed-price nominal debt contracts (i.e. the real world), a NGDP level target provides better risk sharing among creditors and debtors against economic shocks than does a price stability target.

This is because a NGDP level target makes inflation countercyclical.

Posted by at 10:32 AM

Labels: Inclusive Growth

Housing View – June 15, 2018

On cross-country:

- “Hot Property: the housing market in major cities” – Netherlands Bank

- Built on Sand? Global Housing Sector Showing Weakness – Continuum Economics

- The Dog that didn’t Bark: Social Housing in European Peripheries – Copenhagen Business School

On the US:

- Housing and expenditures: before, during, and after the bubble – Bureau of Labor Statistics

- Luxury Dorms Are Struggling to Fill Beds – Bloomberg

- Housing Sentiment Continues to Strengthen, but High Home Prices Complicate Consumer Purchase Confidence – Fannie Mae

- Developers are taking on residential building challenges by extending the concept of prefabricated housing to manufacture entire apartment buildings – New York Times

- Finding Common Ground on Rent Control – Terner Center for Housing Innovation

- Reported Mortgage Demand Falls to Three-Year Low, Fueling Lenders’ Negative Profit Margin Outlook – Fannie Mae

- Affordable Housing Is Your Spare Bedroom – New York Times

- Philadelphia Wants To Tax Housing Construction to Make Housing Cheaper – Reason

- Home Equity Lines of Credit Increase 14 Percent in Q1 2018 – ATTOM

On other countries:

- [Canada] ‘Growth coalition’ kept foreign money flowing into B.C. real estate, professor says – Globe and Mail

- [Canada] Uncertainty reigns, though Ford’s win may signal shift for Ontario housing policy – Globe and Mail

- [Canada] Foreign buying of Vancouver real estate—beware the siren call of sovereignty – Straight

- [Czech Republic] Czech central bank caps mortgage loans as property prices soar – Reuters

Photo by Aliis Sinisalu

On cross-country:

- “Hot Property: the housing market in major cities” – Netherlands Bank

- Built on Sand? Global Housing Sector Showing Weakness – Continuum Economics

- The Dog that didn’t Bark: Social Housing in European Peripheries – Copenhagen Business School

On the US:

- Housing and expenditures: before, during, and after the bubble – Bureau of Labor Statistics

- Luxury Dorms Are Struggling to Fill Beds – Bloomberg

- Housing Sentiment Continues to Strengthen,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 14, 2018

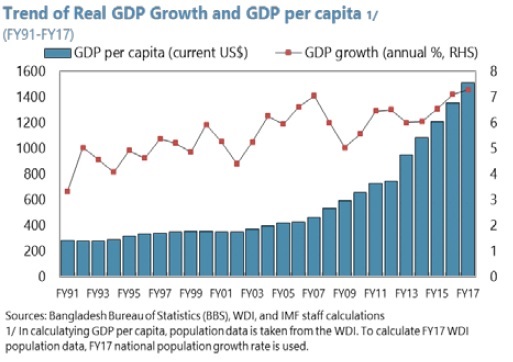

Bangladesh Reaches Middle Income Status

A new post by Timothy Taylor discusses Bangladesh’s growth, declined poverty, gender equity, and financial sector: “Bangladesh has over 160 million people, which makes it the eighth most populous country in the world (just behind Pakistan and Nigeria, just ahead of Russia, Mexico, and Japan). I can’t claim that I’ve been paying close attention to its economy, but I was nonetheless started to see that Bangladesh has shifted (in the World Bank’s classification) from being a “low-income” to a “middle-income” country.”

A new post by Timothy Taylor discusses Bangladesh’s growth, declined poverty, gender equity, and financial sector: “Bangladesh has over 160 million people, which makes it the eighth most populous country in the world (just behind Pakistan and Nigeria, just ahead of Russia, Mexico, and Japan). I can’t claim that I’ve been paying close attention to its economy, but I was nonetheless started to see that Bangladesh has shifted (in the World Bank’s classification) from being a “low-income”

Posted by at 10:02 AM

Labels: Inclusive Growth

Subscribe to: Posts